Ohio Life Insurance - Save up to 70% Off

See what plans you qualify for in just a few minutes

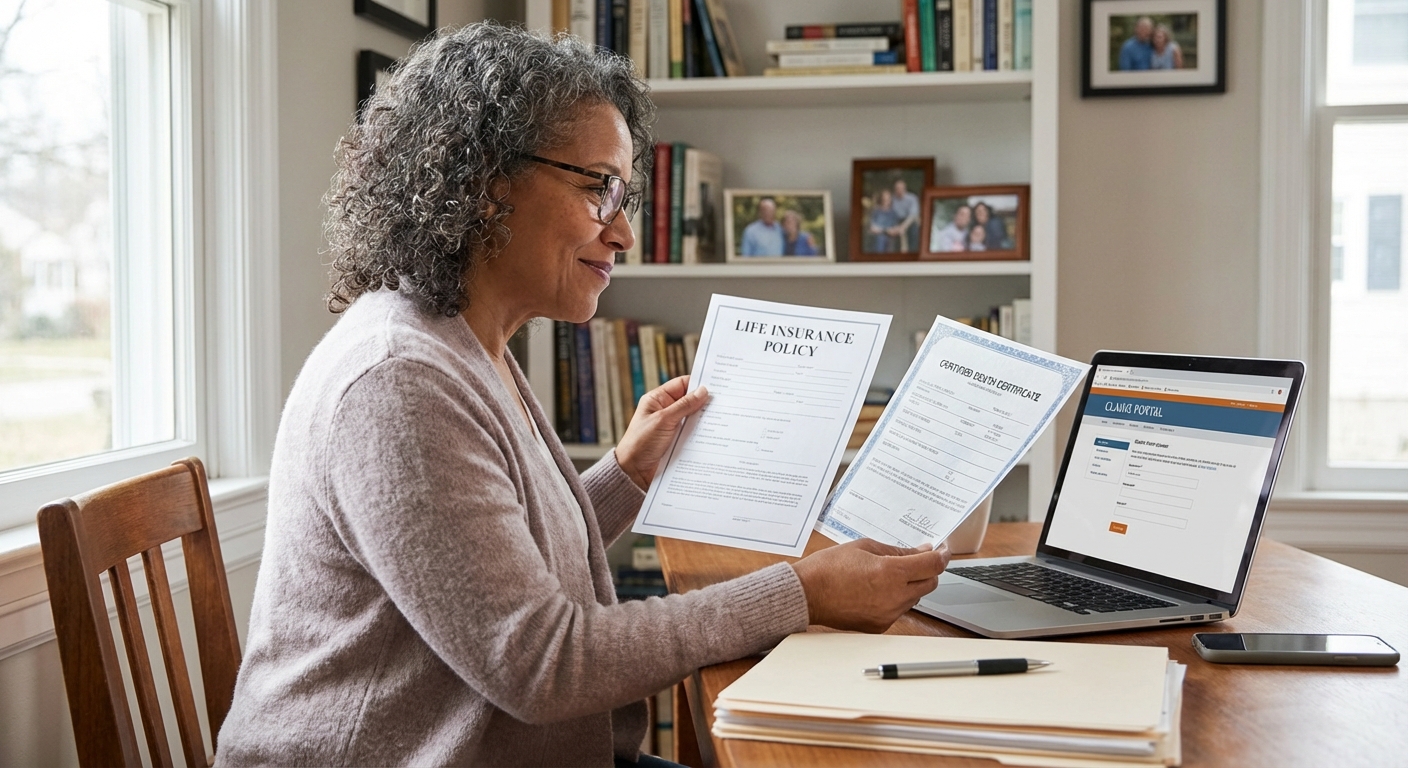

Filing a Life Insurance Claim

Required Documentation

Filing a life insurance claim requires several key documents. The certified death certificate is the most critical document, showing the cause and manner of death. Beneficiaries should obtain multiple copies from vital records offices or the funeral home. For benefits exceeding $100,000 to $500,000, insurers typically require original certificates, while smaller claims may accept copies.

