Compare Car Insurance Rates in Ohio

See if you qualify for a lower rate in less than 2 minutes

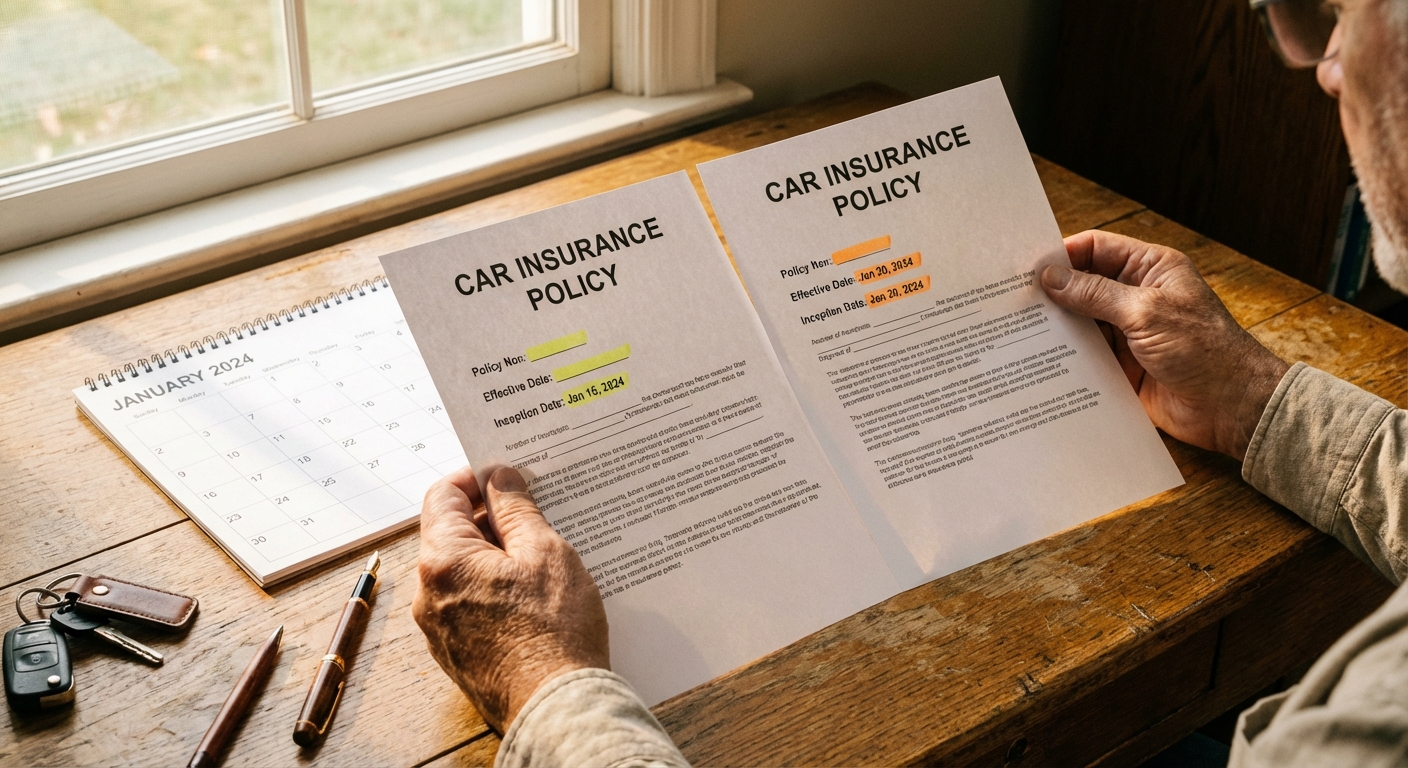

What Is an Inception Date vs. an Effective Date?

Most drivers have seen both "inception date" and "effective date" printed on their policy documents and assumed they mean the same thing. In most cases, they do. But there are important nuances that can affect your coverage, your claims, and your wallet. Knowing the difference could be what stands between a paid claim and a denied one.

