Compare Home Insurance Plans in Ohio

Find your best options in less than 2 minutes

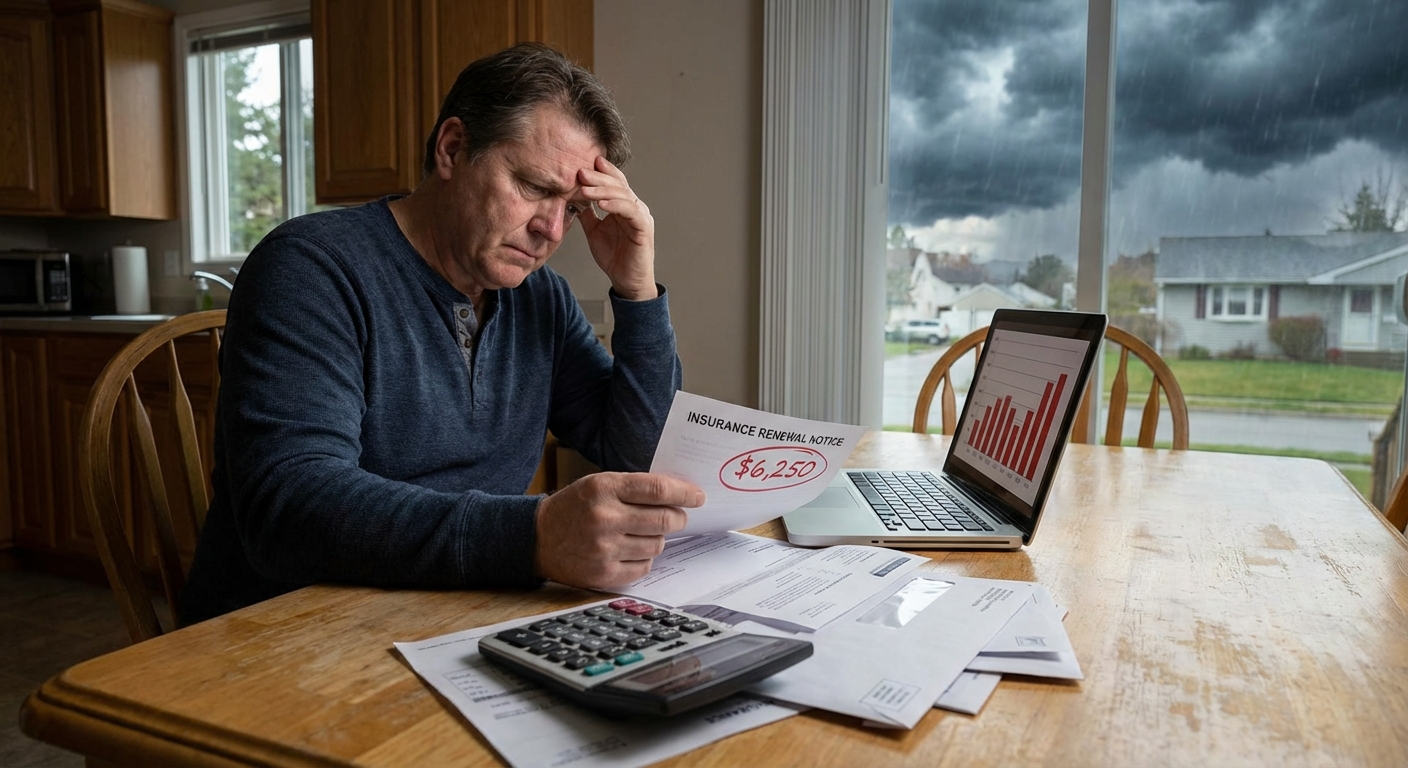

Why Home Insurance Deductibles Are Rising So Fast

If your home insurance renewal arrived with a noticeably higher deductible this year, you're not imagining things. According to Matic's 2026 Home Insurance Predictions report, the average home insurance deductible rose 22% in 2025, accelerating from an already steep 15% increase in 2024. That's a roughly 40% cumulative jump in just two years. Meanwhile, a LendingTree survey found around 1 in 10 homeowners have voluntarily raised their deductibles just to keep their premiums manageable, and another 1 in 5 said they plan to switch insurers in the next year.

So why are deductibles climbing faster than ever? Insurers are deliberately shifting more financial risk onto homeowners as a way to manage growing losses from natural disasters, soaring rebuild costs, and record-high claim payouts. Rather than absorbing every small claim, carriers are incentivizing (or in some cases requiring) higher deductibles to keep the overall insurance market sustainable. With U.S. insurers paying out roughly $103 billion in 2025 catastrophe losses (about 81% of global insured losses), the pressure to reduce claim frequency is intense, and severe convective storm losses have already surpassed $22 billion through mid-2026 before peak season even hit.

