Ohio Life Insurance - Save up to 70% Off

See what plans you qualify for in just a few minutes

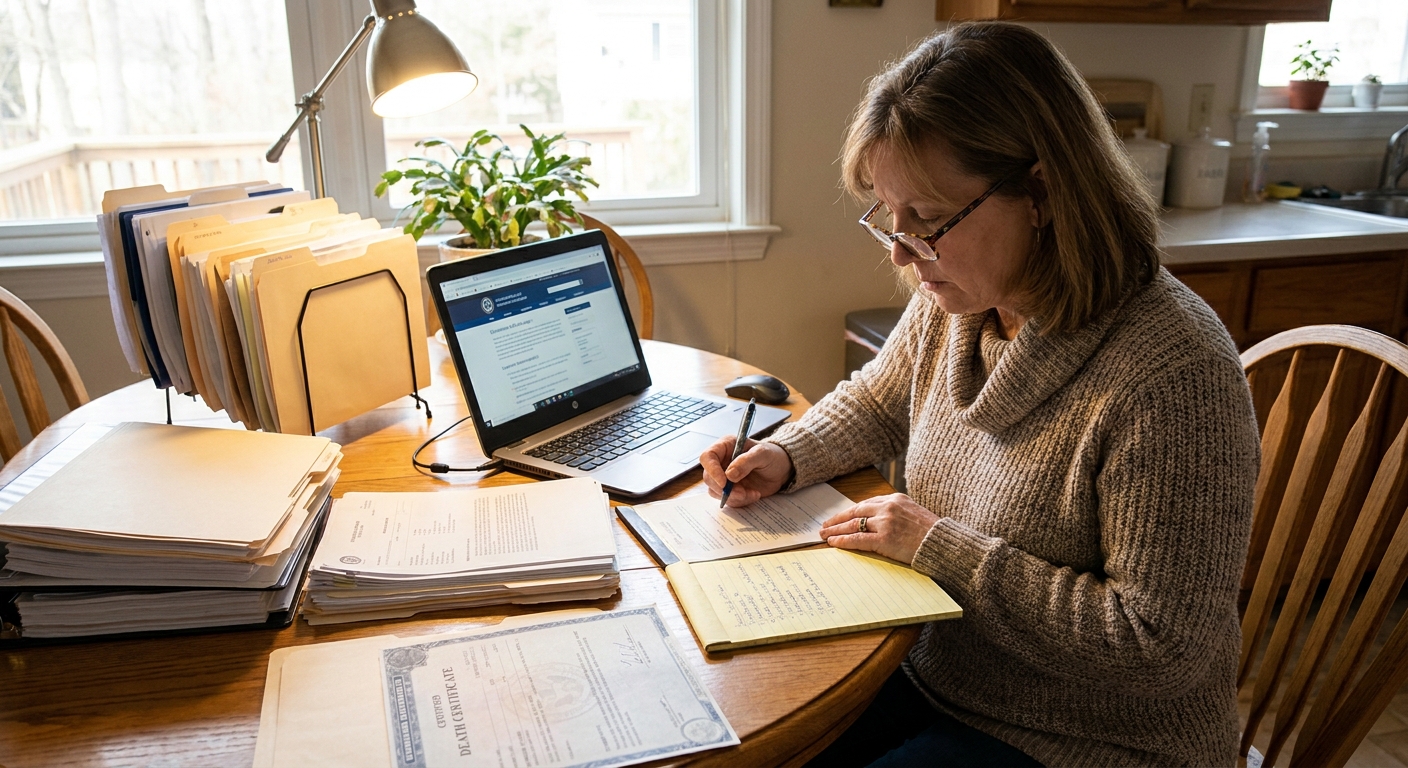

The NAIC Life Insurance Policy Locator Service

The NAIC Life Insurance Policy Locator (LIPL) is the most powerful free tool available for finding a lost or missing life insurance policy. Operated by the National Association of Insurance Commissioners, this secure online service has already helped consumers connect with more than $13.18 billion in unclaimed life insurance and annuity benefits as of August 31, 2025, based on over 611,000 policy matches and 1.17 million total search requests since its 2016 launch. Best of all, it searches the records of participating insurance companies nationwide at no cost to you.

