Compare Car Insurance Rates in Ohio

See if you qualify for a lower rate in less than 2 minutes

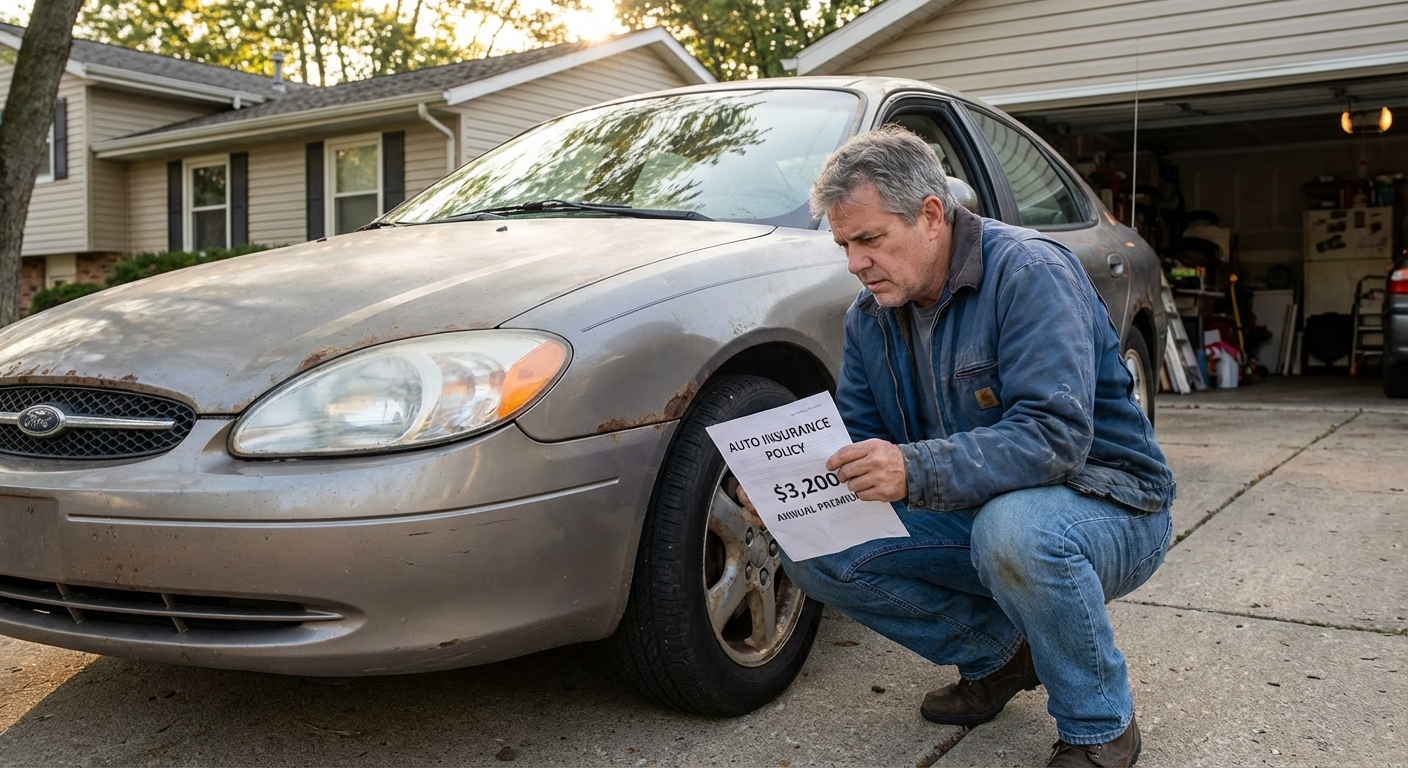

How a Car's Age Affects Your Insurance Decisions

When your car gets older, your insurance strategy should evolve with it. A brand-new vehicle financed through a lender requires full coverage car insurance, but the math changes dramatically once a car depreciates. As a vehicle ages, its market value shrinks, and in many cases the cost of maintaining comprehensive and collision coverage outpaces what the insurer would ever pay out in a claim.