The major forces driving this shift include:

| Driver | Impact on Deductibles |

|---|---|

| Climate-related disasters (wildfires, hurricanes, storms) | More frequent, larger claims push risk to homeowners |

| Rising reconstruction & labor costs (up 45% since 2020) | Deductibles must keep pace with home replacement values |

| Premium stabilization strategy | Higher deductibles help lower premiums by 9% to 25% |

| Insurer profitability pressures | Carriers reduce exposure in high-risk states and markets |

| Stricter underwriting standards | Lower deductible options are being phased out by many carriers |

Wondering why home insurance premiums are rising at the same time? It's because the same forces (extreme weather, rebuild inflation, and reinsurance costs) are driving both premiums and deductibles upward simultaneously. You can also learn more about the ongoing affordability crisis that is forcing many households to make difficult tradeoffs.

Compare Home Insurance Plans in Ohio

Find your best options in less than 2 minutes

Flat-Dollar vs. Percentage Deductibles: Know the Difference

Not all deductibles work the same way. There are two primary structures, and understanding them is critical, especially in high-risk states.

Flat-Dollar Deductibles

A flat deductible is a fixed dollar amount you pay out of pocket before your insurer covers a covered claim. For example, if you have a $1,500 flat deductible and file a $10,000 claim for kitchen fire damage, you pay $1,500 and your insurer covers the remaining $8,500. Flat deductibles are straightforward and predictable, typically ranging from $500 to $5,000, and the Insurance Information Institute still reports $1,000 as the most common base deductible in 2026, though the share of policies at this level continues to shrink.

Percentage Deductibles

A percentage deductible works very differently. Instead of a fixed dollar amount, you pay a percentage of your home's insured dwelling value, not the claim amount. This can translate to significant out-of-pocket exposure:

| Home Insured Value | 1% Deductible | 2% Deductible | 5% Deductible |

|---|---|---|---|

| $200,000 | $2,000 | $4,000 | $10,000 |

| $300,000 | $3,000 | $6,000 | $15,000 |

| $400,000 | $4,000 | $8,000 | $20,000 |

| $500,000 | $5,000 | $10,000 | $25,000 |

As you can see, percentage deductibles can balloon quickly on higher-value homes. Carriers are increasingly shifting to this model in storm-prone regions because it scales with property values and limits insurer exposure on large claims. For a deeper dive, see our full guide on how to choose the right deductible amount.

Protect your home with State Farm

Average Rate:

Homeowners who bundle and save with State Farm save an average of $1,000 per year!

You're in Good Hands® with Allstate

Average Rate:

Get comprehensive home coverage with flexible policy options.

Customize your home coverage

Average Rate:

Only pay for the coverage you need with personalized home insurance.

Smart coverage for your home

Average Rate:

Protect what matters most with award-winning home insurance.

High-Risk Areas: Florida, Texas, and Tornado Alley

Homeowners in certain regions face the sharpest deductible increases, and those deductibles are almost exclusively percentage-based. Here's how the three highest-risk regions break down in 2026:

Florida (Hurricane Deductibles)

Florida law (statute 627.701) requires insurers to offer hurricane deductible options of $500, 2%, 5%, or 10% of the dwelling coverage limit. For properties insured at $250,000 or more, the $500 option isn't required, and for homes valued between $1 million and $3 million, a 3% option can replace the 2%. On a $400,000 home with a 2% hurricane deductible, you would pay $8,000 out of pocket before insurance pays a cent. Importantly, Florida uses a calendar-year hurricane deductible, meaning you only pay it once per calendar year with the same insurer even if multiple hurricanes strike. It's worth understanding how hurricane coverage and deductibles work in detail if you own a home in a coastal state.

Texas (Wind & Hail Deductibles)

In Texas, most carriers have officially moved to a 2% wind and hail deductible as the new standard for 2026, with The Hartford ending its 1% option in early 2026 and some carriers like Germania now writing 3% deductibles in North Texas. On a home insured for $400,000, a 2% deductible means $8,000 out of pocket before any wind or hail claim is covered. Unlike Florida, Texas wind/hail deductibles typically apply per occurrence, not once per calendar year. West Texas cities like Midland and Lubbock, among the most hail-prone in the nation, are particularly affected.

Tornado Alley States (Midwest & Plains)

States stretching across the Midwest and into the South (Oklahoma, Kansas, Nebraska, Missouri, Colorado, and parts of the Southeast) are experiencing rapidly growing tornado and hail risk. According to Aon's 2026 Climate and Catastrophe Insight report, severe convective storms generated $61 billion in insured losses globally in 2025, officially overtaking tropical cyclones as the costliest insured peril of the 21st century. Triple-I reports that U.S. severe convective storm losses alone reached $51 billion in 2025, the third consecutive year above $50 billion, and Cotality found that 42% of analyzed U.S. properties now fall into moderate-or-higher hail risk categories. Most policies in these areas now feature 1% to 2% wind/hail deductibles on top of the standard all-perils deductible.

