Ohio Life Insurance - Save up to 70% Off

See what plans you qualify for in just a few minutes

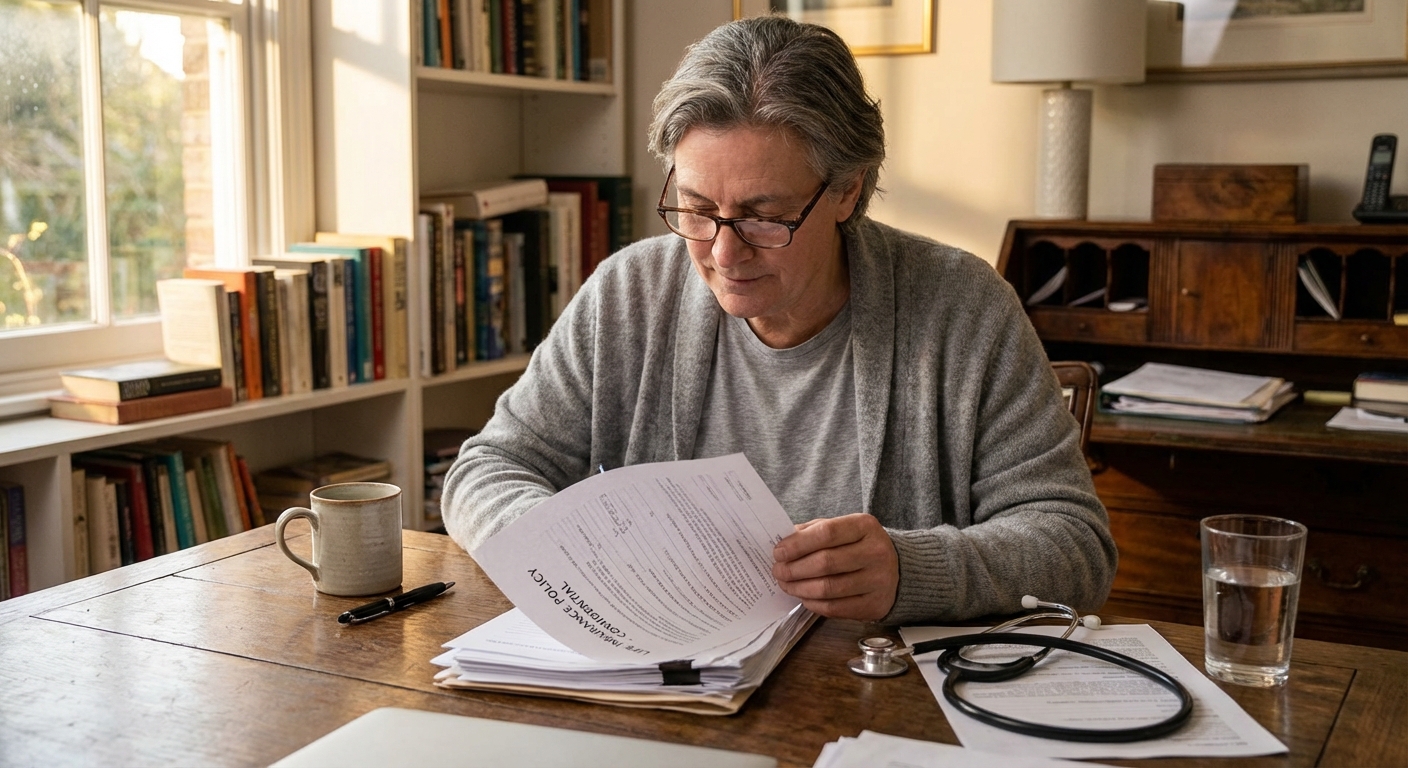

How a Viatical Settlement Works

A viatical settlement is a financial transaction in which a terminally or chronically ill life insurance policyholder (called the viator) sells their policy to a licensed third-party buyer in exchange for an immediate lump-sum cash payment. The buyer assumes ownership of the policy, takes over premium payments, and ultimately collects the full death benefit when the insured passes away.

The step-by-step process typically looks like this:

- Application & Review. The viator contacts a viatical settlement provider or broker, who reviews the policy type, face value, and the insured's medical condition.

- Medical Underwriting. Medical records, physician statements, and life expectancy estimates are assessed to determine the offer amount.

- Competitive Bidding. The case is often shopped to multiple institutional buyers to secure the best offer.

- Offer Acceptance. The viator reviews one or more offers and, if satisfied, signs closing documents through a secure escrow process.

- Transfer & Funding. Ownership and beneficiary rights transfer to the buyer, and the viator typically receives funds within 3 to 5 business days after closing.

Who Qualifies for a Viatical Settlement in 2026?

