Compare Car Insurance Rates in Ohio

See if you qualify for a lower rate in less than 2 minutes

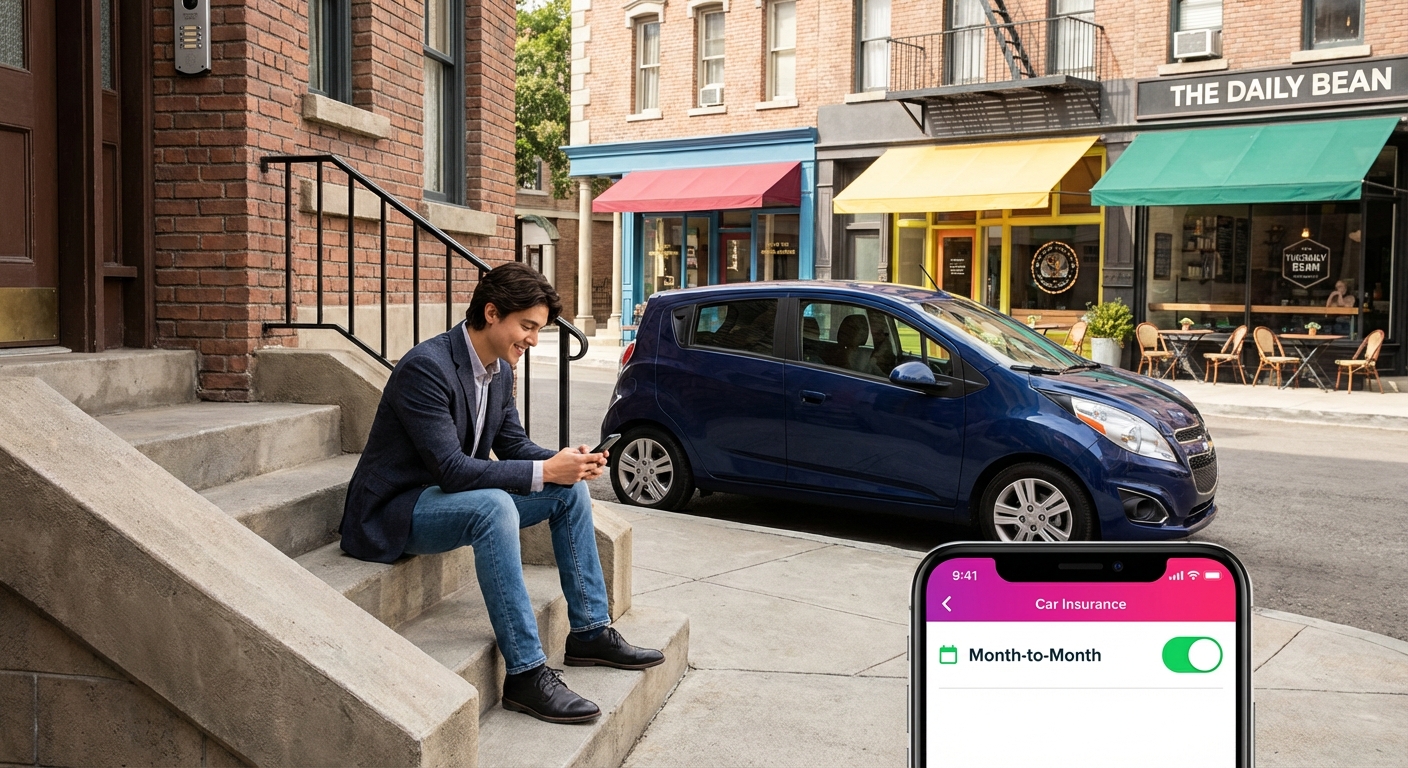

What Is Subscription-Based Car Insurance?

Subscription-based car insurance is a flexible alternative to traditional 6-month or 12-month auto policies. Instead of locking into a long-term contract, drivers pay on a month-to-month basis — and in many models, they're only charged for the miles they actually drive. The two most common formats are pay-per-mile insurance (a base monthly rate plus a per-mile fee) and pay-as-you-go insurance (flexible billing cycles tied to actual usage or driving behavior).

Unlike standard policies that charge fixed premiums regardless of how much or how little you drive, subscription-style plans use telematics — either a smartphone app or a plug-in device — to track mileage and behavior in real time. This creates a dynamic pricing model that rewards low-mileage and safe drivers. Learn more about how telematics programs work and how they can lower your premiums.

