Compare Home Insurance Plans in Ohio

Find your best options in less than 2 minutes

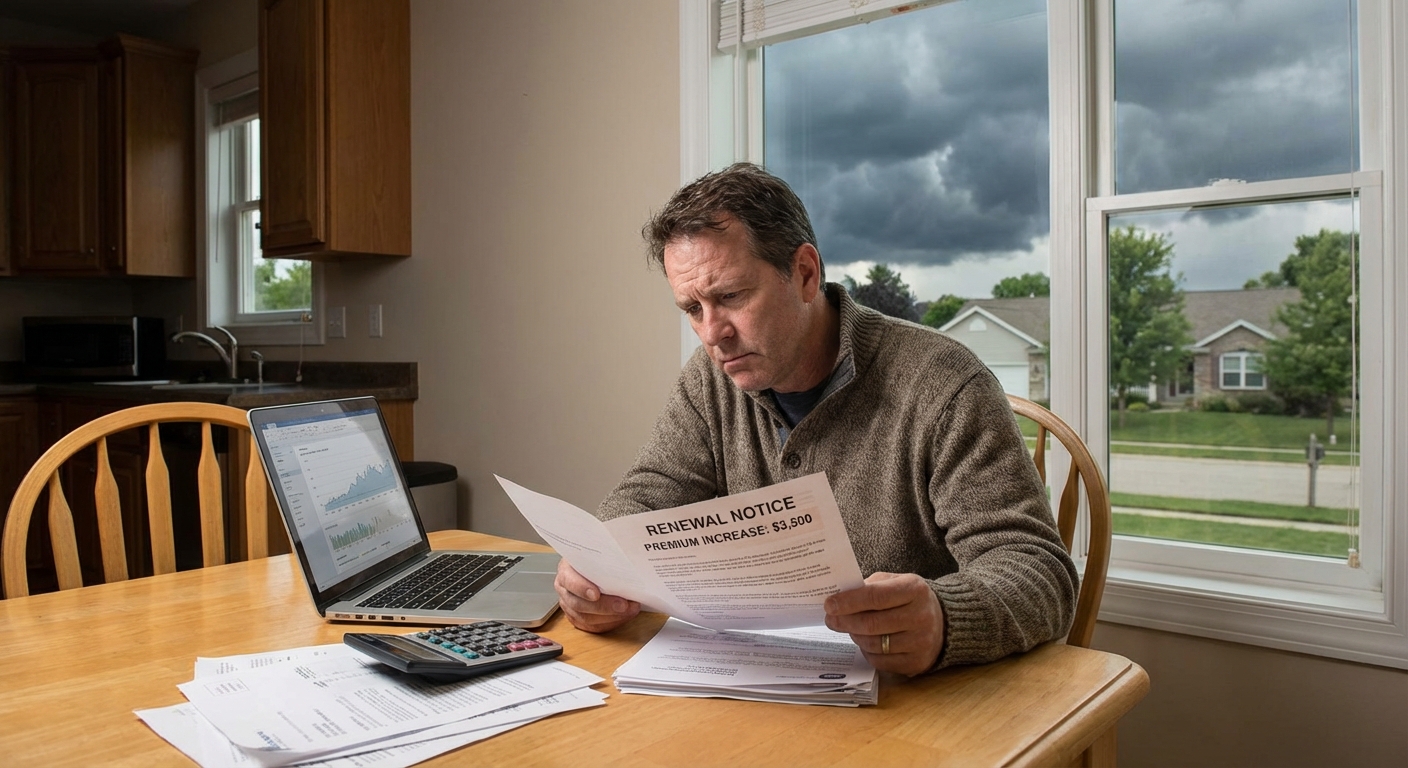

What's Driving Home Insurance Premium Increases in 2026?

Home insurance rate hikes don't happen in a vacuum. Insurers set premiums based on the risks they expect to pay out, and every major cost driver has surged simultaneously since 2021. Here's a breakdown of the forces pushing your bill higher.

Climate Change and Severe Weather Losses

The most visible culprit behind rising premiums is the surge in catastrophic weather events. Wildfires, hurricanes, hail storms, tornadoes, and flooding have all increased in both frequency and cost, forcing insurers to pay out record-breaking claims year after year.

The January 2025 Los Angeles wildfires generated billions of dollars in claims that insurers are still working through in 2026. Meanwhile, severe convective storms (large hail, damaging winds, and tornadoes) have hammered the Midwest and Plains states, generating massive claims even in areas not traditionally considered "high risk." Insurance expert Peter Kochenburger identified climate change as the "primary reason" for the recent rise in insurance premiums.

Inflation and Skyrocketing Construction Costs

When your home is damaged, the cost to repair or rebuild it has never been higher. According to a U.S. Treasury report, replacement costs for property and casualty losses rose by an average of 45% from 2020 to 2023, and labor expenses for employing construction workers on single-family homes increased 37% from 2018 to 2022.

