Ohio Life Insurance - Save up to 70% Off

See what plans you qualify for in just a few minutes

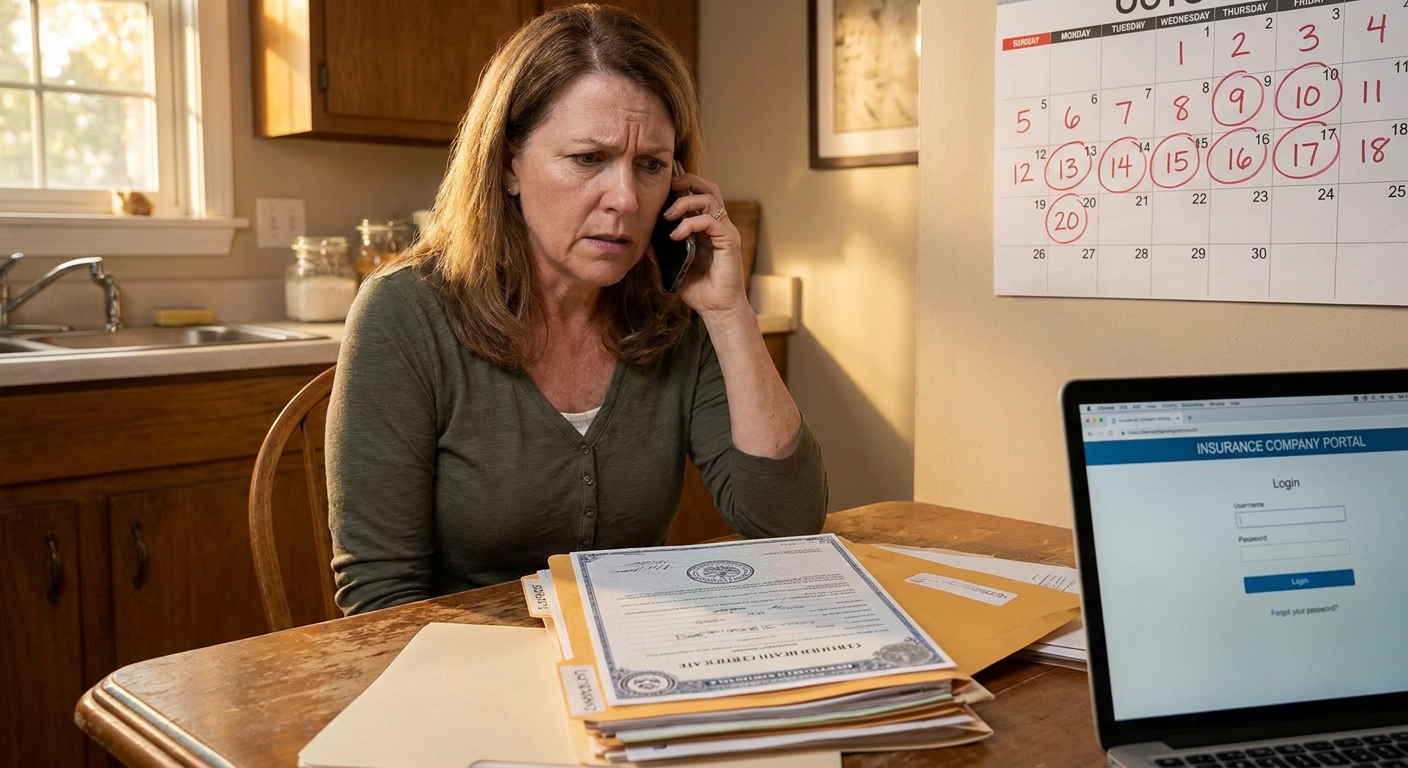

Understanding Life Insurance Claim Timelines

When a loved one passes away, the last thing you want is to battle an insurance company for months over a payout. Understanding what a normal timeline looks like, and what counts as an unreasonable delay, is the first step to protecting your rights as a beneficiary.

Standard Processing: 14 to 60 Days

For straightforward claims with complete documentation, most life insurance companies resolve payouts within 14 to 60 days of receiving the claim. According to 2026 industry data, roughly 72% of clean claims are paid within 10 business days, and simple cases with no red flags can sometimes be paid in as few as 3 to 5 business days. The industry benchmark most insurers aim for is 30 days from the date all required documents are submitted.

