Compare Home Warranty Options in Ohio

See what plans you qualify for in less than 2 minutes

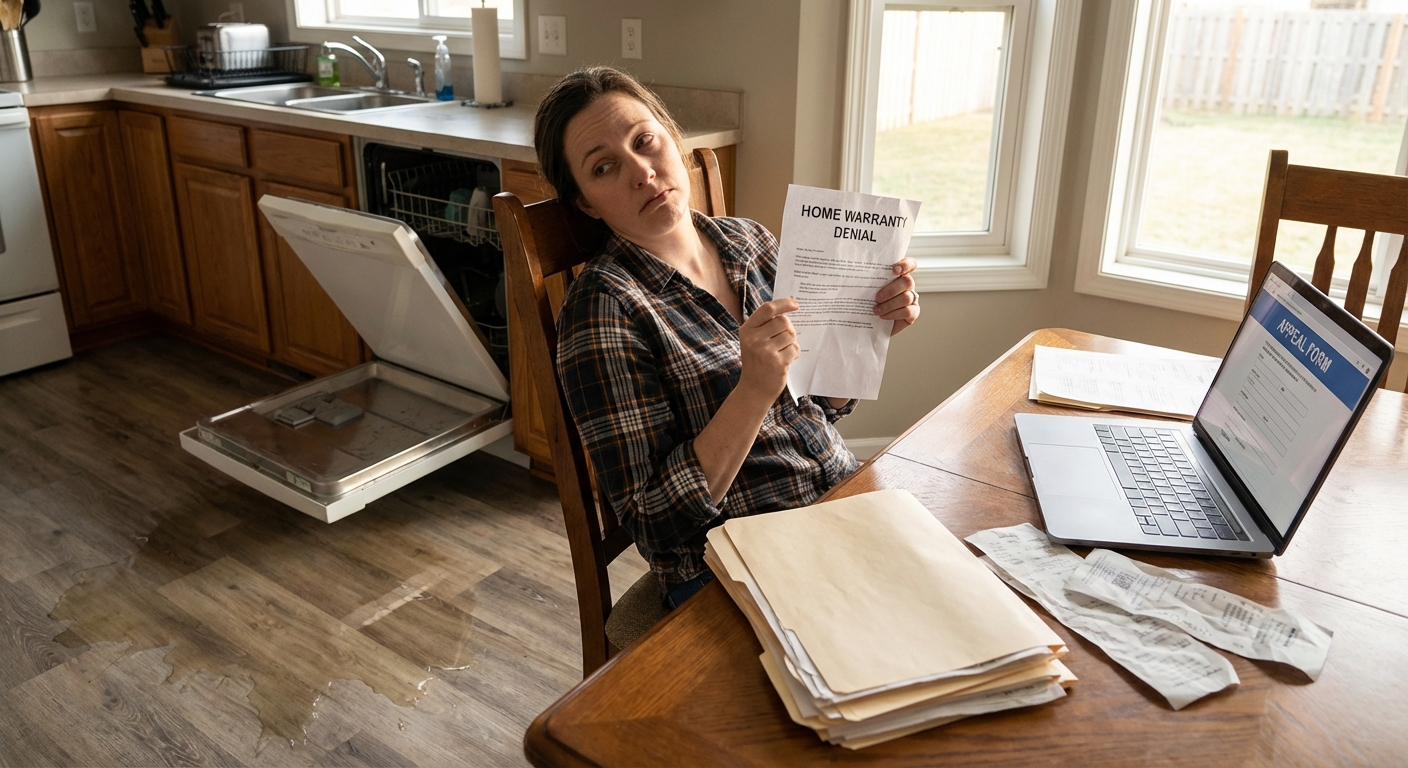

The Most Common Reasons Home Warranty Claims Are Denied

Getting your home warranty claim denied is frustrating, but it happens far more often than most homeowners expect. Understanding why companies reject claims is the first step to either preventing a denial or successfully fighting one. According to a 2026 This Old House survey of 2,000 homeowners, the four leading reasons for denial are pre-existing conditions (29%), items not covered under the plan (29%), repair costs exceeding coverage limits (20%), and lack of maintenance (13%). Below is a breakdown of each major denial trigger.

Pre-Existing Conditions

Home warranty plans are designed to cover new and unforeseen breakdowns that occur after your coverage begins. If a home warranty company determines that an appliance or system had a defect or needed repair before you purchased the policy, they can (and typically will) deny the claim entirely. This single reason accounts for nearly 3 in 10 denials in 2026, making it the most common cause of rejection alongside non-covered items.

