Compare Home Insurance Plans in Ohio

Find your best options in less than 2 minutes

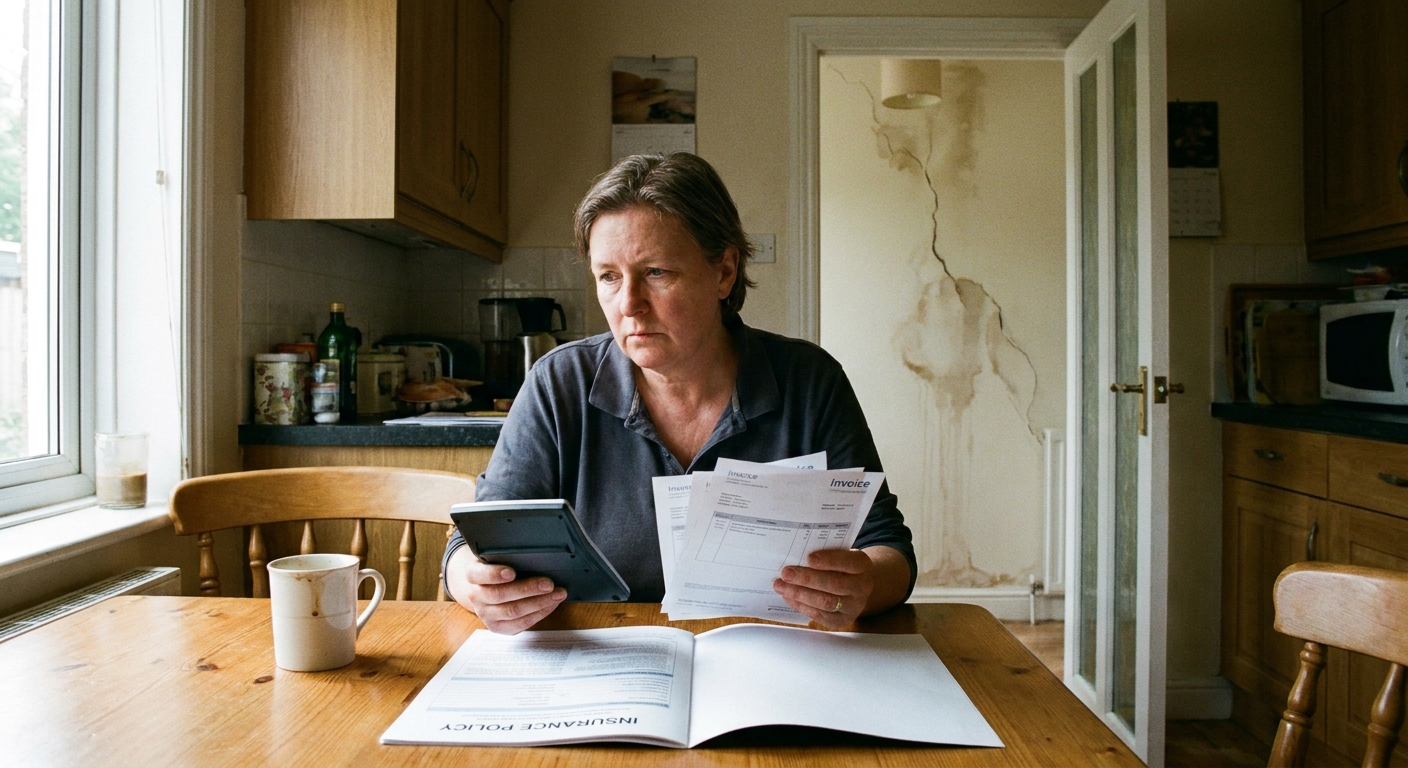

The Real Cost-Benefit Analysis: Deductible vs. Repair Cost vs. Premium Increase

Before you call your insurer, you need to run the numbers — because filing a claim isn't always the financially smart move. The core calculation involves three variables: your deductible, the cost to repair the damage, and how much your premium will increase afterward.

The Golden Rule: Experts generally recommend only filing a claim when the repair cost is at least 1.5x to 2x your deductible. For a $1,000 deductible, that means your damage should realistically exceed $1,500–$2,000 before filing makes sense.

