Compare Home Warranty Options in Ohio

See what plans you qualify for in less than 2 minutes

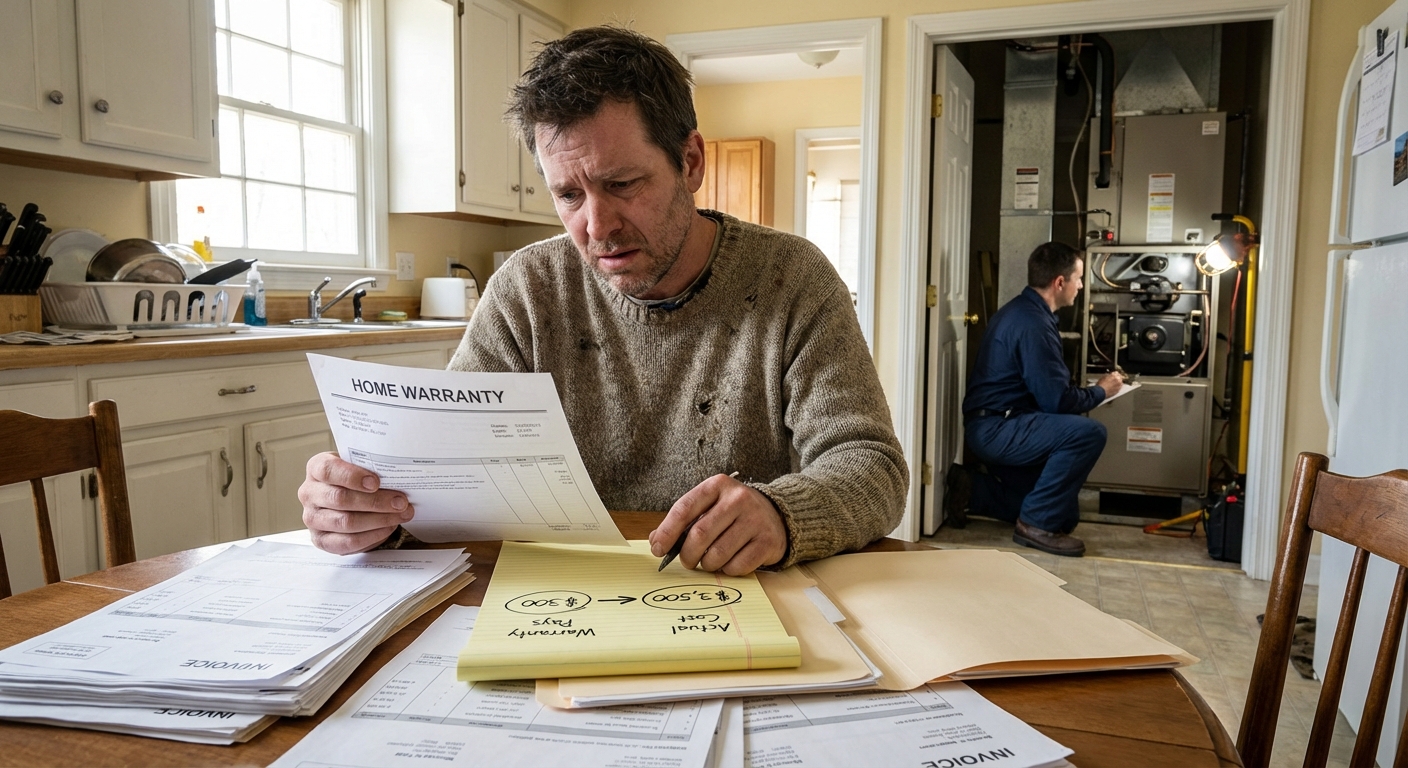

Understanding Home Warranty Payout Limits

Home warranty payout limits are the single most important detail hiding inside your service contract — and most homeowners don't discover them until they're staring down a $9,000 HVAC replacement bill with a $2,000 cap. Every home warranty plan sets a maximum dollar amount it will pay per covered item, per repair incident, and sometimes per year in total. These figures directly determine whether your warranty is a financial safety net or a false sense of security.

There are two primary types of limits you need to understand:

- Per-item caps — The maximum the plan pays for a single covered system or appliance (e.g., $2,000 for your air conditioner)

- Annual aggregate limits — The total the plan will pay across all claims in a 12-month contract period (e.g., $15,000 total regardless of how many claims you file)

Once either limit is hit, you're responsible for 100% of remaining costs. Understanding what a home warranty actually covers before you buy is essential to making a smart purchase.

