Compare Home Insurance Plans in Ohio

Find your best options in less than 2 minutes

Why Are Home Insurance Rates Still Going Up in 2026?

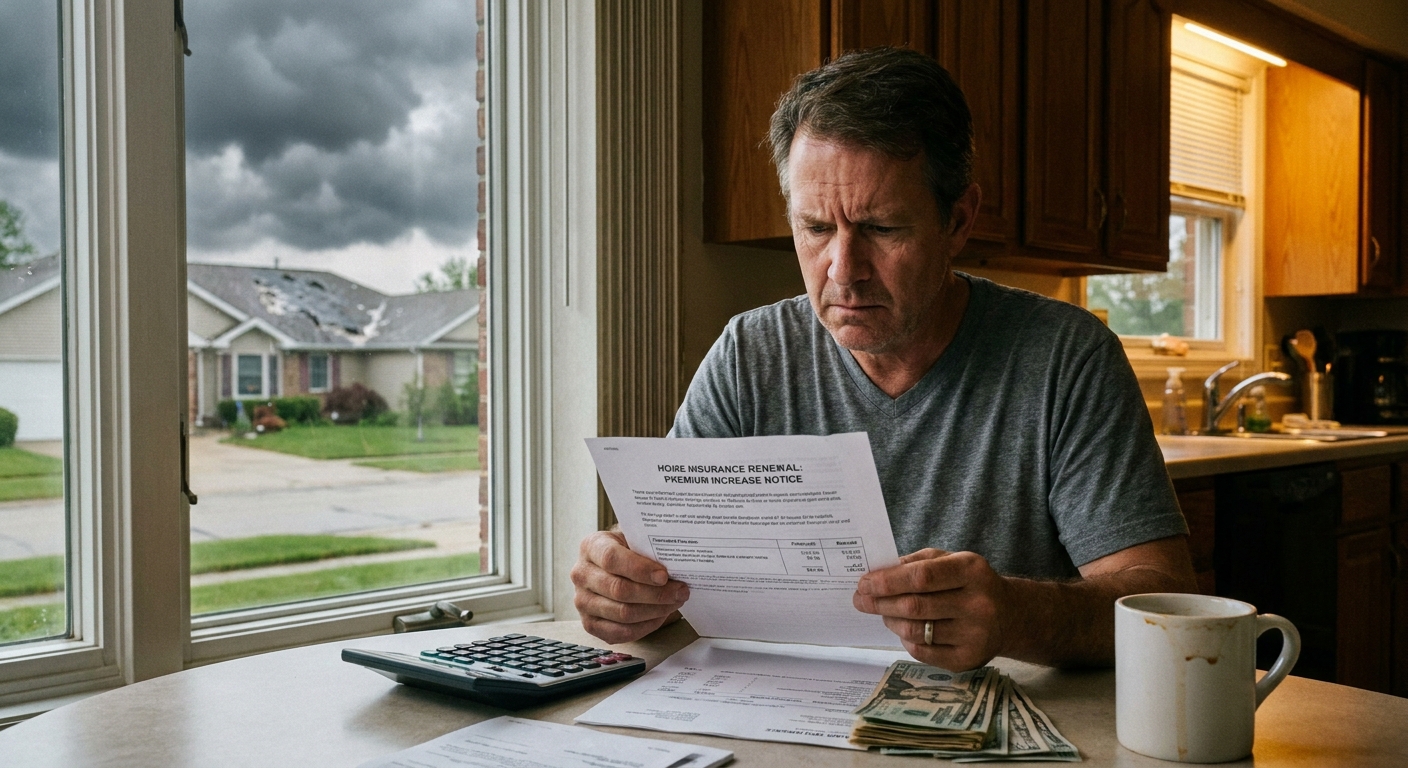

Home insurance premiums are climbing for a fifth consecutive year, and many homeowners are asking the same question: when does it stop? The short answer is not yet, but the pace is finally slowing. Understanding what's actually driving rates higher puts you in a much better position to respond strategically.

Multiple structural forces are converging in 2026 to keep upward pressure on premiums, even as growth has moderated to the low single digits nationally. U.S. home insurance rates rose a cumulative 46.8% from 2020 to 2025, with annual increases accelerating sharply in 2022 and peaking at 12.7% before beginning to slow.

The Biggest Cost Drivers Behind 2026 Rate Increases

Severe Convective Storms Remain the Dominant Loss Driver

Tornadoes, hailstorms, and high-wind events, collectively known as severe convective storms (SCS), have overtaken hurricanes as the single biggest loss driver in the U.S. property insurance market. Severe convective storms have risen to prominence on the risk management agenda, with global insured losses totaling $208 billion over the past three years, and the U.S. accounts for the overwhelming majority of that damage.