Inception Date Defined

The inception date is the date on which your insurance policy first came into existence with a specific insurer. Think of it as the "birthday" of your policy. It is the original date you first contracted coverage, and critically, it can remain fixed across renewals with the same company. Insurers use this date to track how long you have been a customer and to calculate long-term loyalty discounts. Loyalty discounts typically range from 5% to 20% across major carriers, but they're applied to a base premium that has often already been inflated significantly above what a new customer would pay. Some top carriers like American Family reward tenure with discounts of up to 18% after 5 or more years of continuous coverage. State Farm's tenure-related benefits begin after 3 continuous years and, as of May 2026, State Farm expanded its Drive Safe & Save program to include customers with 3 or more years of tenure (previously 5), stacking on top of a program that can deliver up to 30% off for safe driving behavior.

Effective Date Defined

The effective date (also called the coverage start date or commencement date) is the exact date, and sometimes exact time, when your insurance protection becomes legally active. This is the moment the insurer becomes liable for covered losses. It is listed on your declarations page and your insurance ID card. Policies typically become effective at 12:01 AM on the stated date, meaning protection kicks in at the very start of that calendar day.

Compare Car Insurance Rates in Ohio

See if you qualify for a lower rate in less than 2 minutes

Why These Dates Sometimes Differ and When It Matters

For most straightforward policies, the inception date and effective date are identical. However, the distinction becomes significant in three common scenarios:

1. Policy Renewals

When you renew with the same insurer, the inception date stays anchored to when you originally started your policy, while the effective date rolls forward to the new term's start. This matters because some insurers use your original inception date to calculate loyalty discounts and rate tiers. Nationwide's Vanishing Deductible reduces your collision deductible by $100 for each claims-free year, taking a $500 deductible to $0 after 5 years, and critically that benefit does not transfer if you switch carriers. Progressive's loyalty benefits are more modest, typically in the 5% to 10% range, though the company will factor in prior continuous coverage from other insurers when you switch in. The policy term you choose (6 months or 12 months) also determines how frequently the effective date turns over and how often your rate can be re-evaluated. Learn more about how automatic renewal works and why shopping around before renewal can save switchers hundreds of dollars per year.

2. Future-Dated Policies

You can purchase a policy today but set it to become active 30 to 60 days from now. In this case, the inception date (when the contract was formed) precedes the effective date (when coverage activates). This is commonly done to lock in a better rate or to time coverage with a vehicle purchase. Learn more about the car insurance waiting period and how future-dating a policy can work in your favor.

3. Administrative Processing Delays

Sometimes an insurer issues your policy documents a day or two before your coverage actually begins. The issue date (when paperwork is generated) is different from both the inception and effective dates. Always confirm which date officially starts your coverage.

Protect your car with Farmers

Average Rate:

Find coverage options that fit your budget.

The insurance savings you expect.

Average Rate:

Enjoy personalized policies, comprehensive coverage & more.

See how much you could save today!

Average Rate:

Drivers who switch their auto insurance and save with State Farm save $764 on average!

Safe Drivers Save with Allstate®

Average Rate:

Get rewarded with savings for having a clean driving record.

When Coverage Actually Begins: Boundary Dates & Claims

Understanding exactly when coverage starts is not just academic. It has real financial consequences.

The 12:01 AM Rule

Most car insurance policies activate at 12:01 AM on the effective date. This means if your policy effective date is March 20, your coverage begins at the very start of that day, not at noon, not when you wake up. This matters enormously if an incident occurs on the first or last day of your policy. The same rule applies at expiration: most policies also end at 12:01 AM on the expiration date. Learn more about when policies expire to avoid an accidental gap.

Claims Filed on Boundary Dates

| Scenario | Covered? |

|---|---|

| Accident at 11:59 PM on the day before effective date | ❌ Not covered, policy not yet active |

| Accident at 12:01 AM on effective date | ✅ Covered, policy is active |

| Accident at 11:59 PM on policy expiration date | ❌ Not covered, policy has typically already ended |

| Accident on the inception date during a grace period | Depends on insurer terms |

Because policies often expire at 12:01 AM, you can be technically uninsured for nearly an entire calendar day if your old policy ends and your new one hasn't started yet. Understanding this window is critical, since even a brief gap in coverage can have expensive consequences.