Additional required documents include completed claim forms from the insurer and the policy number or policy document if available. Depending on the beneficiary type, you may need proof of relationship to the insured, tax identification numbers for trusts or estates, or affidavits for minors or heirs. For a complete list, see our life insurance application checklist.

Step-by-Step Claim Process

The claim process begins by contacting the insurance company promptly after the insured's death. You'll need to provide basic information including the policy number, insured's name, date of birth, and your relationship to the deceased. The insurer will send a personalized claims kit with specific forms.

Next, gather all required documents, particularly the certified death certificate. Complete all claim forms in the kit with your personal details such as name, address, Social Security number, and relationship to the insured. For trust or estate beneficiaries, include entity-specific information like trust dates and tax IDs. Learn more about filing a life insurance claim step by step.

Submit your completed documents through the insurer's preferred method, which may include online portals, email, fax, or mail. Typically, only one death certificate is needed even for multiple beneficiaries or policies. Most insurers process complete claims within 14 to 60 days, though timelines vary based on documentation quality and claim complexity. Our beneficiary guide walks through what happens after you submit.

Ohio Life Insurance - Save up to 70% Off

See what plans you qualify for in just a few minutes

Typical Payout Timeline

Standard Processing Time in 2026

Life insurance death benefit payouts typically take 14 to 60 days after filing a complete claim. Most straightforward cases (a policy in good standing, clear cause of death, and complete paperwork) are paid within 7 to 30 days of receiving a complete claim submission. For clean claims paid via electronic funds transfer, payouts can occur as quickly as 3 to 5 days. Industry data continues to show that the vast majority of filed claims are ultimately paid, with LIMRA studies putting the final denial rate at just 1.9%.

The industry follows a "30-day rule" as a standard benchmark: once a life insurance company receives a completed claims package, it generally has around 30 days to review documentation, verify the policy and death, and make a formal decision. Most states require insurers to pay a completed claim within about 30 days or begin accruing interest on the unpaid benefit. Every state also requires carriers to act in good faith and with reasonable promptness when handling claims.

Common Reasons for Delays

Several factors can extend the payout timeline beyond the standard window. Delayed or incomplete paperwork is the most common cause, and roughly 22% of claim disputes stem from delays in claim processing due to administrative bottlenecks. Missing documentation (death certificates, beneficiary proof, or policy details) causes another 25% of disputes. For a deeper look at what causes hold-ups and how to push back, see our guide to life insurance claim delays.

Deaths occurring within the contestability period (typically the first two years of the policy) trigger automatic application reviews for fraud or misrepresentation. If discrepancies arise during this review, the claim can be delayed significantly while the insurer investigates. In some cases, complex or contested claims stretch to 60 to 90 days or more.

Investigations may also be triggered by the cause of death, particularly if it involves excluded activities, fraud suspicion, or requires extensive medical records verification. Policy status problems such as lapsed policies due to unpaid premiums or lost policies can result in denial or extended searches.

Beneficiary complications create additional delays. Incomplete beneficiary information, identity verification issues, or probate and estate disputes can put claims on hold. Learn more about beneficiary disputes and how they're resolved.

Death Benefit Payout Options

Available Settlement Options

Beneficiaries typically have five main options for receiving life insurance proceeds. The lump sum option provides the full death benefit at once, usually via check, wire transfer, or direct deposit. This is the default on virtually every policy and remains the most common choice, offering the entire proceeds income-tax-free in a single payment.

Fixed period installments spread the benefit over a chosen number of years (often 10, 15, or 20). Each payment includes principal plus credited interest, designed to fully deplete the benefit by the end of the period. For example, a $250,000 benefit might be paid as $25,000 annually for 10 years.

Fixed amount installments let beneficiaries choose a specific monthly or annual dollar amount (such as $2,000 per month) and continue payments until the funds plus credited interest are exhausted. The duration depends on the payment size and interest crediting rate.

Life income options convert the death benefit into lifetime monthly payments, similar to a single premium immediate annuity, based on the beneficiary's age and actuarial life expectancy. Younger beneficiaries receive smaller monthly amounts since payments continue longer. A life income with period certain feature guarantees payments for a minimum period (typically 10, 15, or 20 years), so remaining payments go to a contingent beneficiary if the primary beneficiary dies early.

