Ohio Life Insurance - Save up to 70% Off

See what plans you qualify for in just a few minutes

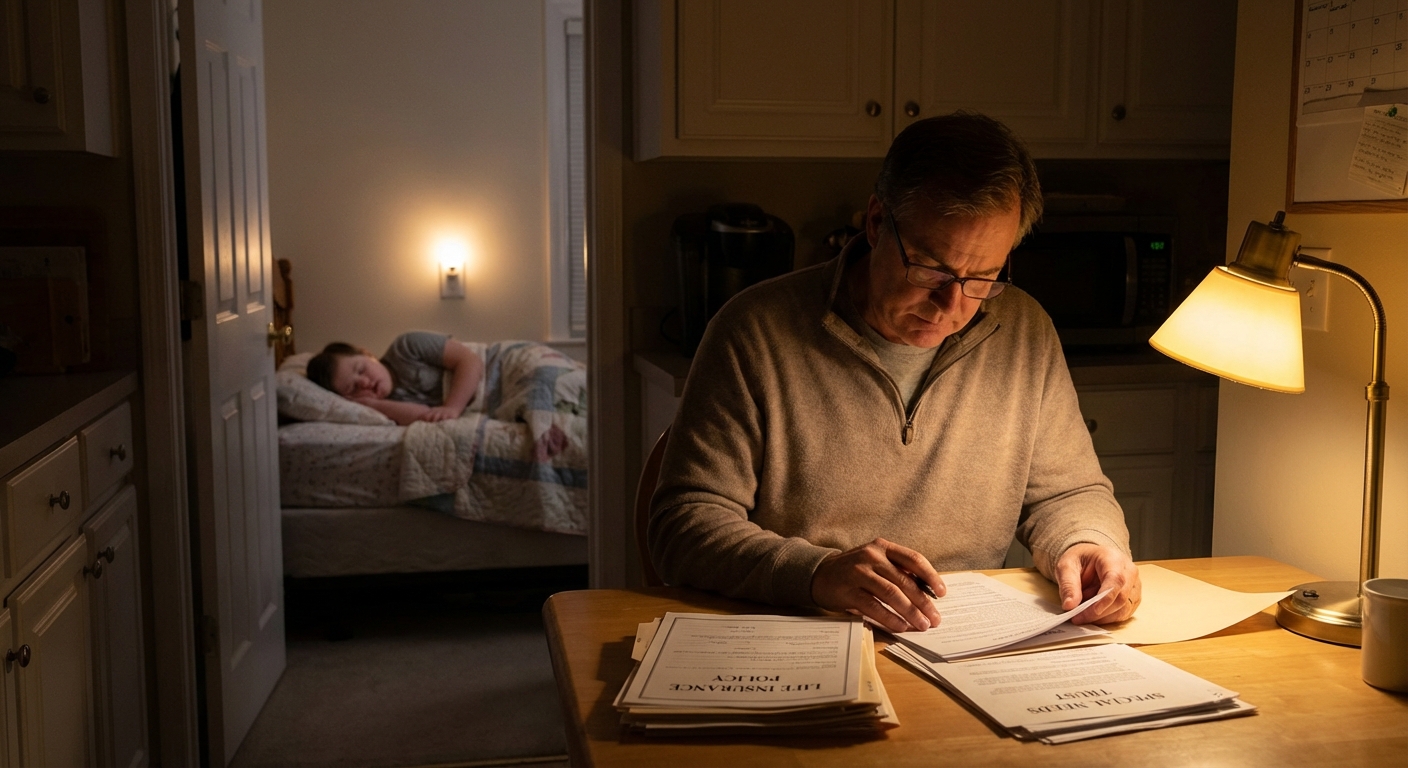

Why Parents of Special Needs Children Need Life Insurance

For most families, life insurance replaces income and pays off debts. For parents of children with disabilities, it does something far more critical. It funds a lifetime of care that no one else may provide. Unlike typical children who grow into financial independence, many special needs children require housing, medical support, therapy, and daily care indefinitely.

Without proper planning, a parent's death can trigger a financial crisis. The SSI countable resource limit remains $2,000 for an individual and $3,000 for a couple in 2026, unchanged since 1989 despite decades of inflation. If life insurance proceeds are paid directly to the child, they can push assets above that $2,000 threshold, immediately disqualifying them from Supplemental Security Income (SSI) and Medicaid. A special needs trust (SNT) funded by life insurance solves this problem by holding assets outside the child's name, preserving benefit eligibility while still providing for supplemental care needs.