Backdating Insurance Policies: What's Allowed and What Isn't

One of the most misunderstood topics around inception dates is backdating. Here's the unambiguous truth:

Backdating Is Generally Illegal

Backdating an effective date is considered to be illegal in most states and agents can be found guilty of auto insurance fraud. Many state insurance departments have made it illegal for carriers to sell backdated policies as new business. Major insurers including Geico, State Farm, Progressive, and Allstate operate under strict regulations that prevent issuing retroactive policies, and no legitimate insurer will alter your policy's effective date to cover a prior incident. Attempting to do so can result in:

- Immediate policy cancellation

- Denial of all claims

- Criminal charges and fines

- License suspension

- Permanent rate increases or difficulty obtaining coverage in the future

Learn more about material misrepresentation and the serious consequences of lying on an insurance application.

The One Narrow Exception: Administrative Backdating

There is a limited circumstance where a short administrative backdate may be permitted, specifically when a brief lapse occurred due to a paperwork or processing delay, and no losses occurred during that gap. In such cases, your insurer may ask you to sign a "no-loss statement" (also called an ACORD 37, a signed affidavit confirming no incidents happened during the lapse) before adjusting the effective date. This is a formal legal warranty, not just paperwork, and it is rare, insurer-specific, and never applies if any claim or accident is involved.

Planning ahead with a proper insurance binder is always the right way to avoid the temptation of backdating.

Continuous Coverage, Renewals & What to Verify When Buying

How Inception Dates Affect Continuous Coverage

Continuous coverage (having no lapse between policies) is critical for several reasons:

- State compliance: Most states require drivers to maintain active insurance. A lapse, even of one day, can trigger fines, registration suspension, or SR-22 requirements. Learn more about what happens after a lapse and how Louisiana's Act 476, effective January 1, 2026, prevents insurers from raising rates or adding surcharges for a driver's first lapse of 90 days or less, with the "first lapse" status resetting after 5 continuous years of coverage.

- Rate savings: In 2026, industry underwriting practice treats lapses as a significant risk factor, with common surcharges ranging from roughly 10% for short administrative lapses to 30% or more for longer or repeated gaps. With 2026 national average full-coverage premiums ranging from about $2,237 per year (Insurify, July 2026) to $2,496 (ValuePenguin) and $2,578 (Insurance.com), even a 20% lapse surcharge can add $450 to $500 per year. Insurify projects the national full-coverage average will climb only about 1% by the end of 2026, so a lapse penalty easily dwarfs typical rate movement.

- Insurer loyalty benefits: Some insurers use your original inception date to reward long-term customers with vanishing deductibles, accident forgiveness, or tenure-based discounts. Nationwide's Vanishing Deductible reduces your collision deductible by $100 per claims-free year up to $500 in savings, while top-tier loyalty programs at American Family and State Farm can reach 18% to 20% at 5 or more years.

When switching policies, time your new policy's effective date to the exact moment your old policy expires. A gap of even a few hours can create legal and financial exposure. Read more about coverage gaps and why they matter.

State Minimum Coverage Changes to Know (2025 to 2026)

Several states raised their minimum liability requirements recently, which can affect your declarations page and policy costs at renewal:

| State | Previous Minimum (BI/PD) | New Minimum | Effective |

|---|---|---|---|

| California | 15/30/5 | 30/60/15 | Jan. 1, 2025 |

| Utah | 25/65/15 | 30/65/25 | Jan. 1, 2025 |

| Virginia | 30/60/20 | 50/100/25 | Jan. 1, 2025 |

| North Carolina | 30/60/25 | 50/100/50 | July 1, 2025 |

| New Jersey | 25/50/25 | 35/70/25 | Jan. 1, 2026 |

| Colorado | Prior PD limits | Higher PD minimums | 2026 |

If you live in one of these states, verify that your declarations page reflects the updated minimums at your next renewal. Your insurer may auto-adjust, but it's still worth confirming.