Interest-only arrangements allow the benefit to remain with the insurer while earning guaranteed interest. The beneficiary receives periodic interest payments while keeping the principal intact for later withdrawal or conversion to another payout option. Retained asset accounts are similar but function like a checking account with check-writing privileges. For a detailed comparison, see our guide to beneficiary payout options.

Comparing Lump Sum vs. Installment Payments

Lump sum payments offer immediate full access to funds, making them ideal for paying off debts, investing, or addressing urgent financial needs. This is the simplest option and most commonly chosen by beneficiaries. However, lump sums carry the risk of rapid spending or poor investment decisions, and they don't provide a built-in income stream for long-term needs.

Installment payments provide steady income over time, which can help with budget management and spending control. The remaining balance typically earns interest, potentially increasing the total received. The downsides include lower immediate access to funds and gradual depletion of the principal.

For income replacement purposes, installments or annuities may better serve beneficiaries who need steady cash flow. Lump sums work better for those with specific financial goals or the discipline to manage a large amount responsibly.

Tax Implications of Death Benefits

When Death Benefits Are Tax-Free

Under IRC Section 101(a), amounts received under a life insurance contract by reason of the insured's death are excluded from gross income. Beneficiaries receiving lump-sum payments typically owe no federal income tax on the proceeds, regardless of the benefit amount. Employer-provided group life insurance is tax-free up to $50,000, with amounts above that potentially taxed as a fringe benefit. Read our full guide on whether life insurance is taxable.

Taxable Interest on Payments

The principal death benefit amount remains tax-free, but any interest earned on payments is subject to federal income tax as ordinary income. This becomes relevant when beneficiaries choose installment payments, annuities, or interest-only arrangements rather than lump-sum payouts.

For example, if a $500,000 death benefit is paid over multiple years, the beneficiary pays no tax on the $500,000 principal but must report any interest accrued as taxable income. Interest earned on retained asset accounts is also taxable, and beneficiaries typically receive Form 1099-INT (or Form 1099-R depending on the structure) from the insurer reporting this interest for tax filing.

Special Tax Situations in 2026

Death benefits paid to the insured's estate rather than a named beneficiary may be subject to estate taxes if the total estate value exceeds federal thresholds. Under the One Big Beautiful Bill Act signed July 4, 2025, the 2026 federal estate and gift tax exemption is permanently set at $15 million per person ($30 million for a married couple with portability), with a top estate tax rate of 40% on amounts above the exemption. The 2026 annual gift tax exclusion is $19,000 per recipient ($38,000 per recipient for a married couple splitting gifts).

If a life insurance policy was sold to a third party before the insured's death through a life settlement or viatical settlement, different tax rules apply. For high-net-worth families, naming a trust as beneficiary (specifically an irrevocable life insurance trust) can help keep the death benefit out of the taxable estate. Read more about using life insurance for estate liquidity in larger estate plans.

Situations Where Claims Are Denied

While roughly 98% of filed claims are eventually paid, 2026 industry analyses show that 10% to 20% of claims encounter an initial denial, extended investigation, or major delay before ultimate resolution. Only about 2% to 3% of claims result in a final, uncompensated denial. Understanding the most common denial reasons can help beneficiaries prepare and protect themselves.

Material Misrepresentation

The single most common true denial reason is alleged non-disclosure or material misrepresentation on the application. NAIC research has historically attributed roughly 56% of denied and resisted claims to material misrepresentation. Applicants must fully disclose health history, lifestyle habits, hobbies, income, and other material facts. If the insurer discovers discrepancies after death (particularly during the contestability period), they can deny the claim.

Examples include failing to disclose pre-existing medical conditions, tobacco use, dangerous hobbies like private aviation, or criminal history. Even unintentional omissions can lead to denial if the insurer determines the information would have affected underwriting. Insurers increasingly use post-death pharmacy, medical, and financial data reviews to find discrepancies.

Contestability Period Issues

The contestability period (typically the first 24 months after policy issuance) allows insurers to investigate and contest claims. During this window, insurers can scrutinize applications for fraud, omissions, or inaccuracies regardless of the cause of death. This represents a top trigger for claim denials and delays.

