Compare Home Insurance Plans in Ohio

Find your best options in less than 2 minutes

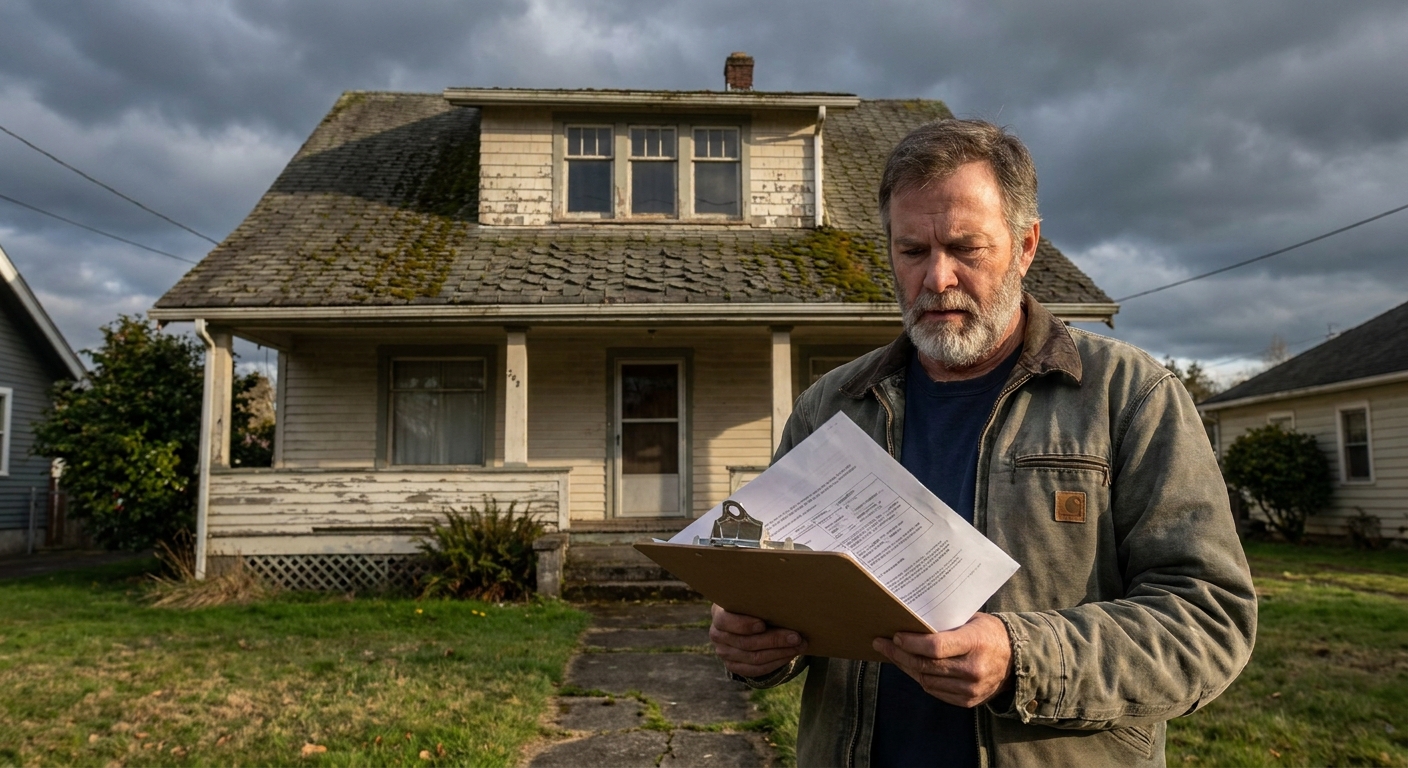

What Makes a Home "High Risk" for Insurance?

Insurers evaluate every home on a spectrum of risk before agreeing to cover it. When certain red flags stack up, a property can tip into "high risk" territory, making standard coverage difficult or impossible to obtain. Understanding what triggers that classification is the first step to addressing it.

