Ohio Life Insurance - Save up to 70% Off

See what plans you qualify for in just a few minutes

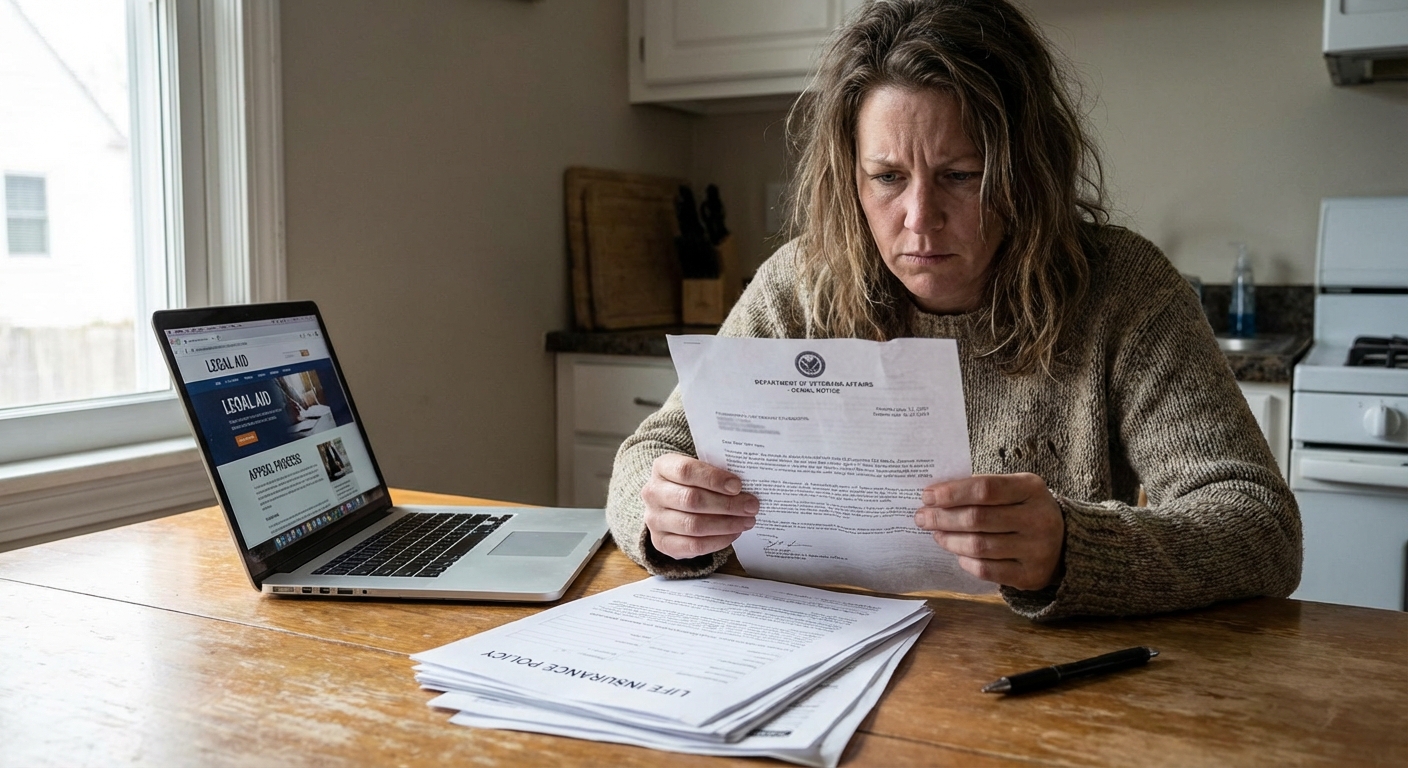

The Most Common Reasons a Life Insurance Claim Gets Denied

Receiving a life insurance claim denial is one of the most frustrating and devastating things a grieving family can face. While outright denials are rare (industry data shows only about 1.9% to 2.6% of claims are ultimately denied and never paid), they still happen, and the consequences are enormous. Industry analysts estimate that roughly 10% to 20% of life insurance claims encounter an initial denial, extended investigation, or major rejection in 2026. Understanding why insurers deny claims is the first step toward fighting back, or preventing the problem entirely.

