Compare Home Insurance Plans in Ohio

Find your best options in less than 2 minutes

How Many Claims Triggers a Red Flag?

There is no single law that sets a hard claims limit, and no formal industry threshold exists in 2026. However, most insurance underwriters apply an informal rule of thumb: 2 to 3 claims within a 3 to 5 year window is typically where alarm bells start ringing. Carriers are reviewing homeowners' claims much more closely, and non-renewals are more likely when there are two or more claims in the last three to five years, a major water loss, repeat sump pump or drainage claims, storm-related roof claims, or liability incidents. Frequency (not just severity) impacts eligibility.

It's important to understand the difference between a cancellation and a non-renewal. A mid-term cancellation (cutting your coverage before the policy ends) is heavily regulated by state law and generally limited to specific reasons like non-payment, fraud, or a material change in risk. Non-renewal happens at the end of your policy term and requires far less justification. In 2026, insurers are moving away from state-wide risk assessments and toward hyper-local ZIP code modeling, with companies like State Farm and Allstate using satellite imagery and AI to identify specific neighborhoods (sometimes just a few blocks) that they now deem uninsurable. Texas even passed a law effective January 1, 2026, requiring insurers to publicly disclose their reasons for non-renewals by ZIP code.

Here's a general overview of how claim volume tends to influence insurer decisions in 2026:

| Claims in 3–5 Years | Likely Insurer Response |

|---|---|

| 1 claim | Premium increase of roughly 10%–25% (up to 33% for fire); no major coverage threat |

| 2 claims | Steep rate surcharge (40%–80%); increased underwriting scrutiny |

| 3 claims | Strong non-renewal risk; may be flagged as high-risk |

| 4+ claims | Near-certain non-renewal; likely restricted to surplus lines or FAIR plans |

Learn more about what happens after a claim to understand the full downstream impact on your policy and premium.

Compare Home Insurance Plans in Ohio

Find your best options in less than 2 minutes

How Different Claim Types Are Weighted

Not all claims are created equal in the eyes of an underwriter. Insurers look at both the frequency and the severity of claims, but certain claim types raise far more concern than others.

Water Damage Claims

Water damage is one of the most scrutinized claim types in home insurance. Repeated water damage claims (from burst pipes, plumbing leaks, or appliance failures) signal to insurers that a property may have ongoing maintenance issues or structural vulnerabilities. According to ConsumerAffairs data covering 2017 to 2021, the average U.S. household claim for water damage and freezing exceeded $12,500, and water damage comprised almost 24% of all U.S. homeowner insurance claims. A single water damage claim typically increases premiums by about 25%, and insurers frequently raise rates after paying these claims because they view water losses as likely to recur.

Liability Claims

Liability claims (think dog bites, slip-and-fall injuries on your property) are relatively rare but expensive when they do occur. Even a single liability claim can cause an insurer to reassess your risk profile, especially if the circumstances suggest a pattern like multiple dog bite incidents or an "attractive nuisance" (pool, trampoline, dog with bite history). A modest liability claim typically raises premiums 10% to 20%, while a large bodily injury claim or one involving an ongoing exposure can push increases to 30% or more.

Catastrophic and Weather-Related Events

Wind and hail remain among the most common claim types nationally. Insurers generally treat a single weather-related event with more leniency than a series of non-weather claims, because a hurricane or tornado is considered outside the homeowner's control. In fact, in states like Florida, insurers should not raise your rates simply because you filed a hurricane or storm claim. However, in high-catastrophe regions (Florida, Texas, coastal California), even weather claims can accelerate non-renewal decisions as carriers reduce exposure. In 2026, insurers are using satellite imagery and drones to flag roof age, defensible space, and neighborhood-level hazards at the ZIP-code level.

Protect your home with State Farm

Average Rate:

Homeowners who bundle and save with State Farm save an average of $1,000 per year!

You're in Good Hands® with Allstate

Average Rate:

Get comprehensive home coverage with flexible policy options.

Customize your home coverage

Average Rate:

Only pay for the coverage you need with personalized home insurance.

Smart coverage for your home

Average Rate:

Protect what matters most with award-winning home insurance.

The CLUE Report: Your Claims History Follows You

Even after switching insurers, your claims history doesn't disappear. That's because virtually every insurer in the country reports claims to the CLUE database (Comprehensive Loss Underwriting Exchange), maintained by LexisNexis Risk Solutions. According to the Consumer Financial Protection Bureau, CLUE collects and reports up to seven years of home insurance and personal property claims to help inform pricing and underwriting decisions.

What the CLUE Report Contains

The CLUE report is a detailed record that includes:

- Date of each loss

- Type of loss (fire, water, liability, etc.)

- Amount paid by the insurer

- Policy number and property address

This data is retained for up to 7 years from the date of loss. When you apply for coverage with a new insurer, they will pull your CLUE report before issuing a quote. A history of multiple claims (even with a different company) will directly influence your new premium or eligibility.

Get the full walkthrough on how to check, correct, and interpret your CLUE report so you can use it strategically when shopping for insurance or buying a new home.