The key factors that enable fast processing:

- A certified copy of the death certificate

- A fully completed claim form

- Valid proof of the beneficiary's identity

- A clean, in-force policy with no coverage gaps

- No suspicious circumstances surrounding the death

Extended Delays: When 6+ Months Is the Reality

Certain situations push claims into extended territory, ranging from three months to over a year. While frustrating, some of these delays are legally permitted when investigations are actively underway. A delay of 6 to 12 months may still be considered acceptable if the insurer is conducting a legitimate investigation, particularly for large death benefits or policies under two years old. Term life claims involving medical exam reviews now average about 45 to 55 days industry-wide.

Any delay exceeding 30 days without a written explanation is a signal worth noting, and delays beyond 90 days with no resolution deserve serious scrutiny. A 2025 Wall Street Journal report highlighted a growing trend of insurers stalling payouts by citing "administrative reviews" or outdated documents, leaving families waiting months longer than needed.

| Timeline | What It Typically Means |

|---|---|

| 3-30 days | Fast-tracked, simple claim |

| 30-60 days | Standard processing |

| 60-90 days | Minor complications or missing documents |

| 3-6 months | Active investigation underway |

| 6-12 months | Complex investigation (contestability, fraud review) |

| 12+ months | Potential bad faith, consider escalating |

Ohio Life Insurance - Save up to 70% Off

See what plans you qualify for in just a few minutes

What Triggers a Life Insurance Claim Investigation

Not every claim is paid automatically. Insurers flag certain situations for deeper review before releasing funds. Knowing what raises a red flag can help you understand why your claim may be taking longer than expected. Learn more about the contestability period rules for a deeper dive on one of the most common investigation triggers.

The 2-Year Contestability Period

This is the single most common trigger for a claim investigation. If the insured person dies within the first two years of the policy being issued, the claim is subject to automatic review. During this window, the insurer has the legal right to examine the original application in detail, cross-referencing it against medical records, pharmacy databases, and physician notes.

If a material misrepresentation is found, even one unrelated to the cause of death, the insurer can rescind the policy and deny the claim. For example, if the insured failed to disclose a pre-existing heart condition but died in a car accident, the claim can still be denied if the omission was material to the underwriting decision. The good news: industry attorneys report that most claims filed during the contestability period are ultimately paid after review, not denied outright.

The Suicide Clause

Most policies include a 1 to 2 year suicide exclusion from the date of issuance. If the cause of death is determined or suspected to be suicide within that window, the insurer will typically deny the full death benefit and refund premiums paid. After the exclusion period expires, suicide is generally covered under standard life insurance. Claims where the cause of death is ambiguous, such as a drug overdose, may trigger toxicology reviews and autopsy requests to determine intent.

Other Common Investigation Triggers

A contested life insurance claim, where multiple parties are asserting rights to the death benefit, can also push a payout into limbo for months or even years until the dispute is legally resolved. Deaths that occur outside the U.S. also routinely trigger delays because insurers require additional foreign documentation.

How to Speed Up Your Life Insurance Claim

The good news: beneficiaries have more control over claim speed than most people realize. Taking the right steps early can dramatically reduce processing time.

Step 1: File Immediately and File Complete

The single most effective thing you can do is submit a fully complete claim package right away. Incomplete submissions and missing beneficiary information cause an estimated 15% of all claim delays. Before you send anything, gather:

- Certified death certificate (get multiple copies, you may need them)

- Completed claim form from the insurer

- Copy of the original policy (or policy number if the document is lost)

- Government-issued ID for the beneficiary

- Any supporting documents the insurer requests upfront

Learn more about the full step-by-step claim filing process and review the complete beneficiary guide to make sure nothing gets missed.

Step 2: Respond Instantly to Insurer Requests

Every time the insurer sends a request for additional information, the internal clock often resets. Respond to every request within 24 to 48 hours if possible. Keep copies of everything you send, and send via methods that create a paper trail (email, certified mail, or insurer portal uploads).

Step 3: Know Your State's Prompt Payment Law

Every U.S. state except South Carolina has a prompt payment law that requires insurers to acknowledge, investigate, and pay claims within specific timeframes. These laws create legal accountability. Here's how some major states handle it in 2026:

| State | Acknowledgment Deadline | Payment Deadline | Penalty for Late Payment |

|---|---|---|---|

| Texas | 15 business days | 5 business days after acceptance | 18% annual interest + attorney fees |

| Texas (adverse claims) | Standard | 90 days to pay or interplead | 18% interest under §542.060 |

| California | Prompt / reasonable time | Prompt / reasonable time | Interest + potential punitive damages |

| Florida | Within statutory window | 30-60 days after proof of death | Statutory interest accrues |

| New York | Prompt / reasonable time | Prompt after proof of death | Mandatory interest per DFS rules |

Texas has one of the strictest frameworks in the country. Under Insurance Code Chapter 542, insurers who miss any of the three key deadlines (15 business days to acknowledge, 15 business days to accept or deny, and 5 business days to pay after acceptance) automatically owe 18% annual penalty interest plus attorney fees.