Subscription vs. Traditional Auto Insurance

Here's how the two models stack up against each other:

| Feature | Subscription / Pay-Per-Mile | Traditional 6 or 12-Month Policy |

|---|---|---|

| Pricing Model | Base rate + per-mile fee (e.g., $0.05–$0.12/mile) | Fixed premium regardless of mileage |

| Commitment | Month-to-month; cancel anytime | Locked in for 6 or 12 months |

| Tracking Required | Yes — app or OBD-II device | No tracking required |

| Best For | Low-mileage, occasional, or urban drivers | High-mileage or predictable daily commuters |

| Average Annual Cost | $800–$1,500 for drivers under 10,000 mi/yr | $2,158–$2,697 nationally (full coverage, 2026) |

| Coverage Types | Liability, collision, comprehensive available | Full range available |

| Rate Flexibility | Scales with actual usage | Locked until renewal |

Learn more about how pay-per-mile insurance works and whether it's right for your situation.

Compare Car Insurance Rates in Ohio

See if you qualify for a lower rate in less than 2 minutes

Who Offers Subscription-Style Car Insurance?

Several established insurers and insurtech companies now offer flexible, usage-based plans that function like a subscription model. Here's a look at the major providers as of 2026:

Major Pay-Per-Mile Providers in 2026

| Provider | How It Works | States Available | Best For |

|---|---|---|---|

| Nationwide SmartMiles | Base rate + per-mile charge; 250-mile daily cap; up to 10% safe driver discount | ~40 states (excl. AK, HI, LA, NC, NY, OK) | Best overall; avg. 33% savings |

| Allstate Milewise | Daily base rate + per-mile fee; also offers Unlimited option | ~22 states + D.C. | Occasional and remote drivers |

| Mile Auto | Odometer photo check-ins; no GPS tracking | Select states | Privacy-conscious low-mileage drivers |

| Lemonade | Absorbed Metromile in 2022; AI-driven; app-based | AZ, IL, OH, OR, TN, TX, WA | Tech-savvy urban drivers |

| Hugo | Unlimited Basic and Full plans; liability-focused; no down payment | ~16 states (expanding) | Gig workers and infrequent drivers |

| OCHO | Bi-weekly, $0 down payment; full coverage options; credit-building | Select states | Budget-conscious and credit-thin drivers |

Note: Hugo discontinued its Flex (on/off) plans for new customers in March 2025 and now offers its Unlimited Basic and Unlimited Full plans. OCHO remains a strong alternative for those needing full coverage with flexible payment schedules.

For a broader look at flexible coverage options, check out our guide to on-demand car insurance and how pay-as-you-go coverage works. You can also explore micro auto insurance for even shorter-term coverage options.

Protect your car with Farmers

Average Rate:

Find coverage options that fit your budget.

The insurance savings you expect.

Average Rate:

Enjoy personalized policies, comprehensive coverage & more.

See how much you could save today!

Average Rate:

Drivers who switch their auto insurance and save with State Farm save $764 on average!

Safe Drivers Save with Allstate®

Average Rate:

Get rewarded with savings for having a clean driving record.

Who Benefits Most from Subscription Car Insurance?

Subscription and pay-per-mile models aren't the right fit for every driver — but for certain groups, the savings are significant.

Occasional Drivers & Urban Residents

City dwellers who rely on public transit, rideshare apps, or walking for most of their trips often drive far fewer than the national average of approximately 13,596 miles per year. For these drivers, paying a fixed traditional premium means subsidizing miles they never actually drive. A pay-per-mile model directly ties cost to usage, making it far more fair and affordable.

Remote Workers & Retirees

If your car mostly sits in the driveway, a subscription-style plan can dramatically cut your annual insurance bill. Remote workers and retirees commonly fall under 7,500 miles per year — the sweet spot where pay-per-mile pricing generates the biggest savings over fixed-rate policies. See how annual mileage affects your rates in more detail.

Gig Workers (with Caveats)

Gig workers who drive heavily for work but keep personal miles low can benefit from flexible subscription plans for their personal driving. However, they must separately ensure they're covered during commercial use.

Comparison: Who Should Use What?

Costs, Cancellation, and 2026 Trends

What Does Subscription Car Insurance Actually Cost?

Traditional full-coverage auto insurance now averages $2,158–$2,697 per year nationally in 2026 — a range that reflects variation by source, methodology, and state. Subscription-style plans can significantly undercut that for the right driver:

- Low-mileage drivers (under 10,000 miles/year): Estimated $800–$1,500/year on pay-per-mile plans — roughly 30–50% less than traditional full coverage

- Moderate drivers (10,000–12,000 miles/year): Savings shrink; costs may be comparable to traditional pricing

- High-mileage drivers (15,000+ miles/year): Pay-per-mile costs can exceed traditional policy rates

The per-mile rate typically ranges from $0.05 to $0.15 per mile, plus a fixed base rate of $30–$60/month. Usage-based insurance programs (telematics-based, not strictly pay-per-mile) can reduce premiums by 10–30% for safe drivers. See how these compare to annual vs. monthly payment structures in traditional policies, or review how car insurance payment plans work to find the best billing option for your budget.