CLUE and Home Sales

The CLUE report follows the property, not just the owner. If you're buying a home, you can request that the seller provide a copy of the property's CLUE report before closing. A history of repeated water damage or fire claims on the home you're purchasing could mean higher premiums, or difficulty finding coverage at all.

Should You File a Claim or Pay Out of Pocket?

One of the most powerful tools for protecting your claims history is simply deciding not to file for smaller losses. This is especially true in 2026, when insurers are more aggressive about non-renewals and premium surcharges. National home insurance rates have risen 46.8% cumulatively from 2020 to 2025 (peaking at a 12.7% jump in 2024 before easing to 6.0% in 2025), so any post-claim surcharge lands on top of an already elevated base premium. Before reaching for the phone to call your insurer, run through this decision-making framework.

The Core Calculation

Estimated repair cost minus your deductible equals potential insurance payout.

If that number is low (say, under $1,500), the premium surcharges you'll absorb over the next 3 to 5 years could easily exceed what the insurer would have paid you. A single claim can raise your rates 10% to 40% nationally, and a second claim within a few years can push increases to 40% to 80%, with a second fire claim adding up to a 60% surcharge and a second theft claim around 55%. Experts commonly suggest only filing when the damage significantly exceeds your deductible, typically by at least $1,000 to $2,000 or more.

| Scenario | Repair Cost | Deductible | Net Payout | Recommendation |

|---|---|---|---|---|

| Broken window | $400 | $1,000 | $0 | Pay out of pocket |

| Minor roof damage | $1,800 | $1,000 | $800 | Usually pay OOP |

| Water damage | $6,500 | $1,500 | $5,000 | File the claim |

| Major fire damage | $45,000 | $2,000 | $43,000 | Definitely file |

When to Absolutely Pay Out of Pocket

- The repair cost is at or below your deductible

- You've already filed one or more claims in the past 3 years

- The damage is in a gray area for coverage (e.g., gradual wear vs. sudden event)

- You're concerned about policy non-renewal

Get a full breakdown on when to file a claim versus paying out of pocket, and understand how the claims process works before you decide to move forward.