Step 4: Escalate When Necessary

If your claim is stalled without a clear explanation, here's how to escalate:

Day 30-60: Contact your insurer in writing and request a status update with a specific explanation for the delay.

Day 60+: File a complaint with your State Department of Insurance. Include your claim submission date, all correspondence, and documentation showing the delay. Regulators take prompt payment violations seriously.

Day 90+: Consult a life insurance attorney. Many offer free consultations, and in states like Texas and California, attorneys can recover their fees from the insurer if bad faith is proven.

Claim Denials vs. Delays: Knowing the Difference & Your Rights

A delay means the insurer is still processing your claim. A denial means the insurer has formally refused to pay. Knowing which situation you're in matters, because they require very different responses. Encouragingly, roughly 40% of denied claims are overturned on appeal, so it is often worth fighting back. If your claim has been denied, read our guide on what to do after a denial to understand your appeal rights.

Warning Signs of an Improper Delay

Not all delays are legitimate. Watch for these red flags that may signal bad faith conduct:

Recent high-profile litigation illustrates why this matters. In 2025, an Arkansas class action accused Globe Life of using an "outlawed Good Faith Defense" to rescind policies for irrelevant health disclosures. A separate Massachusetts court in late 2025 ordered three Liberty insurers to pay nearly $91 million for unfair settlement practices, one of the largest bad-faith awards of the year.

Beneficiary Rights You Should Know

- You have the right to a written explanation for any denial or delay

- You have the right to appeal a denial, and most insurers must maintain a formal appeals process

- You have the right to file a complaint with your state insurance regulator at any time

- If the insurer is acting in bad faith, you may be entitled to damages beyond the policy amount, including interest, attorney fees, and in some states, punitive damages

Keeping your beneficiary designations up to date and avoiding common beneficiary mistakes are two of the most proactive ways to prevent future claim complications before they happen. Reviewing your life insurance payout options and understanding what a policy actually covers can also protect your family from surprises down the line.

Frequently Asked Questions

How long does a life insurance claim typically take to pay out?

Most straightforward life insurance claims are processed within 14 to 60 days of the insurer receiving a complete claim package, and roughly 72% of clean claims settle within 10 business days. Simple cases with no red flags can sometimes pay out in as few as 3 to 5 business days. However, claims involving investigations, beneficiary disputes, or policies in the contestability period can take anywhere from 3 months to over a year. The speed largely depends on how quickly you submit complete documentation.

Why is my life insurance claim taking so long?

The most common reasons include incomplete documentation, a death that occurred within the policy's 2-year contestability period, a pending investigation into the cause of death, a beneficiary dispute, or a large death benefit that requires additional review. In some cases, insurers are legally required to investigate before paying. If you haven't received a clear written explanation after 30 days, contact your insurer in writing and ask for a specific status update.

What happens if a life insurance claim is under investigation?

When a claim is under investigation, the insurer may request medical records, autopsy reports, toxicology results, or police reports before making a payout decision. Investigations are common for policies less than two years old, large death benefits, or deaths from unclear causes. They can extend the timeline significantly, from a few months to over a year. Cooperate fully with any information requests, but consult an attorney if the investigation appears to be dragging on unreasonably.

Can a life insurance company deny a claim after years of paying premiums?

Yes, most commonly during the contestability period or if a policy exclusion applies. However, once a policy is past the 2-year contestability window and all premiums are current, it becomes much harder for an insurer to deny a claim. Application misrepresentation is the most common basis for post-payment denial, accounting for roughly 2 to 2.6% of all life claim denials in 2026. If you believe a denial is unjustified, you have the right to formally appeal and can escalate to your state insurance department or hire an attorney.

When should I hire an attorney for a delayed life insurance claim?

Consider consulting an attorney if your claim has been delayed beyond 90 days without a satisfactory explanation, if the insurer has formally denied the claim and you believe it's unjustified, or if you're seeing warning signs of bad faith conduct. Many life insurance attorneys offer free initial consultations and work on contingency. In several states, if the insurer is found to have acted in bad faith, they may be required to pay your attorney fees in addition to the claim amount and any accrued interest.