How It Works

The LIPL is designed exclusively for searches on behalf of deceased individuals. It cannot be used to locate a living person's policies. Here's how to use it step by step:

- Visit the NAIC website at naic.org and navigate to Consumer Tools > Life Insurance Policy Locator.

- Create a secure account with your name, mailing address, email, and a password.

- Agree to the terms of use on the welcome page.

- Submit a search request by entering the following information (ideally from the certified death certificate):

| Required Field | Details |

|---|---|

| Deceased's Legal Full Name | Include any maiden name or former names |

| Social Security Number (SSN) or ITIN | The 9-digit SSN or ITIN of the deceased |

| Date of Birth | MM/DD/YYYY format |

| Date of Death | MM/DD/YYYY format |

| Your Relationship to Deceased | Spouse, child, executor, etc. |

| Veteran Status | Yes or No |

| Last Known Address | Helps insurers narrow their search |

- Submit your request. You'll receive a "Do Not Reply" confirmation email immediately.

- Wait for results. Participating insurers search their own records. If a match is found and you are the named beneficiary or legal representative, the insurer will contact you directly, typically within 90 business days.

When to Use the NAIC Locator

- After the death of a spouse, parent, or other loved one

- During estate settlement when insurance is suspected but undocumented

- When going through financial records and finding premium payments to an unknown insurer

- When you suspect a policy exists but don't know which insurer wrote it

For a full walkthrough of what happens next, see our life insurance beneficiary guide.

Ohio Life Insurance - Save up to 70% Off

See what plans you qualify for in just a few minutes

State Unclaimed Property Databases and Other Search Tools

When unclaimed life insurance benefits go uncontacted for a number of years, insurance companies are required by law to turn those funds over to the state government through a process called escheatment. Most states apply a 3-year or 5-year dormancy period once benefits become due and payable, though some states (like California, Florida, Nevada, New York, and Oregon) now trigger the clock as soon as the insurer knows, or should have known, about the policyholder's death. Every state maintains an unclaimed property database, and these databases are searchable for free.

How to Search Unclaimed Property Databases

Step 1: Visit MissingMoney.com, a free multi-state search tool sponsored by the National Association of Unclaimed Property Administrators (NAUPA). This single tool searches participating states simultaneously, and NAUPA estimates state treasuries collectively hold over $80 billion in unclaimed property of all types, with life insurance and annuities among the largest categories.

Step 2: Visit your state's official unclaimed property website directly. Search using:

- The deceased's full legal name (including maiden or former names)

- City or state of last known residence

Step 3: If a match is found, submit a claim through the official state portal. You'll typically need a certified death certificate and proof of your legal right to claim the funds.

States With Their Own Life Insurance Locator Tools

Six states run dedicated free life insurance policy search services in addition to the NAIC national locator: Illinois, Louisiana, Michigan, New York, North Carolina, and Oregon. New York's Lost Policy Finder, for example, is operated by the Department of Financial Services and queries all New York-licensed life insurers on behalf of the requester. Check your state's Department of Insurance website to see if a state-run service is available.

The MIB Group Policy Locator Service

The MIB Group (formerly the Medical Information Bureau) is a data solutions provider that serves the life insurance industry. Its Policy Locator Service searches life insurance application records from approximately 420 MIB member carriers in the U.S. and Canada, covering applications submitted from January 1, 1996 to the present.

To use the MIB service, visit policylocator.com and submit a notarized application along with an original death certificate and the $75 non-refundable fee (typically by money order or bank certified check). Results include the carrier name(s), application date(s), and contact information for insurers where the decedent applied for coverage. Keep in mind the service confirms only that an application was submitted, not that a policy was issued or is still in force, and it does not provide beneficiary information.