According to Munich Re, severe thunderstorm losses in the United States amounted to $56 billion in 2025, of which $42 billion was insured, significantly higher than the 10-year average. In 2026, the trend continues: U.S. severe convective storm insured losses surpassed $22 billion by mid-June 2026, marking the 11th consecutive year with more than $20 billion in annual SCS insured losses.

Hail is the primary culprit. The Insurance Information Institute notes that hail alone can account for as much as 80% of severe convective storm claims in a given year, with roofs responsible for 70 to 90% of total insured residential catastrophic losses. You can learn more about how extreme weather is driving up costs for homeowners across every region.

Reinsurance Costs Are Finally Softening (But Still Elevated)

Insurers don't absorb catastrophic risk alone. They purchase reinsurance, and after years of steep increases, that market is finally turning. Property-catastrophe reinsurance prices fell again at January 1, 2026 renewals with double-digit percentage declines, though prices remain above pre-2023 levels. Howden Re estimates risk-adjusted property catastrophe reinsurance rates-on-line decreased by as much as 25% on a weighted-average basis at the June 1, 2026 renewal.

This is genuinely good news for the market long-term, but the savings take time to reach consumers. Learn more about how reinsurance affects your home insurance rates and why it's one of the biggest hidden forces driving your bill.

Accumulated Prior-Year Losses and Construction Inflation

Many insurers are still recovering financially from catastrophic loss years between 2017 and 2023, when the industry paid out far more in claims than it collected in premiums. Rate hikes in 2026 are partly a mechanism to rebuild that financial cushion. Construction cost inflation continues to compound this problem, pushing replacement cost values higher every year policies are renewed.

Trade Tariffs Adding New Pressure

A lesser-discussed wildcard in 2026: tariffs on Canadian lumber and imported building materials are directly inflating home reconstruction costs. According to Insurify, tariffs on building materials could raise the average annual home insurance premium meaningfully, potentially pushing rates even higher by year-end 2026 in a worst-case scenario.

Compare Home Insurance Plans in Ohio

Find your best options in less than 2 minutes

2026 Home Insurance Rate Increases by State

Rate increases are far from uniform. Where you live matters enormously when it comes to what you'll pay in 2026.

States Facing the Highest Increases

According to Insurify's 2026 projections, the states expected to see the steepest home insurance rate hikes are:

| State | Projected 2026 Increase | Primary Risk Factor |

|---|---|---|

| Louisiana | ~23% | Hurricanes, carrier insolvencies |

| Maine | ~19% | Storm frequency, coastal exposure |

| Michigan | ~14% | Severe storms, hail |

| Utah | ~13% | Wildfire, hail |

| Montana | ~12% | Wildfire, wind |

Consumers in a third of ZIP codes across the country saw premiums rise by more than 30% from 2021 to 2024, with the sharpest increases in Utah and other high-growth Western states. Meanwhile, the California home insurance crisis has taken a dramatic new turn. The California Department of Insurance approved a 29.1% average FAIR Plan rate increase statewide, effective October 15, 2026, and policyholders with significant wildfire exposure may see the wildfire portion of their premium double.

Colorado also continues to bleed. Colorado has seen the largest cumulative increase in home insurance rates, with costs rising 100.8% (more than doubling) from 2020 to 2025, driven largely by wildfire and hail exposure.

States Where Rates Are Actually Falling

Florida is the most notable exception to the national trend, and the turnaround has been dramatic. After years of being the most volatile home insurance market in the country, legislative reforms enacted in 2022–2023 are finally producing results. Citizens Property Insurance Corporation's Board of Governors approved 2026 rate recommendations that reduce average rates by 2.6% statewide, with about 60% of customers seeing an average premium cut of 11.5% (roughly $359).

By the end of 2025, Citizens' policy count is expected to fall to 385,000, a decrease of 73% from the October peak and the lowest level ever, as private carriers absorb former Citizens policyholders. Private insurers are also filing rate cuts. Some homeowners in Florida's insurance market are seeing premium reductions of 5% to 11% on renewal.

Protect your home with State Farm

Average Rate:

Homeowners who bundle and save with State Farm save an average of $1,000 per year!

You're in Good Hands® with Allstate

Average Rate:

Get comprehensive home coverage with flexible policy options.

Customize your home coverage

Average Rate:

Only pay for the coverage you need with personalized home insurance.

Smart coverage for your home

Average Rate:

Protect what matters most with award-winning home insurance.