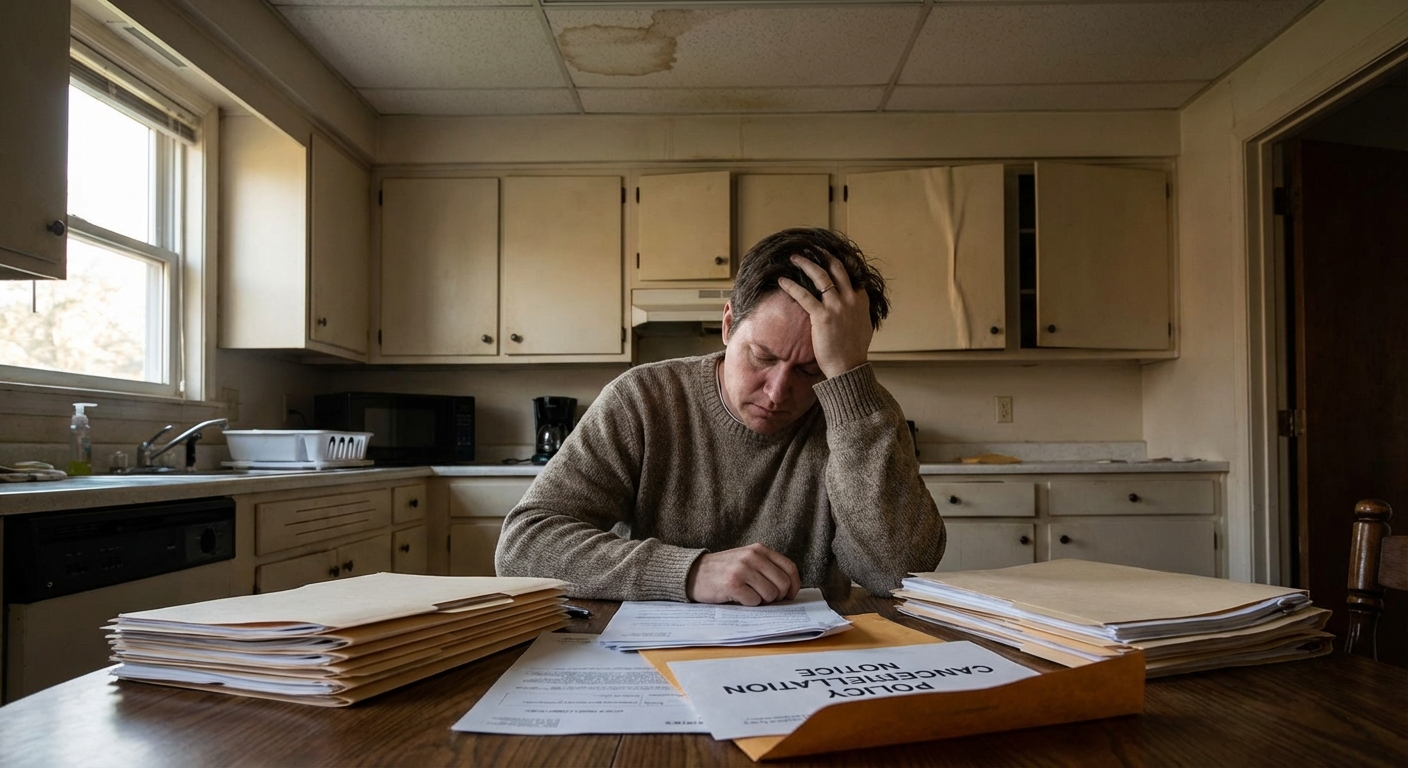

What to Do If You've Been Dropped

Receiving a non-renewal notice is alarming, but it doesn't mean you're out of options. Non-renewals in 2026 are concentrated in California, Florida, Texas, and Louisiana. Here's how to navigate the situation strategically.

Step 1: Don't Panic, But Act Fast

State law requires insurers to give advance notice before non-renewal, typically 30 to 120 days depending on your state. Florida home insurance companies must provide 120 days' notice, while Louisiana providers only need 30 days. Massachusetts requires at least 45 days. Use that time wisely. Ask your current insurer if there are any steps you can take to reverse the decision, like replacing an aging roof (many carriers won't insure roofs older than 15 to 20 years), clearing defensible space, or completing a home inspection.

Step 2: Shop the Standard Market First

Not every insurer weighs claims history the same way. An independent insurance agent can submit your application to multiple carriers simultaneously, including smaller regional insurers that may take a different view of your risk profile. In California, State Farm's March 2026 settlement extended its moratorium on non-renewals and cancellations for at least an additional year, so some homeowners who were on the brink of losing coverage have gained breathing room.

Step 3: Consider Surplus Lines (E&S) Insurers

If standard carriers won't write your policy, the Excess & Surplus (E&S) lines market is your next option. If the "Big Three" legacy carriers (State Farm, Allstate, or Farmers) drop you, don't let your coverage lapse. Immediately look for Excess and Surplus lines. Reputable surplus lines carriers include names like AIG and Lloyd's of London. Expect higher premiums and potentially more exclusions, but it's legitimate coverage.

Step 4: State FAIR Plans

Every state with a FAIR (Fair Access to Insurance Requirements) plan offers coverage as a last resort for homeowners who can't find it elsewhere. California's FAIR Plan alone has grown to 684,388 policies in force as of March 2026, a 152% increase since September 2022, with total exposure now at $750 billion. Its rates are set to rise by an average of 29.1% statewide starting with renewals on or after October 15, 2026, the largest approved increase in recent history. FAIR plans typically provide less comprehensive coverage at higher-than-market rates, but they keep you legally covered and protect you from lender-imposed force-placed insurance.

If you've already received a non-renewal notice, read our detailed guide on home insurance non-renewal for a step-by-step plan. And if you've been outright denied, see what to do after a denial to understand your full range of options.

Frequently Asked Questions

How many home insurance claims is too many?

Most insurers consider 2 to 3 claims within a 3 to 5 year period to be a significant red flag. At that level, you'll likely see premium surcharges of 40% to 80%, and insurers may choose not to renew your policy. There's no universal rule written into law, but underwriting guidelines across the industry tend to converge on this range in 2026. The type and severity of claims matter too, not just the count.

Will filing a small home insurance claim raise my rates?

Yes. Even a relatively small paid claim can increase your premium by 10% to 40% nationally, with water damage claims averaging about a 25% jump. In sample states like California, a first fire claim raises the average premium roughly 33%, in Florida about 20%, and in New York around 18%. The surcharge typically follows you for 3 to 7 years and applies at renewal, not immediately, so modest payouts often aren't worth filing.

Can I get home insurance with a bad claims history?

Yes, but your options may be more limited and more expensive. If standard carriers decline your application, you can look to the Excess & Surplus (E&S) lines market or your state's FAIR Plan. Working with an independent agent who specializes in high-risk properties is often the fastest path to finding a workable policy, and in 2026 growth in California's FAIR Plan is actually slowing, suggesting more private capacity is returning to some markets.

Does my claims history follow me if I switch insurance companies?

Absolutely. Your claims history is stored in the CLUE database maintained by LexisNexis for up to seven years for home and personal property claims. Every insurer you apply with will pull this report before offering you coverage. Switching companies doesn't reset your record, but claims older than seven years should automatically fall off the report and no longer affect underwriting decisions.

What is a zero-paid claim, and does it hurt me?

A zero-paid claim occurs when you report a potential loss to your insurer but no money is ultimately paid out, either because the damage fell below your deductible or you decided not to proceed. Despite the $0 payout, this inquiry is still recorded on your CLUE report and can be viewed as a negative signal by future underwriters. In 2026, carriers using hyper-local ZIP-code risk modeling may treat even a single reported inquiry as evidence of elevated risk, so it's worth thinking carefully before calling in a small loss.