Compare Home Insurance Plans in Ohio

Find your best options in less than 2 minutes

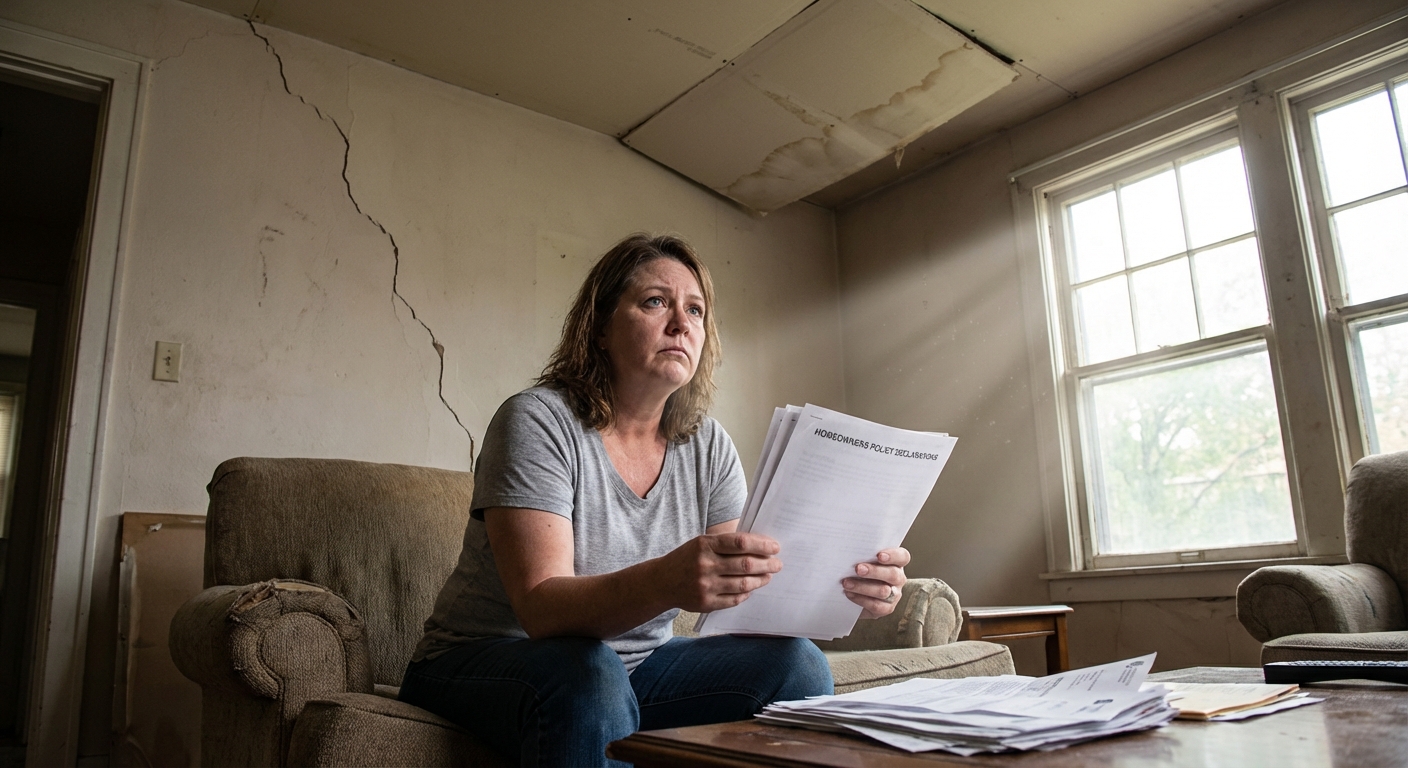

What Does "Underinsured" Mean for Homeowners?

Being underinsured means your home insurance policy is active but does not provide enough coverage to fully pay for rebuilding or repairing your home after a major loss. In other words, the gap isn't that you lack insurance. It's that what you have isn't enough.

This is fundamentally different from being uninsured, where no policy exists at all. An uninsured homeowner has zero financial protection. An underinsured homeowner has a false sense of security: they believe they're protected, but when disaster strikes, they discover their coverage falls thousands of dollars short.

Here's a simple breakdown of the distinction:

For example, if your home would cost $450,000 to rebuild but your policy limit is only $380,000, you are underinsured by $70,000. That $70,000 comes out of your pocket, whether you have the money or not.

How Widespread Is the Problem?

Underinsurance is far more common than most homeowners realize. According to recent LendingTree data, about 12.2 million owner-occupied homes (roughly 1 in 7 households) lack insurance entirely in 2026, and many millions more have policies with insufficient coverage limits. Industry analysts at Realtor.com and Clark Howard warn that a "huge percent" of insured homeowners are also underinsured, primarily because rebuilding costs have outpaced policy limits.