New cars typically lose about 20% of their value in the first year alone, then continue depreciating roughly 10 to 15% per year through year four. By the five-year mark, the average car retains only about 40 to 45% of its original value, according to Kelley Blue Book and CARFAX data. After that, depreciation keeps eating away at the car's worth, which means the gap between what you pay in premiums and what an insurer would actually pay you keeps narrowing. The aging vehicle fleet trend is real. The average vehicle age on U.S. roads hit a record 12.8 years in 2025, per S&P Global Mobility, with CCC projecting the figure will reach 13 years in 2026. Passenger cars alone now average 14.5 years, meaning more drivers than ever face this exact coverage decision.

Here are the primary ways vehicle age influences insurance decisions:

- Depreciation reduces payout potential. A 10-year-old car worth $4,000 can only ever be reimbursed up to $4,000, minus your deductible. If your deductible is $1,000, your maximum net payout is just $3,000.

- Lender requirements drop off. Once your auto loan is paid off, you're free to reduce coverage. Lenders require full coverage on financed cars to protect their investment, but once you own it outright, it's your call.

- Repair costs may exceed value. Older vehicles often cost more to repair than they're worth, making collision and comprehensive payouts almost irrelevant.

- Liability remains mandatory. No matter how old your car is, every state requires you to carry some form of liability insurance to legally drive on public roads.

Compare Car Insurance Rates in Ohio

See if you qualify for a lower rate in less than 2 minutes

The Value Threshold: When to Drop Comprehensive & Collision

The most practical framework for deciding when to drop comprehensive and collision coverage is the 10% rule: if your annual premium for those coverages exceeds 10% of your car's total market value, dropping them is likely the smarter financial move.

In mid-2026, the national average cost of full coverage car insurance ranges from approximately $2,237 to $2,926 per year depending on the data source (Insurify's July 2026 data reports $2,237/year, ValuePenguin $2,495/year, Insurance.com $2,578/year, and Experian $2,926/year), compared to roughly $738 to $1,572 per year for liability-only or minimum coverage. That's a savings gap of $1,000 to $2,100 annually, savings that compound quickly when your car simply isn't worth protecting with full coverage.

The 10% Rule in Practice

| Car Value | Annual Comp/Collision Premium | 10% Threshold Exceeded? | Recommendation |

|---|---|---|---|

| $10,000 | $600 | ❌ No (6%) | Keep coverage |

| $6,000 | $700 | ✅ Yes (11.7%) | Consider dropping |

| $4,000 | $500 | ✅ Yes (12.5%) | Drop coverage |

| $2,500 | $450 | ✅ Yes (18%) | Strongly drop |

| $1,500 | $400 | ✅ Yes (26.7%) | Drop immediately |

The $5,000 to $7,500 Tipping Point

Most financial experts recommend dropping collision coverage when your vehicle's market value falls below $5,000 to $7,500. With elevated premiums and repair costs in 2025 and 2026 (driven in part by the 25% Section 232 tariff on imported auto parts that took effect in May 2025), MoneyGeek and other advisors have moved this threshold up from the traditional $4,000 to $5,000 benchmark. Here's why the math matters:

- A $4,000 car with a $1,000 deductible yields a maximum payout of just $3,000.

- If you're paying $500/year for collision alone, you break even in only 6 years, and that's assuming a total loss scenario.

- A 20-year-old car has typically depreciated 90 to 99% of its original value, making any comp/collision payout minimal.

Always verify your car's actual cash value using tools like Kelley Blue Book, Edmunds, or NADA Guides before making any coverage changes. The number you find there is what an insurer would actually pay, not what you paid for the car. Learn more about how coverage downgrades work and the real risks involved.

When to Keep Comprehensive Coverage

Comprehensive coverage is generally cheaper than collision and covers events like theft, fire, flooding, and animal strikes. Even on an older car, it may still make sense to keep it if:

- You live in an area prone to hail, flooding, or high vehicle theft

- The car is stored outdoors and exposed to weather damage

- Your annual comprehensive premium is under $100

Protect your car with Farmers

Average Rate:

Find coverage options that fit your budget.

The insurance savings you expect.

Average Rate:

Enjoy personalized policies, comprehensive coverage & more.

See how much you could save today!

Average Rate:

Drivers who switch their auto insurance and save with State Farm save $764 on average!