To qualify, a policyholder generally must meet these criteria:

- Terminal illness with a physician-certified life expectancy of 24 months or less, OR be chronically ill (unable to independently perform at least two activities of daily living for 90+ days, or with severe cognitive impairment)

- Policy must have been in force for at least 2 years (past the contestability period). Some states apply longer waiting periods (the NAIC model uses a 5-year waiting period with enumerated exceptions such as divorce, retirement, or loss of employment)

- Minimum face value typically $100,000 (varies by provider)

- The policy must be assignable to another owner

Unlike standard life settlements (which usually require the insured to be 65+), viatical eligibility is driven by health status, not age. For a deeper look at how health affects coverage, read our guide on life insurance with pre-existing conditions.

Which Policy Types Are Eligible?

Both term and permanent life insurance policies may qualify, though permanent policies are generally preferred by buyers.

| Policy Type | Eligible? | Notes |

|---|---|---|

| Whole Life | ✅ Yes | Highly preferred; has cash value |

| Universal Life | ✅ Yes | Highly preferred; flexible permanent coverage |

| Term Life | ✅ Conditional | Must be convertible or have sufficient remaining term |

| Variable Life | ✅ Conditional | Reviewed case-by-case |

| Group Life | ⚠️ Sometimes | Depends on ownership rights and face value |

Ohio Life Insurance - Save up to 70% Off

See what plans you qualify for in just a few minutes

Viatical Settlement Payout: How Much Can You Expect in 2026?

Payout amounts depend on several factors, including your life expectancy, the policy's face value, current premiums, and the insurer's financial strength. The shorter your life expectancy, the higher your offer, because the buyer will wait less time to collect the death benefit.

The NAIC Model Act sets minimum payment guidelines that most licensed providers follow as a floor. These minimums can be reduced by up to 5 percentage points for policies issued by lower-rated insurers (below the four highest A.M. Best categories):

| Life Expectancy | NAIC Minimum Payout | Typical 2026 Market Range |

|---|---|---|

| Less than 6 months | 80% of net face value | 70 to 85% |

| 6 to 12 months | 70% of net face value | 65 to 75% |

| 12 to 18 months | 65% of net face value | 55 to 70% |

| 18 to 24 months | 60% of net face value | 50 to 60% |

| 24 to 36 months | 50% of net face value | 40 to 55% |

According to 2026 industry data, viatical settlement proceeds typically fall between 50% and 85% of the death benefit, with offers at the upper end for insureds with the shortest life expectancies. That's dramatically higher than the average cash surrender value, which hovers around just 3% to 5% of the death benefit. Compared to simply surrendering a cash value life insurance policy to the carrier, a viatical settlement can pay roughly 6 to 8 times more.

Viatical Settlement vs. Life Settlement vs. Accelerated Death Benefit

Before committing to a viatical settlement, it's important to understand your three main options for accessing life insurance value while still living.

For more on selling a policy when you're not terminally ill, see our life settlement guide, which includes LISA's 2025 market data (released May 19, 2026) showing an average payout of $212,066 per policy, an 8.71x multiple over the average cash surrender value of $24,360, across 2,955 completed transactions.

Accelerated Death Benefit (ADB): Your Third Option

An accelerated death benefit is a rider built into many life insurance policies that allows you to access a portion of your own death benefit directly from your insurer, with no third-party sale required. Key differences:

- Policy ownership stays with you so your beneficiaries still receive the remaining death benefit

- No competitive bidding. The insurer sets the payout, typically capped at 50% to 80% of the death benefit (Mutual of Omaha, for example, offers up to 80% chronic illness acceleration)

- Generally tax-free for terminal illness under IRC Section 101(g)

- Availability depends on your specific policy terms

Learn more about how living benefits and ADB riders work and what conditions qualify, or explore the related critical illness rider option. If you need long-term care support specifically, our chronic illness rider guide explains how ADL-based triggers work.

When does a viatical settlement make more sense than ADB?

- Your policy doesn't include an ADB rider

- The ADB payout cap is too low to meet your financial needs

- You want the highest possible lump sum and are willing to give up beneficiary rights

Tax Implications and Federal Rules in 2026

One of the biggest advantages of a viatical settlement over a standard life settlement is the favorable tax treatment under IRC Section 101(g), which was created by the Health Insurance Portability and Accountability Act (HIPAA) of 1996.

- Terminally ill policyholders (physician-certified life expectancy of 24 months or less): Proceeds are generally 100% tax-free at the federal level, treated as an amount paid by reason of death

- Chronically ill policyholders: Proceeds are tax-free only if used for qualifying medical, long-term care, or custodial care expenses, or up to the IRS per-diem cap. For 2026, IRS Rev. Proc. 2025-32 sets the per-day exclusion limit at $430 per day (roughly $13,079 per month), up from $420 in 2025, under IRC Section 7702B(d)(4)

- State taxes: Most states follow federal guidelines, but rules vary. Always verify with your state's insurance department

For a broader look at life insurance taxation, including 2026 federal estate tax rules (now permanent at $15 million per person under the One Big Beautiful Bill Act), see our guide on is life insurance taxable.