A striking real-world example came after the January 2025 Los Angeles wildfires, which caused over $60 billion in damages and ranked as the costliest wildfire on record. Many homeowners in affected areas learned only after the fact that their coverage limits, set years earlier, would not come close to covering the actual cost to rebuild in a post-disaster market with severe contractor and material shortages.

Home insurance rates have also climbed sharply in recent years, with U.S. premiums rising a cumulative 46.8% from 2020 to 2025. Cotality and Insurify both project another 8% increase in 2026, bringing the national average to roughly $3,250 per year. As rates rise, many homeowners cut coverage limits to lower their premiums, directly worsening the underinsurance problem.

Compare Home Insurance Plans in Ohio

Find your best options in less than 2 minutes

Common Causes of Being Underinsured

Understanding why homeowners end up underinsured is the first step toward fixing it. Here are the four most frequent culprits in 2026:

1. Inflation and Rising Construction Costs

Construction material and labor costs continue to rise. Industry forecasts project U.S. residential construction inflation of about 4 to 5% in 2026, with tariff-related cost increases expected to push metal-intensive trades (steel, copper, aluminum) even higher. From 2020 to 2023 alone, replacement costs for property and casualty losses jumped by an average of 45%. If your policy limits haven't been adjusted in several years, there's a strong chance they no longer reflect what it would actually cost to rebuild today. Learn more about construction cost inflation and home insurance for a deeper look at how these trends affect your coverage.

2. Home Renovations Not Reported to Your Insurer

Did you finish a basement, remodel a kitchen, add a deck, or put in a new bathroom? Every renovation increases the value and rebuild cost of your home. If you didn't notify your insurer and update your policy, your coverage is based on the original home, not the upgraded one. See our guide on home insurance during renovation for what to do before, during, and after major work.

3. Infrequent Policy Reviews

Many homeowners purchase a policy and forget about it for years. Over time, property values shift, construction costs climb, and personal belongings accumulate, none of which are reflected in a stale policy. The Pew Research Center reports that 71% of homeowners say their insurance costs have gone up recently, and many respond by raising deductibles or dropping optional coverages, often without realizing how much risk they're taking on.

4. Coverage Gaps and Policy Misunderstandings

Choosing minimum coverage to save on premiums, relying on actual cash value (ACV) instead of replacement cost value, and overlooking special item riders are all common ways coverage gaps form silently. Many homeowners also confuse market value (what the home would sell for, including land) with replacement cost (what it would cost to rebuild the structure), and insure for the lower market figure. Our guide on rebuild cost vs. home value breaks down this critical distinction.

Protect your home with State Farm

Average Rate:

Homeowners who bundle and save with State Farm save an average of $1,000 per year!

You're in Good Hands® with Allstate

Average Rate:

Get comprehensive home coverage with flexible policy options.

Customize your home coverage

Average Rate:

Only pay for the coverage you need with personalized home insurance.

Smart coverage for your home

Average Rate:

Protect what matters most with award-winning home insurance.

How to Tell If Your Home Is Underinsured

There are no warning lights or notifications when you cross into underinsurance territory. You typically find out only when you file a claim, which is far too late. Here are the most reliable signs to watch for:

| Warning Sign | What to Do |

|---|---|

| Policy hasn't been updated in 3+ years | Request a policy review and rebuilding cost estimate |

| You've completed major renovations | Notify your insurer immediately and update your dwelling limit |

| You have ACV coverage instead of replacement cost | Ask about upgrading to replacement cost coverage |

| High-value items aren't scheduled | Add riders for jewelry, electronics, art, or collectibles |

| You're not sure what your dwelling limit is | Call your insurer and compare it to a rebuild cost calculator |

| You bought minimum coverage to reduce premiums | Recalculate your actual coverage needs with your agent |

The most reliable way to gauge your exposure is to get a professional rebuilding cost estimate or use an online replacement cost calculator to compare your current dwelling limit against what it would actually cost to rebuild your home at today's prices. You can also learn more about ACV vs RCV coverage to make sure your loss settlement method matches your needs.

The Financial Consequences of Being Underinsured

The moment you file a major claim and discover your coverage is inadequate, the financial impact is immediate and significant. A recent Wall Street Journal analysis found that the five largest home insurers failed to pay out on more than 44% of homeowner claims settled in 2025, up from 36% a decade earlier, making adequate coverage limits even more critical.

Out-of-Pocket Repair Costs

The most direct consequence is the difference between what your insurer pays and what repairs actually cost. If your home suffers $300,000 in damage but your policy cap is $250,000, you must cover that $50,000 gap yourself, on top of your deductible. The home insurance coinsurance clause can further reduce your payout if your coverage falls below 80% of replacement cost.

Partial Repairs and Unfinished Rebuilds

When homeowners can't fund the coverage gap, they are often forced into partial repairs, fixing only what the insurance payout covers. This can leave homes structurally compromised, reduce resale value, and create long-term habitability issues.