Location-Based Risk Factors

Where your home sits is often the single biggest driver of high-risk status. Insurers use catastrophe models and geographic data to identify homes exposed to:

- Wildfire zones, Homes in or near the Wildland-Urban Interface (WUI) in states like California, Colorado, and Oregon face non-renewals at alarming rates. The January 2025 Palisades and Eaton wildfires generated roughly $40 billion in insured losses, accelerating carrier pullbacks that continue into 2026.

- Coastal and hurricane-prone areas, Properties within miles of the coast in Florida, Louisiana, and the Gulf states carry elevated wind, storm surge, and flooding exposure. Learn more about coastal home insurance costs and what to expect.

- Flood plains, Homes in FEMA-designated flood zones require separate flood coverage and signal elevated risk to property insurers.

- High-crime areas, Elevated theft and vandalism rates increase expected claims frequency.

According to recent analysis, homeowners in the top 20% of ZIP codes most exposed to climate-related losses now pay premiums roughly 82% higher than those in the lowest-risk ZIP codes.

Property Condition Risk Factors

Beyond location, the physical state of your home plays a major role in how insurers assess risk. Common property-condition triggers include:

| Risk Factor | Why Insurers Flag It | Typical Insurer Response |

|---|---|---|

| Old or damaged roof | Major driver of wind, hail, and water claims | Denial, surcharge, or ACV-only payout |

| Knob-and-tube or aluminum wiring | Significant fire hazard | Denial or requirement to update before binding |

| Galvanized steel or polybutylene pipes | High leak and burst failure rate | Surcharge or denial |

| Oil furnace or wood stove as primary heat | Fire and carbon monoxide risk | Endorsement required or denial |

| Prior claims history | Predicts future loss frequency | Surcharge, non-renewal, or denial |

| Deferred maintenance / poor condition | General liability and loss amplifier | Denial pending repairs |

For a deeper look at how these factors are evaluated, see home insurance underwriting explained and how each detail influences the decision. If your home has multiple property-condition issues, our guide to hard-to-insure homes walks through each red flag in detail.

Compare Home Insurance Plans in Ohio

Find your best options in less than 2 minutes

Insurance Options for High-Risk Homeowners

Being labeled high risk doesn't mean you're uninsurable. Several market segments exist specifically to serve homeowners that standard admitted carriers decline.

Admitted Carriers With Restrictions

Some standard admitted insurers will still write policies on high-risk homes, but with notable conditions attached:

- Higher deductibles, Often percentage-based (e.g., 1–5% of dwelling value) for windstorm, hail, or named storms rather than a flat dollar amount

- Exclusions for specific perils, A carrier might cover fire but exclude wind or require separate flood coverage

- Required upgrades before binding, They may offer a conditional quote contingent on roof replacement or electrical panel update within 30–60 days

If a standard insurer declines you outright, you have three primary alternative pathways. Read what to do when you're denied home insurance for a step-by-step recovery plan.

Excess & Surplus (E&S) Lines Insurance

Excess and surplus (E&S) insurance is the private market's answer to hard-to-place risks. E&S carriers are non-admitted, meaning they operate outside standard state rate and form regulations, giving them the flexibility to insure properties that admitted insurers won't touch.

The U.S. E&S market grew to roughly $130 billion in direct premium written by the end of 2024 and is projected to reach $140–145 billion for 2025, with more measured growth expected through 2026. AM Best has revised its 2026 outlook for the E&S segment to "Stable" from "Positive," citing moderating premium growth and selective rate softening for well-mitigated homes, while high-hazard properties still face tight underwriting. E&S remains the best private-market option for coastal, wildfire-zone, and older homes that admitted carriers decline.