How Per-Item Caps Work in Practice

Every covered item in your home warranty plan carries its own individual dollar ceiling. These caps vary significantly by provider and plan tier. Here's a breakdown of typical per-item coverage limits across the industry:

| System or Appliance | Low-Tier Cap | Mid-Tier Cap | High-Tier Cap |

|---|---|---|---|

| HVAC (Heating & Cooling) | $1,000–$2,000 | $3,000–$5,000 | $5,000–Unlimited |

| Plumbing System | $500–$1,000 | $1,500–$3,000 | $3,000–Unlimited |

| Electrical System | $500–$1,000 | $1,500–$3,000 | $3,000–Unlimited |

| Refrigerator | $500–$1,000 | $1,500–$2,500 | $3,500–$7,000 |

| Washer / Dryer | $500–$1,000 | $1,500–$2,000 | $3,500–$7,000 |

| Dishwasher | $500–$800 | $1,000–$1,500 | $2,500–$3,500 |

| Water Heater | $500–$1,000 | $1,500–$2,000 | $3,000–$5,000 |

| Built-in Microwave | $150–$300 | $400–$800 | $1,000–$2,000 |

These caps represent the ceiling — not a guaranteed payout. Your actual claim reimbursement will depend on the repair diagnosis, approved labor rates, and whether the failed component is specifically listed in your contract. Learn more about how home warranty appliance coverage works when it comes to individual item claims.

What Happens When Repair Costs Exceed the Cap

When an approved repair or replacement exceeds your plan's coverage limit, the process is straightforward but painful: you pay the difference. There is no negotiation on the cap itself unless you've selected a higher-tier plan.

Here's how common over-cap scenarios play out:

Scenario 1: HVAC Replacement

Your central air conditioner fails completely. The technician quotes a full system replacement at $8,500. Your plan has a $3,000 HVAC cap.

- Warranty pays: $3,000

- You pay: $5,500

- Service fee: $100 (still owed even on a capped claim)

Scenario 2: Refrigerator Compressor Failure

Your refrigerator's compressor fails on a high-end unit. Repair cost: $2,200. Your plan caps refrigerators at $1,500.

- Warranty pays: $1,500

- You pay: $700

- Service fee: $75

Scenario 3: Annual Aggregate Limit Hit

You have a $15,000 annual aggregate cap. Earlier in the year, a plumbing repair used $8,000 and an electrical repair used $5,000 — leaving $2,000 remaining in your aggregate. Your HVAC then fails and needs $6,000 in repairs.

- Warranty pays: $2,000 (remaining aggregate balance)

- You pay: $4,000

Some providers will notify you before work begins if a repair is projected to exceed your coverage cap, giving you a chance to authorize the overage or explore alternatives. This is more common with higher-tier plans from established companies.

Understanding how home warranty companies decide to repair vs. replace an item is also key — because a replacement decision at a low cap can leave you with a much larger bill than a repair would have.

Providers With the Highest Payout Limits

Not all home warranty companies treat caps the same way. Premium providers offer significantly higher — and in some cases, unlimited — coverage on major systems. Here's how the top companies compare:

Top Providers by Payout Generosity (2026)

First American Home Warranty stands out with unlimited coverage on HVAC, electrical, and plumbing repairs on its premium plans — meaning there is no dollar ceiling if your claim is approved. For appliances, it offers $3,500 to $7,000 per item depending on your plan tier.

American Home Shield (AHS) offers the highest overall annual payout limit at up to $50,000 across all claims within a 12-month agreement. AHS pays up to $5,000 for HVAC, $3,000 each for electrical and plumbing, and $2,000–$4,000 per appliance depending on your selected plan.

Old Republic Home Protection provides no cap on electrical repairs and up to $6,500 per HVAC system, with appliance limits reaching $3,500–$7,000 on higher-tier plans.

For a full cost-to-value breakdown, see our home warranty cost guide for 2026 which compares premium pricing against payout potential across major providers.

Coverage Caps vs. Actual Replacement Cost

There's a critical distinction every homeowner must understand: your home warranty's coverage cap is not the same as the item's actual replacement cost — and the gap between the two is where most financial surprises happen.

Coverage cap = The fixed maximum your warranty will pay, as defined in your contract. Actual replacement cost = The real current market cost to repair or replace the item with a new equivalent.

Does Home Warranty Depreciation Apply?

Unlike homeowners insurance, which often pays on an actual cash value (ACV) basis by subtracting depreciation from the item's age and useful life, most home warranties do not formally depreciate items. Your HVAC is not paid out at 60 cents on the dollar because it's 10 years old — the warranty simply pays up to its cap and stops.