Higher rebuild costs mean insurers must pay out more on every claim, which requires higher premiums to stay solvent. It also means your home's replacement cost, or the amount needed to rebuild it from scratch, likely increased significantly, requiring you to carry a higher coverage limit. Learn more about calculating rebuild cost so you're not dangerously underinsured.

Reinsurance Costs (Finally Easing in 2026)

Insurers don't absorb all risk themselves. They purchase their own insurance called reinsurance to cover catastrophic losses. After years of soaring reinsurance costs, 2026 is finally bringing measurable relief. Property-catastrophe reinsurance prices fell 10% to 20% at the January 1, 2026 renewals, with Gallagher Re's global property-cat rate-on-line index down 15% and similar indices from Howden Re and Guy Carpenter dropping 14.7% and 12% respectively. Gallagher Re reported reinsurance pricing declined by an average of 22.8% across its portfolio at the June 2026 Florida renewal, driven by abundant capacity and 2022 legislative reforms.

That softening is allowing insurers in catastrophe-exposed states to slow rate hikes (and in some cases reverse them). Pricing remains above pre-2023 lows, though, so this is rate stabilization rather than a full reset. Read more about how reinsurance affects your rates.

The Combined Result

| Cost Driver | Impact on Premiums | Most Affected Regions |

|---|---|---|

| Severe weather / climate losses | Very High | FL, CA, TX, Midwest, Gulf Coast |

| Construction cost inflation | High | Nationwide |

| Reinsurance cost (easing in 2026) | Moderate | High-risk states |

| Home value / replacement cost growth | Moderate | Nationwide |

| Insurance litigation costs | Moderate | LA, TX (FL improving) |

Compare Home Insurance Plans in Ohio

Find your best options in less than 2 minutes

How Much Have Home Insurance Rates Increased?

The numbers are stark. U.S. home insurance rates rose a cumulative 46.8% from 2020 to 2025, and the upward trend continued into 2026, though at a notably slower pace than the double-digit jumps of 2024.

For 2026, estimates from major analysts put the national average home insurance premium between roughly $2,395 and $2,966 per year, depending on coverage level and dataset. The Zebra reports the average homeowner is now paying $2,966 a year for home insurance, while Insurify reports a national average of $2,868 per year for a policy with $300,000 in dwelling coverage. LendingTree puts the U.S. average at $2,395 per year in its 2026 State of Home Insurance report, and Forbes estimates $2,720 for a $350,000 dwelling limit with a $500 deductible.

The Zebra notes that home insurance is expected to increase in 2026, with rates in many areas expected to rise less than 10%, though locations with recent disaster claims may grow more steeply. The bottom line: homeowners have faced a cumulative rate increase well over 45% in five years, but the pace of increases is finally beginning to moderate in lower-risk markets.

Which States Are Seeing the Biggest Increases in 2026?

Not all states are feeling equal pain. Colorado has seen the largest cumulative increase in home insurance rates, with costs more than doubling (100.8%) from 2020 to 2025, followed by Iowa (96.0%) and Minnesota (88.2%). For 2026 specifically, the heat has shifted west. According to Insurify, the states projected to see the largest 2026 rate hikes are California (16%), Nebraska (13%), and New Mexico (11%).

| State | 2026 Projected Increase | Avg. Annual Premium | Primary Risk |

|---|---|---|---|

| California | +16% | ~$2,900 | Wildfires |

| Nebraska | +13% | ~$4,956 | Severe storms / hail |

| New Mexico | +11% | ~$2,200 | Wildfires / drought |

| Colorado | High (cumulative +100.8%) | $4,310 | Wildfires / hail |

| Oklahoma | (already $5,298) | $5,298 | Tornadoes / hail |

| Florida | Decreases for many carriers | $9,449+ | Hurricanes |

Florida remains by far the most expensive state for home insurance, with an average annual cost of $9,449. However, Florida is showing real signs of recovery: since the 2022 tort reforms, at least 17 new insurance companies have entered the Florida market, and Citizens Property Insurance approved an average 8.7% statewide rate decrease (its first cut in years), with South Florida counties seeing 11-14% decreases on average. Learn more about Florida home insurance options.

California, by contrast, has effectively overtaken Florida as the most stressed property insurance market. New Stanford research finds California homeowners insurance premiums up 84% since 2020, with FAIR Plan enrollment nearly tripling from under 2% to about 5% of homes as the insurance crisis spreads beyond fire country. Nearly 400,000 California policies have been canceled or non-renewed since 2021. Read our deep dive on the California home insurance crisis.

Protect your home with State Farm

Average Rate:

Homeowners who bundle and save with State Farm save an average of $1,000 per year!

You're in Good Hands® with Allstate

Average Rate:

Get comprehensive home coverage with flexible policy options.

Customize your home coverage

Average Rate:

Only pay for the coverage you need with personalized home insurance.

Smart coverage for your home

Average Rate:

Protect what matters most with award-winning home insurance.

Why Does My Home Insurance Go Up Even With No Claims?

This is one of the most common and frustrating questions homeowners ask. The short answer: your premium is not just a reflection of your claims history, it's a reflection of your insurer's total risk exposure.