How Wind/Hail Deductibles Work

Wind and hail deductibles are a separate deductible that only applies when damage is caused by windstorms, tornadoes, or hail, not your standard kitchen fire or burst pipe. They typically range from 1% to 5% of dwelling coverage and are triggered automatically when the peril matches. Named storm deductibles (for declared hurricanes) can range even higher, from 2% to 10%. According to Triple-I, hail alone accounts for as much as 80% of severe convective storm claims in any given year, with roofs bearing 70% to 90% of total insured residential catastrophic losses.

This means a homeowner could potentially face two separate deductibles in a single catastrophic event if the policy is structured with both a standard and a wind/hail deductible, though in Florida the hurricane deductible replaces (rather than stacks with) the AOP deductible for hurricane losses.

Smart Strategies for Managing Higher Deductibles

Rising deductibles don't have to catch you off guard. With the right approach, you can protect yourself financially and even use the deductible structure to your advantage.

Build a Dedicated Emergency Fund

Your #1 priority should be maintaining a savings reserve specifically earmarked for insurance deductibles. Financial experts recommend:

- Standard risk areas: Keep at least $1,000 to $2,500 liquid at all times, equal to your base deductible

- High-risk areas (Florida, Texas, Tornado Alley): Save 1.5 to 2x your highest applicable deductible, which may mean $5,000 to $15,000 or more

- High-value homes with percentage deductibles: Your emergency fund should reflect the actual dollar value of your deductible. Run the math on your declarations page.

When It Makes Sense to Raise Your Deductible

Voluntarily raising your deductible can be a smart financial move, but only under the right circumstances:

- You have sufficient savings to comfortably cover the higher deductible amount

- You maintain your home well and have a low claim history

- You live in a lower-risk area and don't already have mandatory high wind/hail deductibles

- The premium savings will break even with your added exposure within 3 to 4 years

Insurance.com's 2026 state-by-state analysis found that raising your deductible from $500 to $2,500 saves homeowners an average of $512 per year. NerdWallet's data shows a 9% average premium reduction when moving from $1,000 to $2,500. Aggressive increases can save even more, with some carriers offering 15% to 25% off for that same jump, but only households with substantial emergency reserves should consider higher tiers like $5,000 or $10,000.

Additional Cost-Management Strategies

- Bundle home and auto insurance to unlock multi-policy discounts of 10% to 25%

- Shop competing carriers annually. Loyalty rarely pays in today's market

- Improve your home's resilience with storm shutters, upgraded roofing, and security systems to qualify for discounts

- Avoid filing small claims. A single claim can raise your premium enough to wipe out years of savings

If you're feeling squeezed from all sides, our guide on 17 ways to lower your home insurance premium covers proven ways to cut your bill without gutting your coverage.

Frequently Asked Questions

Why did my home insurance deductible go up without me asking? Insurers periodically revise policy terms at renewal, and in many cases, raising your deductible is a condition of remaining insurable in your area. Carriers in high-risk markets are reducing their exposure by mandating higher deductibles, particularly for wind, hail, and hurricane perils. This change can happen automatically at renewal without requiring your signature. Always review your declarations page when your policy renews each year to catch any changes.

What is the average home insurance deductible in 2026? The most common base deductible remains around $1,000, according to the Insurance Information Institute, but the overall range has shifted upward with a 22% average increase in 2025 following a 15% jump in 2024. In high-risk areas, percentage-based deductibles of 2% to 5% are now standard, translating to $6,000 to $20,000+ depending on your home's insured value. Texas has moved to a 2% wind/hail standard and Florida requires hurricane options of $500, 2%, 5%, or 10%.

Do wind/hail deductibles apply to every storm, or just named hurricanes? Wind and hail deductibles apply to damage from any windstorm, tornado, or hail event, not just named hurricanes. They are triggered by the cause of the damage, not the storm's official designation. In some policies, named storm or hurricane deductibles are a separate, additional layer that kicks in only when a storm is officially declared by the National Hurricane Center. Read your policy carefully to understand which deductible applies in different scenarios.

Is it ever smart to keep a low deductible even if premiums are higher? Yes, particularly if you live in a high-risk area where you're statistically more likely to file a claim, if your emergency savings are limited, or if your home has older systems (roof, HVAC, plumbing) that are more likely to generate claims. A lower deductible trades higher annual premiums for lower out-of-pocket exposure at claim time. The right answer depends on your financial cushion, your home's condition, and your local risk profile.

How does a higher deductible affect my mortgage or escrow? Your deductible does not directly affect your mortgage payment or escrow account, but your premium does. If your premium increases at renewal (which is common even if you raise your deductible), your lender may adjust your escrow balance to cover the higher annual cost, resulting in a higher monthly mortgage payment. Raising your deductible can help offset premium increases, but homeowners with escrow accounts should watch for escrow shortage notices at renewal. Learn more about the broader affordability crisis reshaping monthly housing costs.