Safe Drivers Save with Allstate®

Average Rate:

Get rewarded with savings for having a clean driving record.

Liability-Only Coverage for Older Cars

If you've decided to drop comp and collision, liability-only car insurance becomes your default coverage. This is the most affordable way to stay legally insured while owning an older, low-value vehicle. Switching from full coverage to liability-only on a low-value car can reduce your premium by 50 to 70%, saving hundreds to over $1,500 per year based on 2026 averages.

What Liability-Only Covers

Liability insurance covers damage and injuries you cause to others, not your own vehicle. It includes two components:

2026 State Minimum Requirements

Every state has its own minimum liability limits. Coverage is typically expressed as three numbers (e.g., 30/60/25):

- First number - Bodily injury per person (in thousands)

- Second number - Bodily injury per accident total (in thousands)

- Third number - Property damage per accident (in thousands)

Multiple states have updated their minimums in 2025 and 2026. California raised its minimums to 30/60/15 effective January 1, 2025 (the first increase since 1967, up from 15/30/5), and those limits will remain in force through at least 2034. Virginia increased to 50/100/25, Utah moved to 30/65/25, and North Carolina implemented a significant jump to 50/100/50, giving it the highest property damage minimum in the country plus a new mandatory UM/UIM requirement at 50/100. New Jersey completed a phased increase to 35/70/25 for standard policies effective January 1, 2026, and Hawaii moved to 40/80/20 the same day. Most recently, Massachusetts increased its minimum liability from 20/40/5 to 25/50/30 effective July 1, 2026, the state's first increase since 1988, applying to all new and renewing policies. Florida is also scheduled to overhaul its no-fault system on July 1, 2026 under HB 1181, eliminating PIP and adding 25/50 bodily injury minimums. Learn more about how much coverage you really need to protect your assets.

| State | Minimum Liability (BI/BI Total/PD) | Recent Change? |

|---|---|---|

| California | 30/60/15 | ✅ Updated Jan 2025 |

| Hawaii | 40/80/20 | ✅ Updated Jan 2026 |

| Massachusetts | 25/50/30 | ✅ Updated Jul 2026 |

| New Jersey | 35/70/25 | ✅ Updated Jan 2026 |

| North Carolina | 50/100/50 | ✅ Updated 2025 |

| Utah | 30/65/25 + PIP | ✅ Updated Jan 2025 |

| Virginia | 50/100/25 | ✅ Updated Jan 2025 |

| Florida | 25/50 BI + PD | ⚠️ Updates Jul 2026 |

Classic Car vs. Old Car Insurance: Key Differences

Not all older vehicles are created equal. A 1969 Ford Mustang and a 2005 Honda Accord may both be old, but they are insured very differently. Understanding the distinction between a classic car and simply an old car can unlock significant savings and better protection.

What Qualifies as a Classic Car?

Classic car insurance is a specialty product with unique eligibility requirements. While standards vary by insurer, most require:

- Vehicle is at least 20 to 25 years old (some insurers accept as young as 10 years for demonstrable collectibles, and State Farm's Classic+ program accepts vehicles as young as 10 years old)

- The car has collectible, historical, or appreciating value

- The vehicle is not used as a daily driver, limited to pleasure drives, shows, and club events

- Owner has a separate insured daily-use vehicle

- Annual mileage is capped in some plans (American Collectors offers 2,500/5,000/7,500-mile tiers; Grundy, Hagerty, American Family, and J.C. Taylor allow unlimited pleasure-use mileage)

- The vehicle must be stored in a locked garage or secure facility or otherwise off-street

- The vehicle must be in good to excellent condition, and drivers typically must be 25+ years old with a clean record

Classic vs. Standard Insurance Side-by-Side

The biggest financial advantage of classic car insurance is agreed value coverage. You and the insurer agree on the car's worth upfront, and that's exactly what you receive in a total loss, with no depreciation deducted. Standard policies pay actual cash value, which factors in wear and depreciation. Overall, classic car insurance typically costs 30 to 40% less than standard auto coverage because the vehicles are driven fewer miles under strict usage restrictions.