Pro tip: Always get a professional home inspection before purchasing a warranty. Issues flagged in an inspection report can be addressed upfront, reducing your risk of a pre-existing condition denial later.

Lack of Maintenance or Neglect

Home warranty companies require that covered systems and appliances receive routine upkeep. If the company's inspector determines that your failure to maintain the item contributed to the breakdown, your claim will likely be denied. This applies to HVAC filters not being changed regularly, water heaters not being flushed annually, or a dishwasher damaged through misuse.

Learn more about home warranty maintenance requirements to understand exactly what's expected of you as a homeowner.

Improper Installation

If a covered item was installed incorrectly, whether by a previous homeowner or an unlicensed contractor, the warranty company may deny the claim on the grounds that the failure wasn't caused by normal wear and tear. Always verify that any installation work in your home was performed by a licensed professional and that permits were pulled where required.

Non-Covered Items & Policy Exclusions

Many denials come down to a simple mismatch: the homeowner assumed something was covered, but it wasn't. Home warranty policies are filled with exclusions, from cosmetic components to structural elements to specific parts within a covered appliance. For a deep dive into what's typically left out, see our guide on home warranty exclusions.

Exceeding Coverage Limits

Even when a claim is valid, your payout may be capped. In 2026, most providers cap HVAC coverage between $1,500 and $5,000 per system, while appliance caps generally run $500 to $2,000 per item (some premium plans go up to $4,000). About 20% of denied claims in 2026 were rejected because repair costs exceeded those limits. Review home warranty coverage limits so you know your financial exposure before a breakdown happens.

Other Common Denial Triggers

| Denial Reason | What It Means |

|---|---|

| Unauthorized Repairs | Using non-approved technicians voids coverage |

| Code Violations | Repairs not compliant with local building codes |

| Delayed Reporting | Waiting too long to file after an issue occurs |

| Animal / Pest Damage | Excluded as not a direct mechanical breakdown |

| Secondary Damage | Damage resulting from a covered failure may not be covered |

| Lapsed Premiums | Missed payments give the company no obligation to pay |

How to Dispute a Denied Home Warranty Claim

A denial is not always the final word. Many homeowners successfully overturn decisions by following a structured appeal process with solid documentation. Here's how to do it.

Step 1: Review the Denial Letter Carefully

Read the denial notice thoroughly and identify the exact reason given. Then pull out your warranty contract and compare the stated reason against your actual policy language. Look for inconsistencies, vague wording, or clauses that may actually support your position. Understanding how the claims process works will help you spot discrepancies faster.

Step 2: Gather Your Documentation

Strong documentation is the backbone of a successful appeal. Compile the following before contacting your provider:

- Warranty contract and denial notice (in writing)

- Maintenance records including receipts, service logs, and technician notes

- Photos and videos of the damaged item and surrounding area

- Purchase receipts or installation records for the item in question

- The company's initial inspection report

- A second opinion from an independent, licensed contractor

Step 3: Submit a Formal Written Appeal

Contact your home warranty provider and request their official appeal process and required forms. Submit everything in writing and never rely solely on phone conversations. Include all supporting documents, reference specific contract language that supports coverage, and be factual and concise. Most providers respond to formal appeals within 5 to 10 business days, though full resolution can stretch to 30 days or more.

Step 4: Follow Up Persistently

Appeals can take time. Follow up regularly, document every interaction (name, date, time, summary), and don't let the process go cold. Persistence matters since many claims are approved after a homeowner pushes back with new evidence.

When to Escalate: Management, Regulators & Legal Action

If your internal appeal fails, you have several escalation options, each progressively stronger. Knowing your home warranty arbitration rights before escalating is critical.

Escalate to Senior Management

Before going external, ask to speak with a supervisor or claims manager. Sometimes a denial is reversed simply because a higher-level employee re-reviews the file with fresh eyes. Be calm, professional, and come armed with your documentation.

File a Complaint With Regulatory Agencies

After exhausting the provider's internal process, file complaints with the right state agency, which varies based on how your state classifies home warranties:

- State Insurance Department (e.g., California, Florida) where warranties are regulated as home protection contracts

- State Real Estate Commission (e.g., Texas) where warranties are overseen as service contracts

- Department of Financial Services (e.g., New York) for states that regulate them as service contracts

- Attorney General's Consumer Protection Division which works in nearly every state

- The Better Business Bureau (BBB) to create public pressure (American Home Shield alone has logged over 16,000 BBB complaints in the last 3 years)

When to Consider Legal Action

Legal action should be a last resort, but it's sometimes warranted. The 2019 Lamps Plus v. Varela Supreme Court decision made it harder to force class arbitration unless the contract clearly authorizes it, so most consumers are limited to individual arbitration or small claims court. Consider consulting a consumer protection or contract attorney if:

- Internal appeals and arbitration (if required) have been exhausted

- The company clearly denied a claim that your contract covers

- The dollar amount justifies legal costs (typically $3,000+)

- You have clear evidence of a contract breach or bad-faith practices

For issues with chronically bad providers, our guide on home warranty companies to avoid can help you identify patterns of systemic denials. You can also learn more about suing a home warranty company in small claims court.