How to Search Personal Records for a Missing Policy

Before or alongside using online locator tools, searching through a deceased person's personal and financial records is one of the most effective ways to uncover a life insurance policy. Here's where to look:

Tax Returns

Review the last 2 to 3 years of federal income tax returns (Form 1040). Look for:

- Interest income from life insurance companies, which can indicate a whole or universal life policy building cash value

- Interest expenses or deductions associated with policy loans

- Premium payments listed among financial records or expenses

Contact the deceased's accountant or tax preparer directly, as they may know of policies you don't.

Bank Statements and Canceled Checks

Pull 2 to 3 years of bank statements and look for:

- Recurring payments to insurance company names (e.g., MetLife, Prudential, New York Life)

- Automatic premium debits from checking or savings accounts

- Dividend deposits from a life insurer (common with whole life policies covered in our permanent life insurance guide)

Safe Deposit Boxes

Safe deposit boxes are a common storage place for important documents. To gain access as an executor or beneficiary, bring a certified death certificate to the bank. In some states, a court order may be required.

Employer and HR Records

Many people carry group life insurance through their employer, and some coverage continues into retirement. Learn more about group vs. individual coverage options, then contact the HR or benefits department at:

- Current or most recent employer

- Previous long-term employers

- Unions or professional associations the deceased belonged to

Mail and Email Records

Check both physical mail and email accounts for:

- Annual policy statements

- Premium billing notices

- Dividend or interest notices from insurers

Financial Advisor and Attorney Records

If the deceased worked with a financial planner, estate attorney, or CPA, contact them directly. These professionals often maintain records of insurance policies purchased as part of an estate plan, including policies held inside an ILIT.

What to Do Once You Find a Life Insurance Policy

Once a policy has been located, whether through the NAIC, a state database, personal records, or MIB, the next step is filing a life insurance claim with the insurer. Here's how to move forward:

Step-by-Step Claims Process

| Step | Action |

|---|---|

| 1 | Obtain multiple certified copies of the death certificate |

| 2 | Contact the insurance company's claims department |

| 3 | Request and complete a beneficiary claim form |

| 4 | Submit all documents (death certificate, claim form, your ID) |

| 5 | Choose your payout option: lump sum or structured payments |

| 6 | Follow up and track your claim status |

Most standard claims are paid within 14 to 60 days of receiving complete documentation, though contested cases or policies within the two-year contestability period may take longer.

Frequently Asked Questions

How long does the NAIC Life Insurance Policy Locator take to get results?

The NAIC asks that you allow 90 business days for participating insurance companies to search their records. This timeline exists because insurers must independently search their own databases and reach out to beneficiaries directly. If you don't hear from an insurer after 90 business days, it likely means no matching policy was found, or that you are not the listed beneficiary or legal representative on the policy.

Can I search for a life insurance policy if the person is still alive?

The NAIC Life Insurance Policy Locator is designed only for searches involving deceased individuals. If you're trying to locate your own policy or verify coverage while you're alive, start by contacting insurers directly or reviewing your own financial records, tax returns, and employer benefits statements. You may also request your personal MIB Consumer File once every 12 months for free at mib.com to see a history of insurance applications made in your name.

What information do I need to search for a lost life insurance policy?

At minimum, you'll need the deceased's full legal name (including any maiden or former names), Social Security number, date of birth, and date of death. Having a certified copy of the death certificate is essential for submitting claims once a policy is found. Knowing the deceased's states of residence and veteran status can also help when searching state-level unclaimed property databases and the NAIC locator.

What happens if a life insurance policy goes unclaimed?

When a life insurance policy goes unclaimed, the insurer is legally required to turn the funds over to the state government through a process called escheatment. Most states apply a 3-year or 5-year dormancy period once benefits become due and payable, though states like California, Florida, and New York now use the policyholder's date of death as the trigger. The money is then held in the state's unclaimed property fund indefinitely and can be claimed by rightful heirs through MissingMoney.com or the state's official unclaimed property office.

Can I search for a life insurance policy by Social Security number?

Yes. The NAIC Life Insurance Policy Locator and the MIB Group Policy Locator both use the deceased's Social Security number as a primary identifier when searching insurer records. This is one of the most reliable ways to match a person to a policy, especially if there are variations in how a name was recorded. Always use the deceased's full 9-digit SSN as it appears on official government documents.