How Cancellation Works

One of the biggest advantages of subscription-style insurance is the freedom to cancel without major penalties. Here's what to expect:

- You can cancel at any time — most states allow policyholders to cancel whenever they choose by contacting the insurer via phone, app, or written notice

- Prorated refunds are typically issued for any prepaid premium covering unused coverage days

- Cancellation fees are possible but rare — usually a flat fee or a short-rate fee of roughly 10% of the unearned premium in some states

- No coverage gap rule still applies — always have a replacement policy active before canceling to avoid a lapse that could raise your future rates

For more on how flexible plans compare to longer commitments in terms of rate locks, see our guide on subscription-based monthly plans. You can also learn about car insurance billing and payment to understand how payment cycles work across different plan types.

2026 Emerging Trends in Flexible Insurance

The usage-based insurance market is one of the fastest-growing segments in financial services. Key trends shaping subscription car insurance in 2026 include:

- Explosive market growth: The global UBI market is estimated at $30–$75 billion in 2025, with the North American market alone projected at $13–$14 billion and growing at a robust 15–25% CAGR through 2034, driven by telematics adoption and AI-powered pricing

- Embedded vehicle telematics: Automakers are now building telematics directly into new vehicles, eliminating the need for plug-in devices and making data collection seamless for insurers

- AI-driven personalization: Insurers using real-time behavioral data and AI can reduce claims costs by 20–30% while offering better rates to safe, low-mileage drivers

- EV synergies: Electric vehicles, which come standard with connected car technology, are projected to account for a growing share of new UBI policies through the end of the decade

- Privacy legislation intensifying: Beyond the FTC's January 2026 consent order against GM/OnStar, a federal class action against Allstate and its subsidiary Arity — alleging data collection from ~45 million Americans via third-party apps — advanced in March 2026 when a federal court allowed the case to proceed on Wiretap Act and FCRA claims across 20 states

Learn more about how telematics programs track your driving and what your data rights are in 2026. You can also compare usage-based insurance programs side by side to see which offers the best balance of savings and privacy. If you frequently borrow or rent vehicles, a non-owner car insurance policy may also be worth exploring.

Frequently Asked Questions

Is subscription-based car insurance legal and valid in all states?

Pay-per-mile and usage-based insurance are legitimate, state-regulated products, but availability varies significantly. Nationwide SmartMiles is available in approximately 40 states (excluding AK, HI, LA, NC, NY, and OK), while Allstate Milewise now operates in roughly 22 states plus D.C. Before signing up for any subscription-style plan, verify that the specific program operates in your state and meets your state's minimum liability requirements. You can check directly with the insurer or use a comparison tool to see which programs are active in your ZIP code.

Can I switch from a traditional policy to a subscription plan mid-term?

Yes — you can cancel a traditional policy at any time and switch to a subscription or pay-per-mile plan. You'll typically receive a prorated refund for your unused premium, minus any applicable cancellation fee (usually a flat fee or a 10% short-rate charge in some states). Make sure your new subscription plan is active before canceling the old one to avoid a coverage lapse, which can trigger rate increases at your next insurer. Review our guide on car insurance payment plans for tips on managing transitions between policies.

Will subscription insurance cover me if I rent a car or drive someone else's vehicle?

Coverage rules for rental cars and borrowed vehicles depend on the specific policy, not the billing model. Most pay-per-mile or subscription-style plans follow the same rules as traditional policies — liability typically extends to rental cars up to your policy limits, but you may still want a collision damage waiver from the rental company. Always review your declarations page or ask your insurer directly. Consider a non-owner car insurance policy if you frequently borrow or rent vehicles.

Does a subscription plan hurt my driving record or credit if I cancel?

Canceling a car insurance subscription does not directly affect your credit score or driving record. However, a coverage lapse — even a brief one — can be flagged by future insurers, potentially raising your rates by 8–35% depending on the state and duration. Always maintain consecutive, uninterrupted coverage to preserve your insurance history and access the best available rates going forward. Review our guide on car insurance billing and payment for tips on managing transitions between policies.

Is subscription car insurance worth it compared to a 6-month policy?

It depends entirely on your mileage. If you drive fewer than 10,000 miles per year, a subscription or pay-per-mile plan can save you 20–40% versus a traditional full-coverage policy that now averages $2,158–$2,697 annually. If you drive more than 12,000–15,000 miles annually, the per-mile costs will likely match or exceed what you'd pay on a standard policy. Run a mileage estimate before committing — most providers offer free online calculators to compare projected costs, and our guide on pay-per-mile insurance walks you through exactly how to do it.