How to Prevent Home Warranty Claim Denials

The best dispute is the one you never need to have. Taking proactive steps dramatically reduces your risk of a denial.

Read Your Policy Before You Need It

Most homeowners don't read their warranty contract until after a claim is filed, by which point it's too late. Review your policy when you first purchase it, identify every exclusion, note all coverage caps, and understand exactly what maintenance is required to keep your coverage valid. Our guide on how to read a home warranty contract walks you through every section. If a plan's exclusions are excessive, compare options in our best home warranty companies guide which ranks providers by approval rates.

Keep a Maintenance Log

Routine maintenance is your best protection against denial. Keep a running log of every service, inspection, and repair performed on your home's major systems and appliances. Store receipts, invoices, and technician reports in a dedicated folder, physical or digital.

| System / Appliance | Recommended Maintenance Frequency |

|---|---|

| HVAC (filter change) | Every 1-3 months |

| HVAC (professional tune-up) | Annually |

| Water Heater (flush) | Annually |

| Plumbing (inspection) | Every 2 years |

| Roof (inspection) | Annually |

| Refrigerator (coil cleaning) | Every 6-12 months |

Use Approved Contractors Only

Never hire an outside technician to diagnose or repair a covered item without first getting authorization from your home warranty company. Using unauthorized contractors is one of the fastest ways to have a claim denied, even if the work was done correctly. If you must pay out of pocket in a true emergency, review home warranty reimbursement rules so you understand what you can recover.

Report Issues Promptly

File your claim as soon as a problem arises. Most policies have windows for reporting, and delays can be used as grounds for denial. When you file, be specific: describe the symptoms, when they started, and the item's make, model, and serial number.

If you're evaluating whether a home warranty is even the right financial move at $28 to $191 per month in 2026, consider how repair vs. replace decisions play out before you renew.

Frequently Asked Questions

Can a home warranty deny a claim for a pre-existing condition on a newly purchased home?

Yes. Home warranty companies can and do deny claims for pre-existing conditions even on newly purchased homes, and this reason accounts for roughly 29% of all denials in 2026. If the inspector determines that a system or appliance showed signs of wear, damage, or malfunction before your coverage began, the claim is typically considered ineligible. The best protection is a thorough home inspection before purchasing your home and your warranty, so that known issues can be documented and addressed upfront.

What documentation do I need to appeal a denied home warranty claim?

You'll want to gather your warranty contract, the written denial notice, maintenance logs and service receipts, photos and videos of the damaged item, the company's inspection report, and any purchase or installation records for the item. If the denial cites improper maintenance or installation, a second opinion from an independent, licensed contractor is especially valuable. The stronger your documentation, the better your chances of reversing the decision.

How long does the home warranty appeal process take?

Timelines vary by provider, but most companies respond to formal appeals within 5 to 10 business days of receiving your submission. If internal escalation, arbitration, or mediation are involved, the process can stretch to 30 to 90 days. Document every interaction with the company, including dates, names, and conversation summaries, and follow up regularly to keep your case from stalling.

What happens if my repair costs exceed my home warranty coverage limit?

If your repair or replacement cost exceeds your plan's coverage cap, you are responsible for paying the difference out of pocket. In 2026, HVAC caps typically range from $1,500 to $5,000 per system, while appliance caps run $500 to $2,000 per item on standard plans (up to $4,000 on premium tiers like American Home Shield's ShieldPlatinum). Always check your plan's per-item limits before a breakdown so you're not caught off guard.

When should I consider switching home warranty companies after a denial?

If your claim was denied based on vague or overly broad exclusions, if the company has a pattern of denying legitimate claims, or if customer service has been consistently unresponsive, it may be time to switch. Look for providers with high BBB ratings, transparent contract language, and strong independent reviews (Liberty Home Guard and Old Republic Home Protection consistently rank highest for satisfaction in 2026). Before switching, make sure you understand your home warranty cancellation rights including any fees or prorated refund policies.