Long-Term Financial Hardship

Beyond repair bills, underinsurance can lead to debt accumulation, depleted savings, and in severe cases, the loss of the home itself. The emotional weight of navigating a disaster compounds when financial resources fall short of completing recovery.

Understanding how much dwelling coverage you actually need is one of the most important steps you can take to avoid these outcomes.

How to Fix Underinsurance: Practical Solutions

The good news is that underinsurance is entirely preventable. Here are the most effective tools and strategies available to homeowners in 2026.

Replacement Cost Coverage

This is the baseline standard. Unlike ACV policies, replacement cost coverage pays what it actually costs to repair or rebuild using similar materials and quality, without subtracting depreciation. Make sure your policy uses replacement cost, not actual cash value, for both your dwelling and personal property. Compare options in our replacement cost vs. actual cash value guide.

Extended Replacement Cost Coverage

This endorsement adds a buffer, typically 10% to 50% above your dwelling limit, to protect you if rebuilding costs exceed your policy cap after a major disaster. For example, if your dwelling limit is $400,000 and you have 25% extended replacement cost, you're covered up to $500,000. Many carriers use 25% to 50% caps as their standard offering.

Guaranteed Replacement Cost Coverage

The gold standard of home insurance protection, guaranteed replacement cost pays whatever it takes to rebuild your home to its original condition, regardless of how far costs have exceeded your policy limit. This is particularly valuable in areas prone to natural disasters, where post-event rebuilding costs can spike dramatically. Note that this option is no longer universally available, especially in high-risk regions, so check with your carrier. Our guaranteed replacement cost coverage guide covers which insurers still offer it.

Inflation Guard Endorsements

An inflation guard endorsement automatically increases your dwelling coverage limit each year in line with construction cost inflation. Typical adjustments range from 2% to 8% annually. Given that 2025 residential construction inflation was around 5% and 2026 is expected to remain near 4%, an inflation guard with a higher adjustment rate is especially valuable now. Learn more in our inflation guard home insurance guide.

Annual Policy Reviews

Committing to a yearly review of your policy at renewal time is one of the simplest and most effective habits a homeowner can build. Use the review to:

- Update coverage for any renovations completed during the year

- Confirm your dwelling limit matches current rebuild estimates

- Check that personal property limits reflect new purchases

- Verify your additional living expenses coverage is adequate

For older homes or properties with unique features, see our guide on insuring an older home, which often requires special coverage considerations.

Frequently Asked Questions

What is the difference between underinsured and uninsured for home insurance?

An uninsured homeowner has no policy at all, meaning they bear the full financial cost of any damage entirely out of pocket. An underinsured homeowner has an active policy, but the coverage limits are too low to fully cover the cost of repairing or rebuilding after a significant loss. While both situations are financially risky, underinsurance is arguably more deceptive because homeowners believe they are protected when they actually are not. Discovering an underinsurance gap typically only happens at claim time, when it's too late to fix it.

How do I know if my home is underinsured?

The most reliable method is to compare your current dwelling coverage limit against an up-to-date rebuilding cost estimate for your home. You can use an online replacement cost calculator, ask your insurer for an estimate, or hire a professional appraiser. Key warning signs include a policy that hasn't been updated in several years, home improvements that were never reported to your insurer, and coverage based on your home's market value rather than its actual rebuild cost. Reviewing your policy annually is the best way to catch a coverage shortfall before it becomes a problem.

What happens if I'm underinsured when I file a claim?

If your claim exceeds your policy's dwelling limit, your insurer will only pay up to that cap, leaving you personally responsible for the difference. For example, if your home sustains $350,000 in damage but your limit is $275,000, you must cover the $75,000 gap yourself. Coinsurance provisions in some policies can further reduce your payout if your coverage falls below a certain percentage of the home's replacement cost, meaning even smaller claims may not be fully paid.

Does homeowners insurance automatically keep up with inflation?

Not necessarily. Standard homeowners policies do not automatically adjust to rising construction costs unless you have an inflation guard endorsement. With residential construction inflation projected near 4 to 5% in 2026, a static dwelling limit can lag actual rebuild costs by 8 to 10% over just two years. Even with an inflation guard, the annual adjustment percentage may not fully keep pace with sharp, rapid increases in construction costs, so an annual policy review remains important.

Is guaranteed replacement cost worth the extra premium cost?

For most homeowners, guaranteed replacement cost coverage is one of the most valuable endorsements available, particularly in high-risk areas or regions prone to natural disasters. After events like the 2025 Los Angeles wildfires, demand for contractors and materials can push rebuilding costs far above normal estimates, and guaranteed replacement cost ensures you're protected regardless of how high those costs climb. Note that GRC is no longer offered by all insurers, especially in wildfire-prone or hurricane-prone regions, so check availability with your carrier before relying on it.