Material Misrepresentation on the Application

Material misrepresentation remains the #1 reason life insurance claims are denied in 2026. This occurs when an applicant provides false, incomplete, or misleading information on their life insurance application that the insurer considers significant enough to have changed their underwriting decision. Historical NAIC research found that approximately 56% of denied or "resisted" claims were due to material misrepresentation, and even unintentional omissions can give an insurer grounds to void a policy and deny a claim.

Common things people misrepresent on applications include:

| Category | Examples |

|---|---|

| Health & Medical History | Undisclosed pre-existing conditions, medications, diagnoses, mental health treatment |

| Lifestyle Habits | Claiming non-smoker status while smoking, alcohol use, drug use |

| Risky Activities | Concealing hobbies like skydiving, motorsports, or rock climbing |

| Occupation | Understating the dangers of a high-risk job |

| Existing Policies | Failing to disclose other life insurance policies in force |

Policy Lapse, Non-Payment & the Contestability Period

Lapsed policies are another leading cause of denial. If you miss premium payments and your policy lapses past the grace period, your coverage simply ends. Industry data indicate that lapse in premium payment causes about 25% of denials, and insurers will deny any claim where the policy was not active at the time of death.

Equally important is the life insurance contestability period, which is still two years in 2026 across all 50 states. During this two-year window, insurers can investigate the accuracy of your application, and material misrepresentation could result in claim denial or benefit reduction. Notably, misstatements do not have to be related to the cause of death to matter during this period, they only need to be material to underwriting. If the insured passes away during this period, the claim is not automatically paid. Carriers routinely conduct a contestability audit if death occurs within 24 months, scrutinizing the application using medical records, prescription histories, MIB reports, and increasingly AI-driven data cross-checks that automatically flag inconsistencies between application answers and third-party data. Learn more about how life insurance payouts work and what beneficiaries should expect during this process.

Other "Policy Not in Force" Scenarios

- The term policy expired before the insured's death

- A lapse occurred and reinstatement was never completed (reinstatement restarts a new contestability period)

- Premiums were returned or the policy was canceled

- Coverage changed materially (a large face-amount increase can trigger a new contestability window on the added coverage)

Excluded Causes of Death & the Suicide Clause

Most life insurance policies contain specific exclusions your policy won't cover, causes of death that are simply not covered. These are clearly outlined in the policy language, though many policyholders never read the fine print.

The life insurance suicide clause is one of the most commonly misunderstood exclusions. Nearly all policies exclude suicide during the first two years of coverage, though a small but growing group of states now caps this window at just one year, including Colorado, Minnesota, Missouri, North Dakota, and Washington under SB 5495 for policies issued or renewed on or after January 1, 2026. Suicide historically accounts for around 14% of denied claims per recent industry analysis. After the exclusion window, life insurance generally does cover suicide, and the death benefit is paid normally. Learn more about the life insurance suicide clause and how state laws differ.

Other commonly excluded causes of death include:

- Death during the commission of a crime or felony

- Death from undisclosed high-risk activities (e.g., private aviation, skydiving)

- Alcohol or drug-related deaths (if substance abuse was undisclosed)

- Acts of war, terrorism, or armed conflict (varies by policy)

Learn more about what life insurance actually covers to understand the full scope of your policy.

Beneficiary Issues & Fraudulent Claims

Even when a death is clearly covered, a claim can be denied due to problems with the beneficiary designation or outright fraud. Beneficiary disputes delay roughly 10% of claims by 60 days or more, and beneficiary disputes have been a growing source of denied or delayed claims in recent years, particularly with employer-provided group policies.