AM Best's Stable Outlook: What It Really Means

In December 2025, AM Best, the insurance industry's leading credit rating agency, revised its outlook for the U.S. homeowners insurance segment from Negative to Stable. This was a meaningful shift that reflects genuine improvement in market conditions.

AM Best cited enhanced catastrophe risk management practices, improved property reinsurance market dynamics with moderate softening in reinsurance rates, and solid though moderating premium growth combined with refined underwriting practices as key reasons for the upgrade.

What this means for you: A stable market outlook is good news over a longer time horizon. More financially healthy insurers means better competition, fewer market exits, and eventually, more pricing pressure in the consumer's favor. But that process plays out over years, not on your next renewal notice. Understanding the home insurance market stabilization picture helps set realistic expectations.

For homeowners struggling with premium increases, the home insurance affordability crisis is real, and there are more options available than most people realize.

What Homeowners Can Do Right Now

Even in a rising-rate environment, there are proven strategies to meaningfully reduce what you pay. Many homeowners are leaving hundreds of dollars on the table by not taking these steps.

6 Ways to Fight Your Rate Increase

1. Shop the market every year at renewal Carrier pricing varies enormously for the same home. Running new quotes annually, even if you stay with your current insurer, gives you negotiating leverage and can identify substantial savings. Our guide to cheap home insurance options covers 12 proven strategies.

2. Bundle home and auto Combining your home and auto insurance with the same carrier typically saves 10 to 25% on your homeowners premium. This is consistently one of the highest-return moves available.

3. Raise your deductible strategically Moving from a $1,000 to a $2,500 deductible can meaningfully reduce your annual premium. Just make sure you have the cash reserves to cover that deductible if you need to file a claim. Rising deductibles are a growing trend, and understanding how they work is essential.

4. Make risk-reducing home improvements Upgrades that reduce your home's risk profile directly lower insurer exposure. Impact-resistant roofing, storm shutters, reinforced garage doors, and monitored alarm systems all qualify for discounts with most carriers. In hurricane zones, these improvements can reduce premiums by up to 50%.

5. Ask about every available discount Claims-free history, smart home technology, new construction, loyalty programs, and senior discounts can each reduce your premium. Most homeowners don't ask, and don't receive. Review your policy with an agent specifically to identify discount opportunities.

6. Verify your coverage reflects actual replacement cost Avoid paying to insure your land or structures you no longer use. More importantly, make sure your dwelling coverage reflects current construction cost inflation. Being underinsured is a risk no homeowner should take. Our guide to lowering your home insurance premium covers 17 proven tactics with estimated savings for each.

Frequently Asked Questions

How much will home insurance increase in 2026?

The national average home insurance rate increase for 2026 is projected at roughly 4%, well down from the double-digit spikes of 2022–2024. Most regions are expected to see premium increases by less than 10% in 2026, though homeowners in high-risk states like Louisiana, Maine, and Michigan could see hikes of 12% to 23%. Your actual increase depends heavily on your location, home characteristics, and claims history.

Why did my home insurance go up in 2026?

The primary drivers are severe convective storm losses (particularly from hail and tornadoes), rising construction and material costs, elevated reinsurance expenses, and insurers recovering from years of underpriced coverage. Even if your area wasn't hit by a disaster, insurers price risk regionally and nationally. Widespread storm losses in the Midwest or wildfire losses in California influence premiums across the country. Tariffs on building materials are also adding upward pressure not seen in prior years.

Will home insurance rates go down in 2026?

For most homeowners, rates are not expected to decrease in 2026. Florida is the most notable exception, where legislative reforms have helped stabilize the market. Citizens Property Insurance approved 2026 rate cuts of 2.6% statewide on average, with 60% of policyholders seeing about 11.5% reductions. AM Best's upgrade to a stable outlook signals improving conditions, but that improvement is more likely to slow the pace of increases than trigger widespread rate cuts.

Which states have the highest home insurance rates in 2026?

Florida, Oklahoma, Louisiana, Nebraska, and Kansas consistently rank among the most expensive states for home insurance due to their high exposure to hurricanes, tornadoes, and hail. Florida homeowners pay an average of $10,240 per year, 189% above the national average, and the South and Great Plains account for the most expensive states. Average premiums range from just over $1,000 in Vermont and Hawaii to five figures in coastal Florida.

What is the average cost of home insurance in the U.S. in 2026?

The Zebra's 2026 State of Insurance report finds that the average homeowner is now paying $2,966 a year for home insurance, with the average cost nearing $3,000 a year in 2026. Your actual premium varies based on your home's age, location, construction type, and coverage limits. High-risk states can easily exceed $5,000 to $9,000 annually.