State FAIR Plans and Residual Market Programs

When both admitted and E&S carriers decline, state FAIR Plans serve as the insurer of last resort. These are industry-funded pools, not government agencies, that provide basic property coverage to homeowners with no other options.

Key FAIR Plan limitations to understand:

- Coverage is typically named-peril only (fire, smoke, sometimes windstorm)

- No personal liability protection in most states

- No theft coverage in most states

- No loss of use / additional living expenses in most states

- Higher premiums relative to the narrow coverage provided

Most FAIR Plan policyholders should pair their plan with a Difference in Conditions (DIC) policy to fill in the major gaps. Read the full FAIR Plan insurance guide to understand how this combination works.

State-Specific Residual Market Programs

| State | Program | Primary Risk Covered |

|---|---|---|

| California | CA FAIR Plan (CFPA) | Wildfire / fire perils |

| Florida | Citizens Property Insurance Corp. | Hurricane / wind / all perils |

| Louisiana | Louisiana Citizens Property Insurance | Wind / hurricane |

| Texas | Texas Windstorm Insurance Association (TWIA) | Windstorm / hail (coastal) |

| New York | NY Property Insurance Underwriting Assoc. (NYPIUA) | Fire / basic perils |

| North Carolina | NC Insurance Underwriting Assoc. (Beach Plan) | Wind / coastal |

The California FAIR Plan has surged to 684,388 policies as of March 2026, a 146%+ increase since 2022, with total exposure now at $750 billion. It also has an approved 29.1% average rate increase taking effect October 15, 2026. Florida's Citizens Insurance, meanwhile, is moving the opposite direction: through aggressive depopulation, its policy count has dropped to about 336,000 as of March 2026, down 76% from its October 2023 peak of 1.41 million. If your insurer has recently left your state, see what to do when your insurance company leaves your state.

Protect your home with State Farm

Average Rate:

Homeowners who bundle and save with State Farm save an average of $1,000 per year!

You're in Good Hands® with Allstate

Average Rate:

Get comprehensive home coverage with flexible policy options.

Customize your home coverage

Average Rate:

Only pay for the coverage you need with personalized home insurance.

Smart coverage for your home

Average Rate:

Protect what matters most with award-winning home insurance.

Costs and Coverage Limitations of High-Risk Policies

What High-Risk Home Insurance Costs

High-risk home insurance is significantly more expensive than standard coverage. The national average sits around $2,700–$3,050 per year in 2026, with Insurify projecting the average to hit roughly $3,057 by year-end. High-risk policies routinely exceed that, sometimes dramatically.

| State / Scenario | Example Annual Premium | Vs. National Avg (~$2,900) |

|---|---|---|

| Florida (statewide, high-risk profile) | ~$8,292 | +175% |

| Oklahoma (severe storm/tornado) | ~$5,298 | +83% |

| Nebraska (hail, severe storms) | ~$4,956 | +71% |

| Colorado (wildfire, hail) | ~$4,310 | +49% |

| High-risk via E&S carrier | 20–100%+ above standard | Varies by peril |

After home insurance costs rose an average of 12% nationally in 2025, Insurify projects another 4% increase in 2026, though high-risk areas are still seeing sharper hikes driven by reinsurance costs, rebuild cost inflation, and catastrophe losses. Homeowners in the top 20% of climate-risk ZIP codes pay roughly 82% more than those in the lowest-risk ZIPs. This is part of the broader home insurance affordability crisis hitting homeowners nationwide.

Common Coverage Restrictions in High-Risk Policies

High-risk policies, whether from non-standard carriers, E&S insurers, or FAIR Plans, typically come with meaningful coverage limitations compared to a standard HO-3 policy:

- Percentage deductibles for wind, hail, or named storms (1–5% of dwelling value vs. a flat deductible)

- Actual cash value (ACV) payout for roof claims instead of full replacement cost

- Flood and earthquake exclusions requiring separate policies

- No or limited liability coverage (especially FAIR Plans)

- Scheduled personal property required for valuables above low sub-limits

- Ordinance or law exclusions, upgrades required by building codes after a loss may not be covered

For homeowners already stretched thin, being underinsured is a real danger even when you technically have a policy. Always review your coverage limits against your home's actual rebuild cost.