Common beneficiary-related issues include:

- No named beneficiary (benefits may be paid to the estate and face probate delays)

- Deceased beneficiary (if the named beneficiary predeceased the insured with no contingent beneficiary named)

- Vague designations (using terms like "my children" without legal names can cause disputes)

- Homicide by a beneficiary (in all U.S. states, a beneficiary found responsible for the insured's death is legally barred from collecting)

Fraudulent claims are investigated aggressively. Fraud accounts for approximately 2.3% of claim denials, and these cases can also result in criminal charges. Avoid common life insurance beneficiary mistakes to protect your family from unnecessary delays.

Ohio Life Insurance - Save up to 70% Off

See what plans you qualify for in just a few minutes

What To Do If Your Life Insurance Claim Is Denied

A denial is not the end of the road. Beneficiaries have the legal right to appeal, and many denials are successfully overturned. In fact, roughly 40% of appealed life insurance denials are overturned in the beneficiary's favor. Here's exactly what to do.

Step 1: Review the Denial Letter Carefully

The insurer is legally required to provide a written explanation of the denial. Under federal regulations at 29 CFR 2560.503-1, the insurer must provide specific reasons for the denial (not vague statements like "insufficient medical evidence"), reference the exact plan provision relied upon, describe additional material needed to perfect the claim, and explain your appeal rights. Read the letter thoroughly to identify:

- The specific reason(s) for the denial

- References to policy exclusions or clauses cited

- The appeal deadline (typically 60 to 180 days from the denial date)

Step 2: Gather Your Documentation

Build a strong file of evidence to support your appeal:

- A certified copy of the death certificate

- The original life insurance policy

- All premium payment records

- Medical records relevant to the denial reason

- All written correspondence with the insurer

- Any new evidence that directly contradicts the denial reason

For a full breakdown of required paperwork, see our guide on how to file a life insurance claim.

Step 3: File a Formal Appeal

Your appeal letter should be detailed, professional, and directly address each stated reason for denial using policy language and supporting evidence. If the policy was employer-provided, it is likely governed by ERISA, which has its own strict appeal rules. For non-health, non-disability welfare claims like life insurance, a benefit determination is generally due within a reasonable period, not later than 90 days after receipt, with one 90-day extension for special circumstances. ERISA requires a "full and fair review." Most ERISA group life policies allow between 60 and 180 days to file an appeal, and the appeal clock almost always begins on the date of the denial letter, not the date you received it. The administrative record closes after the final internal appeal, so any evidence not submitted by then will likely be excluded from federal court.

Step 4: Contact Your State Insurance Commissioner

If you believe the denial is unjustified, file a complaint with your state's Department of Insurance. Regulators can investigate insurer conduct, apply pressure, and in some cases facilitate a resolution without requiring a lawsuit. Most states publish online complaint portals, and complaints are typically acknowledged within a few business days.

Step 5: Consider Hiring an Attorney

If your appeal is denied or the denial involves complex legal issues, consult a life insurance attorney who specializes in claim disputes. Many work on contingency, meaning you pay nothing unless they recover benefits for you. An experienced attorney can evaluate whether the denial was wrongful and build a case for litigation.

When Bad Faith Denial May Apply

If an insurer unreasonably denies a valid claim, delays payment without cause, misrepresents policy terms, or ignores supporting evidence, this may constitute bad faith, a legal violation of the insurer's duty to deal fairly. Courts, however, are increasingly applying a "fairly debatable" standard, meaning if the insurer had any reasonable basis for its position, bad faith claims may be dismissed. Still, recent verdicts show juries willing to award enormous damages where insurer conduct is egregious. In a 2025 landmark bad faith case, a Colorado jury awarded $145.26 million to Fermin Salguero-Quijada, a construction worker who suffered a traumatic brain injury after falling from a ladder in 2021, including $60 million in punitive damages. In another high-profile ruling, Sierra Health and Life Ins. Co. v. Eskew, the Nevada Supreme Court upheld a $200 million verdict against a health insurer ($40 million compensatory plus $160 million punitive) for bad faith refusal to cover lung cancer treatment. Successful bad faith lawsuits can result in:

- Payment of the full death benefit plus interest

- Compensatory damages for losses caused by the delay

- Damages for emotional distress and mental anguish

- Punitive damages for egregious conduct (which can equal or exceed compensatory damages in some states)

- Attorney's fees and court costs

Document every interaction with the insurer from the moment of denial. This paper trail is critical if litigation becomes necessary. Learn more about handling life insurance claim settlement delays if payment is dragging.

Tips for Preventing a Life Insurance Claim Denial

The best time to protect your beneficiaries is before anything goes wrong. Follow these proactive steps:

- Be 100% honest on your application. Disclose all medical conditions, medications, lifestyle habits, and risky hobbies, even if it costs more upfront.

- Pay premiums on time, every time. Set up automatic payments to prevent an accidental lapse. If you miss a payment, contact your insurer immediately. Most have a 30 or 31-day grace period.

- Name specific beneficiaries. Use full legal names and always designate a contingent (backup) beneficiary in case your primary beneficiary predeceases you.

- Update your beneficiary designations regularly, especially after major life events like marriage, divorce, or the birth of a child.

- Tell your beneficiaries where the policy is stored. A claim that is never filed is a benefit never paid. See our complete guide for life insurance beneficiaries so your loved ones are prepared.

- Read your policy. Understand your exclusions, the contestability period, and any riders or special clauses.

Frequently Asked Questions

Can a life insurance company legally deny a claim?

Yes, life insurance companies can legally deny claims under certain circumstances defined in the policy contract and state law. Common legal grounds for denial include material misrepresentation on the application, a lapsed policy due to non-payment, death from an excluded cause, or a claim filed during the 2-year contestability period where inaccuracies are found. However, the insurer must have a legitimate, documented reason and bears the burden of proof. Arbitrary or bad-faith denials are illegal and can be challenged in court, and recent 2025 and 2026 verdicts show courts continue to punish insurers with substantial punitive damages for unjustified denials.

How long does a life insurance company have to pay or deny a claim?

State laws vary, but most states require life insurance companies to pay claims within 30 to 60 days of receiving proof of death and all required documentation. California, for example, requires insurers to acknowledge a claim within 15 days and accept or deny within 40 days of receiving proof of loss, with interest accruing from the date of death if payment is delayed. Under ERISA, insurers generally have up to 90 days to make an initial claim decision on a life insurance claim, with one possible 90-day extension for special circumstances.

What happens if life insurance is denied due to misrepresentation?

If a claim is denied due to material misrepresentation, the insurer will typically void the policy and refund the premiums paid, but will not pay the death benefit. Beneficiaries have the right to appeal if they believe the insurer's claim of misrepresentation is inaccurate or immaterial. Consulting a life insurance attorney is strongly recommended in these cases, as the insurer bears the burden of proving the misrepresentation was truly material to their underwriting decision.

How long do I have to appeal a denied life insurance claim?

Appeal deadlines vary by policy type. For individual policies, the window is often 60 to 180 days from the denial date, as stated in the denial letter. For ERISA group life policies, most plans allow between 60 and 180 days to file an appeal, and the clock usually begins on the date printed on the denial letter, not the date you received it. Missing this deadline can permanently forfeit your right to appeal and even to sue in federal court, so act quickly and request an extension in writing if you need more time.

What is a wrongful life insurance claim denial?

A wrongful denial occurs when an insurer denies a valid claim without a legitimate contractual or legal basis. This includes denials based on incorrect policy interpretation, minor or immaterial application errors, or deliberately ignoring evidence that supports the claim. Wrongful denials may also rise to the level of bad faith, which opens the insurer to additional legal liability beyond simply paying the death benefit, including emotional distress damages, punitive damages, and attorney's fees in many states.