2026 Classic Car Insurance Costs

Specialty insurers offer significantly lower premiums than standard carriers for qualifying vehicles. For comparison, full coverage on a standard policy runs $2,237 to $2,926/year nationally, making classic car rates a dramatic bargain for eligible vehicles. Sample 2026 quotes (based on a 1966 Ford Mustang valued at $15,000 or a 1969 Camaro at $23,000, per MoneyGeek's 2026 comparison):

| Insurer | Annual Premium (Est.) | Key Feature |

|---|---|---|

| Leland-West | From ~$152/year | Lowest sample rate; unlimited mileage available |

| American Collectors | $201 to $244/year | Mid-range pricing; 2,500/5,000/7,500-mile tiers |

| Grundy | ~$200 to $350/year | Unlimited pleasure-use mileage; often $0 deductible |

| Hagerty | ~$284 to $700/year | Agreed value, spare parts coverage |

| State Farm Classic+ (driven by Hagerty) | Varies | Accepts vehicles as young as 10 years |

High Mileage and Pay-Per-Mile Considerations

For non-classic older vehicles with high odometer readings, mileage can affect both your rate and your coverage decision:

- Insurers consider over 15,000 miles/year as high mileage, which typically raises premiums by 30 to 40% compared to low-mileage drivers

- Pay-per-mile insurance (such as Nationwide SmartMiles or Allstate Milewise) charges a base rate plus a fee per mile driven. SmartMiles reports an average of 25% savings vs. traditional Nationwide policies, and Milewise scenarios show 40 to 50% savings at 4,000 to 6,000 miles/year

- Low annual mileage (under 7,500 miles) can meaningfully reduce your insurance costs, with breakeven typically hitting around 10,000 miles/year

- If your vehicle has over 100,000 miles, factor its overall condition and repair costs into your coverage equation

A high-mileage car with a low market value almost always belongs in the liability-only category. Use the 10% rule alongside your mileage to make the most informed decision. To understand the cost gap between liability and full coverage, see our detailed breakdown.

Frequently Asked Questions

At what mileage or age should I drop full coverage on my car?

There's no single age or mileage cutoff. The decision is based on your vehicle's current market value and the cost of your comp/collision premiums. Most experts recommend the 10% rule: if your annual comp/collision premium exceeds 10% of your car's value, it's time to consider dropping it. For most vehicles, this threshold hits somewhere between 8 and 12 years old, and you can also cross-check using the "10x rule" (drop coverage if your car is worth less than 10 times your annual comp/collision premium).

Is liability-only insurance legal on any car?

Yes. As long as you meet your state's minimum liability requirements, liability-only coverage is completely legal on any vehicle you own outright. The only exception is if your car is financed. Lenders will contractually require you to carry full coverage until the loan is paid off. Check your specific state's current minimums, as seven states have updated theirs in 2025 and 2026, including California, Virginia, North Carolina, Utah, New Jersey, Hawaii, and Massachusetts (effective July 1, 2026).

Can I get classic car insurance on a 10-year-old vehicle?

It depends on the insurer and the vehicle's characteristics. Some insurers, like State Farm's Classic+ program (driven by Hagerty), allow vehicles as young as 10 years old to qualify if they are used on a limited basis. However, most specialty insurers look for cars that are at least 20 to 25 years old with demonstrated collectible value. Review types of car insurance coverage before making the switch.

Does high mileage make car insurance more expensive?

Yes, to a degree. Driving over 15,000 miles annually is considered high mileage by most insurers and can incrementally increase your premiums. For older, high-mileage vehicles, the more important financial decision is whether to drop collision coverage based on the car's total value. Pay-per-mile insurance is worth exploring if you drive infrequently, with SmartMiles averaging around 25% savings and Milewise showing 40 to 50% savings at very low mileage.

What happens if I only carry state minimum liability and cause a major accident?

State minimums may not cover all damages in a serious accident. For example, California's minimum of $30,000 per person for bodily injury can be exceeded quickly in a multi-car crash involving medical bills and lost wages, especially given the average new-vehicle transaction price now exceeds $49,000. Any damages beyond your policy limits come out of your personal finances. Experts recommend carrying at least 100/300/100 limits, even when driving an older vehicle. Learn more about how much coverage you really need to find the right balance.