How to Improve Insurability and Return to Standard Coverage

Being in the high-risk market doesn't have to be permanent. Most homeowners can take concrete steps to reduce their risk profile and qualify for standard coverage, often within one to three years.

Upgrades That Reduce Your Risk Profile

The most effective improvements target the specific factors that triggered your high-risk classification:

Steps to Transition Back to Standard Insurance

- Document every improvement. Keep photos, contractor invoices, and permits for all upgrades. Insurers need proof of work completed.

- Work with an independent agent. They have access to multiple markets including surplus lines, non-standard carriers, and admitted insurers, and can guide you toward the right pathway.

- Maintain claims-free status. Every year without a claim improves your risk profile. A 3–5 year claims-free record is often what tips the scale back toward standard eligibility.

- Request re-underwriting annually. Ask your agent to re-shop your policy each year. Conditions and carrier appetites change, particularly as E&S capacity softens for lower-hazard risks in 2026.

- Consider certifications. Standards like IBHS FORTIFIED Gold or similar resilience certifications can unlock discounts and improve standard market access in some states.

- Bundle policies. If you qualify for auto or umbrella with a carrier, bundling can sometimes open a door to homeowners coverage that wouldn't be available otherwise.

For more on how coverage lapses can compound the challenge, read about continuous home insurance coverage and why maintaining uninterrupted coverage matters even in the high-risk market. Also see cheap home insurance strategies that can apply even when you're working through a non-standard carrier.

Frequently Asked Questions

What makes a home considered high risk for insurance?

Insurers classify homes as high risk based on a combination of location and property condition factors. Location risks include wildfire zones, flood plains, coastal areas, and high-crime neighborhoods. Property factors include old or damaged roofs, outdated electrical wiring (especially knob-and-tube or aluminum), aging plumbing systems, and a history of prior claims. The more of these factors present, the harder the home is to insure through standard admitted carriers.

How much more does high-risk home insurance cost compared to standard?

High-risk policies typically cost 20% to well over 100% more than a standard homeowners policy, depending on the specific risks involved. In 2026, Florida homeowners average around $8,292 annually and Oklahoma around $5,298, compared to a national average of roughly $2,700 to $3,050. E&S and non-standard carrier policies also carry higher premiums, though they offer the flexibility to cover properties standard markets won't touch at any price.

What is the difference between a FAIR Plan and E&S insurance?

A FAIR Plan is a state-mandated insurer of last resort, an industry-funded pool that provides basic named-peril coverage (usually fire and smoke) when no private market option exists. E&S (Excess & Surplus) insurance is a private, non-admitted market where specialized carriers write flexible policies for high-risk properties at market-driven rates. FAIR Plans offer less coverage but exist in most states; E&S coverage is broader but varies by carrier and may not be available in all situations.

Can I get standard home insurance again after being classified as high risk?

Yes, transitioning back to standard coverage is achievable for most homeowners with the right strategy. The key steps include making documented property improvements (roof replacement, electrical/plumbing updates), maintaining a claims-free record for 3–5 years, and working with an independent agent who shops your risk annually. Location-based risks like wildfire or flood zone designation are harder to overcome, but even those homeowners may qualify for better terms over time as the market evolves.

Do I need a special broker to find high-risk home insurance?

You don't need a special license, but you do need to work with the right professional. An independent insurance agent or broker, especially one with access to surplus lines markets, is your best resource. Unlike captive agents who represent a single carrier, independent agents can shop your risk across multiple admitted insurers, E&S carriers, and FAIR Plans to find the best available option. In some states, only licensed surplus lines brokers can place E&S policies, so confirm your agent has that access.