Proof of Prior Coverage and Your Inception Date

When you switch insurers, your new carrier will often ask for proof of prior coverage to verify your insurance history. Your inception date with your previous insurer is a key part of this documentation. It demonstrates how long you maintained continuous coverage and can directly affect the rate you're offered. Longer gaps (over 90 days) can push premium surcharges to 40% or higher with some non-standard carriers.

Renewal Inception vs. Effective Date

At renewal, most insurers issue a new effective date, but your original inception date with that company remains on file. This is your "tenure" date, and it matters for loyalty perks. If you miss a payment and your policy is cancelled, you may lose this tenure entirely, resetting the clock on loyalty discounts you've earned. If a lapse does occur, learn what to do immediately to minimize the damage.

What to Verify When Purchasing a New Policy

Before your new policy goes live, check your declarations page for these critical items:

| What to Verify | Why It Matters |

|---|---|

| Effective date and exact time | Ensures no gap between old and new coverage |

| Policy expiration date | Defines the end of your coverage window |

| Vehicle VIN and details | Prevents claim denials due to wrong vehicle on file |

| Listed drivers | All household drivers must be listed |

| Coverage types and limits | Confirm liability, comprehensive, and collision are correct |

| Deductibles | Know your out-of-pocket amount before a claim arises |

| Lienholder or lessor listed | Required if you're financing or leasing |

| State minimum compliance | Verify updated minimums are reflected post-2025 and 2026 changes |

Confused by the jargon on your declarations page? Our car insurance terms glossary breaks down every coverage type and policy component in plain English.

Frequently Asked Questions

Is the inception date the same as the effective date on my car insurance?

In most everyday contexts, yes. Insurers often use the terms interchangeably to mean the date your coverage begins. However, a technical distinction exists: the inception date may refer to the original date you first contracted with an insurer (remaining fixed across renewals), while the effective date updates with each new policy term. Always review your declarations page to confirm which date is controlling your coverage window.

What happens if I file a claim on my policy's effective date?

Coverage on the effective date depends on the time of the incident relative to your policy's activation time, typically 12:01 AM. If your policy became active at 12:01 AM on March 20 and your accident occurred at 8:00 AM that same day, you are covered. If the accident occurred at 11:59 PM on March 19 (before activation), the claim would be denied. Always confirm the exact activation time listed in your policy documents.

Can I backdate my car insurance policy to cover an accident that already happened?

No. Backdating a car insurance policy to cover a prior incident is insurance fraud and is illegal in every U.S. state. Legitimate insurers such as Geico, State Farm, Progressive, and Allstate will not alter your effective date to cover past accidents or lapses. Attempting this can result in criminal charges, policy cancellation, and permanent difficulty obtaining affordable insurance in the future.

How does a lapse between my old and new policy affect my rates?

Even a short lapse in coverage can signal higher risk to insurers and trigger a premium increase. Industry underwriting practice in 2026 typically applies surcharges of roughly 10% for short administrative lapses and 20% to 30% or more for longer gaps, with high-risk drivers seeing even larger jumps. At 2026 average full-coverage rates ranging from about $2,237 (Insurify) to $2,578 (Insurance.com) per year, a long lapse could cost you several hundred dollars annually. Note that Louisiana's Act 476, effective January 1, 2026, protects drivers from a rate increase on a first lapse of 90 days or less, though state penalties like registration suspension or SR-22 filings can still apply elsewhere.

What is a "no-loss statement" and when would I need to sign one?

A no-loss statement (also called an ACORD 37 or statement of no loss) is a signed affidavit confirming that no accidents, losses, or claims occurred during a specific period, typically a brief coverage gap caused by an administrative or processing delay. Some insurers may use this document to allow a limited administrative backdate of your policy's effective date, helping you avoid state lapse penalties. It is only valid if genuinely no incidents occurred during the gap, and signing a false no-loss statement constitutes insurance fraud. This option is rare, insurer-specific, and should never be attempted to cover a prior accident.