Here's why your rate rises even when you've never filed a claim:

- Regional losses: If your area experiences a major storm, wildfire, or flood, even if your home was untouched, insurers reassess the risk of everyone in that geographic area.

- Industry-wide losses: When your insurer pays out heavily on catastrophic losses anywhere in its portfolio, it needs to raise rates across all policyholders to restore financial stability.

- Rising replacement costs: Inflation has made rebuilding homes significantly more expensive. To ensure adequate coverage, your dwelling limit (and therefore your premium) must increase to keep pace.

- Reinsurance price hikes: When reinsurers charge more, those costs get distributed across your insurer's entire customer base.

- Credit and risk scoring changes: Insurers regularly re-evaluate risk factors including your credit-based insurance score, proximity to hazards, and local claims data.

Understanding what happens to home insurance after a claim (and when it's worth filing one) can help you protect your record and avoid unnecessary premium spikes.

How to Manage Rising Home Insurance Costs

You may not be able to stop the market forces driving rates up, but there are real, effective strategies to lower what you pay, sometimes by hundreds of dollars per year.

1. Shop Around Every Year

This is the single most impactful action you can take. Insurance markets shift constantly, and a carrier that was expensive last year might be highly competitive this year. Comparing quotes from multiple providers annually ensures you're not overpaying by default. Our guide to lowering your home insurance premium details 17 proven strategies that work in 2026.

2. Bundle Your Home and Auto Policies

Most major insurers offer discounts of up to 25% when you bundle home and auto (or other) insurance policies together. This is one of the fastest and simplest discounts to qualify for.

3. Increase Your Deductible

Raising your deductible (the amount you pay out of pocket before insurance kicks in) directly reduces your premium. Moving from a $500 deductible to a $2,000 deductible can generate meaningful annual savings. Be aware that average deductibles have risen 22% and many insurers in storm-prone states now require percentage-based wind and hail deductibles.

4. Make Your Home More Resilient

Upgrades that reduce your home's risk profile can directly lower your premium:

- New or impact-resistant roof: One of the most significant premium factors. Insurers reward roofs that withstand storms.

- Security systems: Alarms, cameras, smart locks, and deadbolts can reduce premiums by up to 20%.

- Smoke detectors and sprinkler systems: Qualify for additional safety discounts.

- Storm shutters and wind mitigation: Especially valuable in hurricane-prone states.

5. Stack Every Discount Available

Many homeowners leave discounts on the table. Ask your insurer specifically about:

For more guidance, read our cheap home insurance guide covering 12 ways to find affordable coverage.

6. Review Your Coverage Limits Annually

Make sure you're not paying for more coverage than you need, but also check that you're not dangerously underinsured due to rising rebuild costs. Reviewing your home insurance affordability options can help if you're struggling to keep up with premiums.

Frequently Asked Questions

Will home insurance rates ever go down?

A significant nationwide decrease is unlikely in the near term, but 2026 is showing the first real signs of moderation. Reinsurance costs are softening sharply (down 10-20% at January 2026 renewals globally and roughly 23% in Florida by June), AM Best has upgraded the U.S. homeowners insurance outlook from Negative to Stable, and Florida's Citizens Property Insurance approved its first rate cuts in years. Some lower-risk states are seeing flat or even slightly decreasing rates, though catastrophe-exposed areas like California will still see double-digit increases through 2026.

How much has home insurance gone up since 2021?

The average U.S. home insurance premium has risen substantially since 2021. U.S. home insurance rates rose a cumulative 46.8% from 2020 to 2025, with Colorado seeing rates more than double (100.8%), followed by Iowa (96.0%) and Minnesota (88.2%). Pew Research found 71% of U.S. homeowners report their costs have gone up, with 42% saying costs went up "a lot." State-level experiences vary dramatically from the national average.

Can I challenge or dispute a home insurance rate increase?

You generally cannot negotiate individual rates directly with your insurer, since rates are actuarially set and state-regulated. However, you can take meaningful action: request a policy review to verify your home's details are accurate (errors can inflate rates), ask about every available discount, and most importantly, shop competing quotes from other insurers. If you believe a rate increase is unjustified, you can also file a complaint with your state's department of insurance.

Why is my home insurance so expensive if I live in a safe area?

Even in areas with low individual risk, your premium reflects regional patterns, your insurer's portfolio-wide losses, and rising construction costs nationwide. Treasury data shows average homeowners insurance premiums per policy increased 8.7 percent faster than inflation in 2018-2022, affecting nearly every region. Factors like your home's age, roof condition, proximity to a fire station, and credit-based insurance score all play a role even in lower-risk regions.

Should I lower my coverage to reduce my premium?

Reducing your coverage limits to save money can be a costly mistake. If your dwelling coverage falls below your home's actual rebuild cost, you risk being dangerously underinsured after a major loss, especially given that construction costs have risen 45% since 2020. Instead, focus on strategies that don't compromise protection: raising your deductible, bundling policies, adding discounts, and shopping competing insurers. These approaches can cut your bill significantly without leaving you exposed.