Here's why: even a single claim can raise your annual premium by 7% to 30% depending on the claim type. On an average national premium of roughly $2,424 per year, a 20% increase adds nearly $485 annually — and that hike typically lasts 3 to 5 years. That's potentially $1,455 to $2,425 in added costs over the penalty period, which can easily wipe out the benefit of a small payout.

| Damage Cost | Deductible | Net Payout | Est. Premium Hike (3 yrs) | File a Claim? |

|---|---|---|---|---|

| $800 | $1,000 | $0 | N/A | ❌ No |

| $1,500 | $1,000 | $500 | ~$1,200–$1,500 | ❌ No |

| $3,500 | $1,000 | $2,500 | ~$1,200–$1,500 | ⚠️ Maybe |

| $8,000 | $1,000 | $7,000 | ~$1,200–$1,500 | ✅ Yes |

| $25,000+ | $2,500 | $22,500+ | ~$1,500–$2,500 | ✅ Absolutely |

Understand your home insurance deductible before any damage happens — choosing the right deductible amount is one of the most powerful ways to manage this tradeoff proactively.

Compare Home Insurance Plans in Ohio

Find your best options in less than 2 minutes

How Claims Affect Your Rates and Insurability

Filing a claim doesn't just affect your premium for one year — it leaves a mark on your record that follows you for up to 7 years through a database called the CLUE report (Comprehensive Loss Underwriting Exchange), maintained by LexisNexis. About 90% of homeowners insurers pull this report when writing new policies or evaluating renewals.

What makes the CLUE report particularly important is that even zero-payout claims appear on your record. If you call your insurer to ask about a potential claim but ultimately don't file, that inquiry may still be logged. And if you do file and receive nothing — because the damage fell below your deductible — your rates can still rise.

How Much Do Premiums Increase by Claim Type?

| Claim Type | Avg. Premium Increase | Risk of Non-Renewal |

|---|---|---|

| Fire damage | ~22% | Moderate–High |

| Liability | ~20% | Moderate |

| Theft | ~20% | Moderate |

| Water damage | ~19% | Moderate–High |

| Vandalism | ~19% | Moderate |

| Wind/Hail | ~9% | Low–Moderate |

| Lightning | ~10% | Low |

Water damage claims in particular raise flags because insurers see them as high-recurrence risks. Learn more about what water damage home insurance covers to understand which water events are even eligible for a payout before you consider filing.

The Multiple-Claims Danger Zone

The non-renewal risk escalates sharply when you file more than one claim in a short window. Most insurers treat 2 or more claims within a 3-to-5-year period as a serious red flag. At 3+ claims in 4 years, non-renewal becomes very likely. And in today's tightening market, some insurers are non-renewing policies after just one claim in high-risk zip codes or wildfire-prone areas.

Insurers are legally required to give 30 to 60 days written notice before non-renewal, but that's cold comfort when you're scrambling to find new coverage. Non-renewal doesn't just mean paying more — it can mean being pushed to your state's FAIR plan, which typically provides less coverage at higher cost.

Protect your home with State Farm

Average Rate:

Homeowners who bundle and save with State Farm save an average of $1,000 per year!

You're in Good Hands® with Allstate

Average Rate:

Get comprehensive home coverage with flexible policy options.

Customize your home coverage

Average Rate:

Only pay for the coverage you need with personalized home insurance.

Smart coverage for your home

Average Rate:

Protect what matters most with award-winning home insurance.

What's Always Worth Claiming vs. Borderline Cases

Not all damage is created equal. Here's a practical breakdown of when to file without hesitation and when to pause and calculate first.

Always File a Claim

For roof-specific situations, the age of your roof matters enormously. If your roof is under 15 years old and sustains significant storm or hail damage, filing is almost always worth it. After 15 years, many insurers switch to actual cash value (ACV) payouts that factor in depreciation, significantly reducing your payout. Check out our full guide on home insurance and roof replacement to understand what you're entitled to.