Choosing a Reputable Viatical Settlement Company

Not all viatical settlement providers operate with the same level of transparency or ethics. Here's how to protect yourself:

- ✅ Verify state licensing with your state's insurance department to confirm the provider and any broker are properly licensed

- ✅ Request multiple offers. A reputable broker will shop your policy to multiple institutional buyers

- ✅ Review all contracts carefully. Look for clear disclosures on compensation and ownership transfer

- ✅ Use an attorney or financial advisor. An independent expert can help you evaluate offers

- ✅ Check complaint history by searching the provider's name with your state insurance commissioner and the NAIC database

- ✅ Insist on escrow through a bank that is not affiliated with the buyer

Red Flags to Watch For

Viatical settlement fraud remains a chronic regulatory concern. State securities regulators have brought at least 191 cease-and-desist or enforcement actions related to viatical sales since 1994, and current warnings still target the same patterns seen in historic scandals like the Mutual Benefits Corp. billion-dollar Ponzi case. Common schemes involve fabricated medical records, manipulated life expectancy reports, and "guaranteed return" pitches. If something feels off, walk away. To learn how investor-side fraud differs from legitimate transactions, read about stranger-originated life insurance (STOLI) risks.

State Regulations in 2026

Viatical settlements are regulated at the state level under frameworks patterned after the NAIC Viatical Settlements Model Act (MDL-697), last comprehensively revised in 2007. Common requirements include:

- Written contracts with full disclosure of all terms and alternatives (including ADB riders and policy loans)

- Mandatory rescission (cancellation) periods: under the NAIC model, viators have the right to rescind until the earlier of 60 calendar days after execution or 30 calendar days after proceeds are paid. Florida law, by contrast, sets a 15-day rescission window

- Financial responsibility through a surety bond or deposit of $250,000 under the 2007 NAIC revisions

- Broker continuing education (15 hours every two years under NAIC commentary) and fiduciary duty to the viator

- Prohibition on fraudulent acts including misrepresentation, embezzlement, and falsifying life expectancy reports

Recent state activity confirms these rules remain active in 2026. Iowa updated its administrative rules (Chapter 48) in July 2026, and West Virginia refreshed Article 13C in May 2026, both reinforcing the requirement that viatical contracts be executed only by providers licensed in the viator's state of residence. Always verify the specific rules in your state through your state insurance commissioner's website.

Pros and Cons of a Viatical Settlement

Before selling, compare your offer against the cash surrender value of your policy. You can also explore borrowing against your life insurance policy as an alternative way to access funds without giving up the policy, with current 2026 policy loan rates ranging from 4% to 8% depending on the carrier (Northwestern Mutual and New York Life around 5%, MassMutual and Guardian at 5% to 6%).

Frequently Asked Questions

What is a viatical settlement in simple terms?

A viatical settlement is when a person who is terminally or chronically ill sells their life insurance policy to a third-party company for immediate cash, usually 50% to 85% of the policy's death benefit. The buyer takes over the policy, pays any remaining premiums, and collects the death benefit when the insured passes away. It's a way to access money you'd otherwise never see while you're alive.

How is a viatical settlement different from a life settlement?

The key difference is the health status and life expectancy of the policyholder. A viatical settlement is specifically for people who are terminally or chronically ill with a life expectancy of 24 months or less, and typically pays 50% to 85% of the death benefit. A standard life settlement is for seniors 65+ who are not terminally ill and generally pays 10% to 25% of the death benefit, though LISA's 2025 data shows the average completed settlement was $212,066, nearly 9 times the average cash surrender value.

Are viatical settlement proceeds taxable in 2026?

For terminally ill policyholders with a physician-certified life expectancy of 24 months or less, viatical settlement proceeds are generally 100% tax-free at the federal level under IRC Section 101(g). For chronically ill policyholders receiving periodic payments, the proceeds are tax-free up to the 2026 per-diem cap of $430 per day set by IRS Rev. Proc. 2025-32, or fully excludable if used for qualifying long-term care expenses. The buyer must also be a licensed viatical settlement provider for the exclusion to apply.

What life insurance policies qualify for a viatical settlement?

Most types of life insurance policies can qualify, including whole life, universal life, variable life, and convertible term life insurance. Term policies are eligible if they are convertible or have a sufficient remaining term, and most providers require a face value of $100,000 or more. The policy must also have been in force for at least two years (past the contestability period) and be legally assignable to a new owner.

How do I find a reputable viatical settlement company?

Start by verifying that any provider or broker is licensed in your state through your state's insurance commissioner and the NAIC database. Work with a licensed broker who can solicit multiple offers on your behalf, since brokers are legally obligated to act in your best interest. Avoid any company that pressures you to decide quickly, refuses to provide written disclosures, promises "guaranteed" returns, or asks you to skip the escrow process.