After the two-year contestability period expires, claims become much harder to contest unless outright fraud is proven.

Policy Lapse and Premium Issues

Coverage ends if premium payments are missed, even after the grace period expires (typically 30 days). Policies must be active at the time of death for benefits to be paid. Industry data attributes roughly 25% of denials to lapse in premium payment. If a policy lapses due to non-payment and the insured dies afterward, the claim will be denied. In fact, roughly 99% of term life policies never pay a claim, largely because policyholders either let the coverage lapse or outlive the term.

Some policies have reinstatement provisions allowing lapsed policies to be restored, but this must occur before death. For more on what happens when a life insurance claim is denied, including how to file a successful appeal, see our dedicated guide.

Suicide Clause and Excluded Activities

Most life insurance policies exclude coverage for suicide within the first two years of the policy, and suicide denials represent about 14% of all denied claims according to industry analyses. Deaths by suicide after the two-year period typically result in full benefit payment. Policies often also exclude deaths resulting from illegal activities, drug or alcohol intoxication, war, or specifically excluded high-risk hobbies like skydiving or BASE jumping unless additional riders are purchased. Learn more about what life insurance actually covers.

Documentation and Beneficiary Problems

Claims can be denied for inadequate documentation or beneficiary designation problems, including unclear, outdated, or disputed beneficiaries resulting from divorce, minors, or legal disputes. NAIC-related data attributes about 22% of denials to incomplete documentation. Avoiding these common beneficiary mistakes is one of the most effective ways to protect your family. Beneficiaries involved in the insured's death may be disqualified under "slayer statutes" in most states. Group life insurance from employers continues to generate a disproportionate share of denials due to employer-side errors such as missed "actively at work" requirements or premium remittance failures.

Frequently Asked Questions

How long does it take to receive a life insurance payout in 2026?

Life insurance payouts typically take 14 to 60 days from the time a complete claim is filed, with most straightforward cases paid within 7 to 30 days when documentation is in order. Clean claims processed via electronic funds transfer can arrive in as little as 3 to 5 days. Most states follow a 30-day benchmark, requiring insurers to pay a completed claim within roughly 30 days or begin accruing interest on the unpaid benefit. Delays beyond 60 days usually indicate a contestability investigation, missing paperwork, or a beneficiary dispute.

Is life insurance money taxable when you receive it?

Life insurance death benefits are generally not taxable as federal income under IRC Section 101(a), and beneficiaries receiving lump-sum payments typically owe no income tax regardless of the amount. However, any interest earned on the death benefit is taxable as ordinary income, which becomes relevant for installment payments, annuities, or retained asset accounts. The principal portion remains tax-free while only the interest is reported on Form 1099-INT. Estate taxes may apply if the death benefit is paid into an estate that exceeds the 2026 federal exemption of $15 million per person.

What is the best payout option for life insurance beneficiaries?

The best payout option depends on individual financial circumstances and needs. Lump sum payments work well for beneficiaries who need immediate funds to pay debts or invest, and who have the discipline to manage a large amount. Installment payments or life income options provide steady cash flow for those who want protection against overspending or worry about outliving the money. Younger beneficiaries or those without financial management experience may benefit from structured payments, while financially experienced beneficiaries often prefer lump sums to invest on their own terms.

Can a life insurance claim be denied after two years?

After the two-year contestability period expires, life insurance claims become much more difficult to deny based on application issues. However, denials can still occur for reasons unrelated to contestability, including lapsed policies due to non-payment, deaths from specifically excluded activities, inadequate documentation, or proven fraud. Most denials after the contestability period relate to policy status issues rather than application misrepresentations. Other policy terms, exclusions, and conditions remain enforceable throughout the policy's lifetime.

What should I do if my life insurance claim is denied?

If your claim is denied, first request a detailed written explanation from the insurance company outlining the specific reasons for denial. Review your policy documents and the application to understand whether the denial is justified, and file a formal appeal with the insurer providing additional documentation. If the appeal fails, consider consulting a life insurance attorney who specializes in claim denials, since many denials are overturned through legal challenge. You can also file a complaint with your state's insurance department, which may investigate and intervene on your behalf.