For structural issues, home insurance coverage for structural damage is another area where the type and origin of damage determines everything — sudden events are covered; gradual settling or neglect is not. Review your home insurance maintenance requirements to make sure ongoing upkeep doesn't give your insurer grounds to deny the claim.

Your Decision Framework: Should You File or Pay Out of Pocket?

Use this step-by-step framework before making your decision:

Step 1 — Confirm Coverage First

Is the damage caused by a covered peril? Floods, earthquakes, normal wear and tear, and animal damage are typically not covered by standard homeowners policies. Filing a claim for an excluded peril creates a record with no payout — the worst of both worlds. If you're unsure what's covered, review your policy or check our guide on accidental damage and home insurance.

Step 2 — Get a Repair Estimate

Before calling your insurer, contact a licensed contractor to get a written repair estimate. If the cost is less than your deductible, stop here — filing accomplishes nothing and creates a claims record.

Step 3 — Run the 3-Year Premium Math

Multiply your estimated annual premium increase percentage by your current premium, then multiply by 3 years (the minimum claim penalty period).

Formula: (Current Annual Premium × % Increase) × 3 years = Long-Term Cost of Filing

If this number exceeds your net payout (repair cost minus deductible), paying out of pocket saves you money.

Step 4 — Check Your Claims History

Pull your free CLUE report at LexisNexis before filing. If you've already filed 1 claim in the past 3 years, a second claim significantly increases non-renewal risk. Understand what happens to home insurance after a claim before adding another entry to your record.

Step 5 — Consider Timing and Deadlines

Some states have specific extensions. California, for example, extends timelines for claims filed during a declared state of emergency. Always notify your insurer as soon as reasonably possible, even if you haven't decided whether to file formally — this protects your rights without locking you into a formal claim.

Step 6 — File If the Numbers Work

If the repair cost significantly exceeds your deductible, the damage type is covered, you don't have multiple recent claims, and the net payout outweighs the long-term premium increase — file the claim. Once you do, understand the full home insurance claims process so you're prepared for every step from adjuster visit to final payout. And know your home insurance payout options so you can advocate for the best settlement structure.

Frequently Asked Questions

What is the minimum damage amount worth filing a home insurance claim for?

Most insurance experts recommend only filing a claim when the total repair cost is at least 1.5 to 2 times your deductible. For a $1,000 deductible, that means damage should be $1,500–$2,000 or more before filing makes financial sense. Below that threshold, the premium increase over 3 to 5 years will likely cost more than your net payout. Always get a written contractor estimate before calling your insurer.

How long does a home insurance claim affect your premium?

A home insurance claim typically affects your premium for 3 to 5 years, which is how long it stays active as a rating factor with most insurers. The claim itself remains in the CLUE database for up to 7 years, meaning new insurers can see your history even after rates normalize with your current carrier. The impact varies by claim type — fire and liability claims cause the steepest increases, while weather-related claims like wind or lightning tend to have a smaller effect.

Can I be dropped from home insurance for filing too many claims?

Yes. Filing 2 or more claims within a 3-to-5-year window is considered a major red flag by most insurers and significantly increases your risk of non-renewal. Some insurers in high-risk markets are now non-renewing policies after even a single claim, particularly in wildfire or flood-prone regions. Insurers must provide 30 to 60 days written notice before non-renewal, but once you're dropped, finding affordable new coverage becomes difficult due to your CLUE report history.

Does calling my insurance company about a potential claim count against me?

It depends on the insurer and how the call is logged. Some insurers record inquiries that don't result in a formal claim as "zero-dollar claims" on your CLUE report, which can still be seen by future insurers. To be safe, consult with an independent insurance agent before calling your insurer to discuss speculative damage. Get a repair estimate first so you only contact your insurer when you've already decided the numbers justify filing.

How soon do I need to report damage to my home insurance company?

Most home insurance policies require you to report damage "promptly" or within a specific window — typically within a few days to a few weeks of discovery. The formal claims deadline is usually 12 months from the date of loss, but many policies have shorter notice requirements written into the fine print. Missing the notification deadline can give your insurer grounds to deny your claim entirely. Always notify your insurer as soon as you discover significant damage, even if you haven't yet decided to file formally.