However, this doesn't mean you're protected from depreciation's effect. If your plan's cap is already lower than a new replacement cost, the age of your system has essentially the same financial impact — you're still paying a large portion out of pocket.

| Item | Actual Replacement Cost | Typical Cap | Your Out-of-Pocket Gap |

|---|---|---|---|

| Central HVAC System | $7,000–$12,000 | $2,000–$5,000 | $2,000–$10,000 |

| Refrigerator (high-end) | $2,500–$4,500 | $1,000–$2,500 | $0–$3,500 |

| Washer + Dryer Set | $1,800–$3,500 | $1,000–$2,000 each | $0–$1,500 |

| Water Heater (tankless) | $3,000–$5,000 | $1,000–$2,000 | $1,000–$4,000 |

| Electrical Panel | $2,500–$5,000 | $1,500–$3,000 | $0–$3,500 |

For a deeper look at how replacement value works compared to actual cash value in related insurance products, read our guide on replacement cost vs. actual cash value in home insurance.

Is a Home Warranty Worth Buying Given Payout Limits?

Here's the honest framework for evaluating whether a home warranty's payout limits make it financially worthwhile for your situation:

Step 1: List Your High-Risk Items

Write down the age and condition of your HVAC, water heater, major appliances, and home systems. Older items (10+ years) carry higher replacement risk. Review what HVAC coverage your warranty plan includes to understand how your biggest expense is treated.

Step 2: Compare Caps to Real Local Costs

Look up current replacement costs in your market. HVAC replacement in high cost-of-living areas can run $10,000–$13,000+. If a plan's HVAC cap is $2,000 in a $10,000 market, the warranty provides limited protection on your biggest risk.

Step 3: Run the Math

Add up: Annual premium + estimated service fees vs. probability of a claim × (real repair cost − cap)

If your expected out-of-pocket after the cap is consistently higher than your annual premium, a higher-tier plan or a dedicated repair savings account may serve you better. Compare your options in our home warranty vs. saving money analysis.

Step 4: Prioritize Plans With Higher Caps on Your Biggest Risks

If you can't afford the highest-tier plan, at minimum target the highest cap available for your most expensive at-risk system — typically HVAC.

Understanding how the claims process works from start to finish can also help you avoid surprises when it's time to actually use your coverage.

Frequently Asked Questions

What is the average home warranty payout limit per item?

Per-item caps range widely, but most mid-tier plans set limits between $1,500 and $3,000 for appliances and $2,000 to $5,000 for major systems like HVAC. Low-cost plans can be as low as $500–$1,000 per item, while premium plans from companies like First American and American Home Shield go up to $7,000 per appliance or offer unlimited system coverage. Always check the "Limit of Liability" section in your specific contract, as limits vary even within the same company's plan lineup.

What happens if my repair cost is more than my home warranty will pay?

You are responsible for paying the difference between the warranty's coverage cap and the actual repair or replacement cost. This applies even on fully approved claims — the cap is not a negotiating point once set in your contract. Some providers may offer a cash-out settlement as an alternative to a repair that exceeds the cap, but the amount offered is typically based on the company's internal wholesale rates, not retail pricing.

Do home warranty companies apply depreciation to payouts?

Most home warranty plans do not apply formal depreciation to their payouts — they pay up to the coverage cap without reducing the amount based on the item's age. This differs from homeowners insurance, which may use actual cash value (ACV) and subtract depreciation. However, since caps are often already lower than full replacement cost, older systems and appliances may still leave homeowners with significant out-of-pocket expenses regardless.

Which home warranty companies offer the highest payout limits?

First American Home Warranty, American Home Shield, and Old Republic Home Protection are the top-tier providers for payout limits in 2026. First American offers unlimited coverage on HVAC, plumbing, and electrical on its premium plans. American Home Shield provides up to $5,000 for HVAC, $3,000 for plumbing and electrical, and an annual aggregate limit of up to $50,000. Old Republic caps HVAC at $6,500 and appliances up to $7,000 on select plans.

How do annual aggregate home warranty limits work?

An annual aggregate limit is the maximum dollar amount your warranty will pay across all claims combined during a 12-month contract period. For example, if your plan has a $15,000 aggregate cap and you file claims totaling $14,000 before December, only $1,000 remains for additional claims that year — no matter how large the next repair is. Annual aggregate limits range from roughly $10,000–$25,000 on most plans, with top-tier options like American Home Shield reaching $50,000.