The financial stakes are enormous. According to Autism Speaks data widely cited by financial planners, the estimated cost to raise a child with autism or an intellectual/developmental disability is $1.4 to $2.4 million, and the more severe the disability, the more expensive the lifetime cost. When you factor in housing, therapies, attendant care, and inflation over a 40 to 60 year horizon, lifetime supplemental needs for a moderate to severe disability commonly fall in the $2 to $3 million range in 2026 dollars. Life insurance is one of the most affordable and efficient ways to fund that gap.

Ohio Life Insurance - Save up to 70% Off

See what plans you qualify for in just a few minutes

How Much Life Insurance Do You Need for a Special Needs Trust?

There is no single "right" number. Coverage should be calculated based on the projected lifetime supplemental needs of your child. Here are the key factors that drive the coverage amount:

| Factor | Why It Matters |

|---|---|

| Estimated lifetime care costs | Housing, therapies, medical, and personal care can total $1.4M to $3M+ over decades |

| Current income and assets | Higher-earning families may need more to maintain the child's current lifestyle |

| Child's life expectancy | Longer horizons demand significantly more funding |

| Government benefits already in place | In 2026 SSI pays a maximum federal benefit of $994 per month for an individual and $1,491 per month for an eligible couple, so SNT funds must cover most supplemental needs |

| Inflation (3 to 5% annually) | Medical and long-term care inflation typically outpace CPI |

| Number of caregivers | Two-parent households may combine policies to build a larger safety net |

A financial planner or special needs attorney can help you model the exact amount needed. As a general benchmark, experts commonly recommend that parents target $500,000 to $1.5 million or more in life insurance coverage directed to the SNT, depending on the child's needs and the family's existing assets.

Learn more about calculating your coverage needs using proven formulas like the DIME method.

Choosing the Right Policy: Term vs. Whole Life vs. Second-to-Die

Not all life insurance types are equally suited for funding a special needs trust. Here's how the three main options compare:

Whole Life Insurance

Whole life provides permanent, guaranteed coverage as long as premiums are paid. It builds a cash value component that grows tax-deferred and can be accessed if needed. Based on 2026 industry data, a $250,000 whole life policy averages roughly $238 per month for a healthy 30-year-old man and $206 per month for a healthy 30-year-old woman, rising to $355 per month for a 40-year-old man and $543 per month at age 50. Women typically pay 15 to 25% less than men at every age due to longer life expectancy. For single parents or those with a special needs child who will require lifelong care, whole life is often the most reliable SNT funding tool because the death benefit will be there regardless of when the parent dies.

Second-to-Die (Survivorship) Life Insurance

Second-to-die policies cover two lives (typically both parents) and pay the death benefit only after both insureds have passed. This is often the most cost-effective option for married couples because:

- Premiums are typically 30 to 50% lower than two individual permanent policies

- The payout timing naturally aligns with when the SNT will need to be fully funded (after both parents are gone)

- It's easier to qualify medically since both lives are insured together

Learn more about how survivorship life insurance works as an estate planning tool for couples.

Term Life Insurance

Term life can work as a temporary bridge, especially for young parents on a tight budget who plan to transition to permanent coverage later. However, it carries the real risk that the policy expires before the parent passes. If your child will need support for 40+ years, term alone is rarely sufficient.

First-Party vs. Third-Party Special Needs Trusts

Understanding which type of SNT you're funding is essential before naming it as a life insurance beneficiary.

| Feature | First-Party SNT | Third-Party SNT |

|---|---|---|

| Funded by | The beneficiary's own assets (e.g., lawsuit settlement, inheritance) | Parents, family members, or life insurance |

| Age limit | Beneficiary must be under age 65 when the trust is established | No age restriction |

| Medicaid payback | Federal law mandates a Medicaid payback provision; at death, remaining assets must first reimburse the state for Medicaid benefits paid | None, remaining assets pass freely to other heirs |

| Best used for | Sudden windfalls the child receives | Long-term family planning and life insurance proceeds |

| Flexibility | More restrictive | More flexible for estate planning |

For life insurance purposes, you will almost always use a third-party SNT. Because the policy is owned and funded by the parent, not the child, the proceeds are considered third-party assets. This gives the trust far more flexibility and eliminates the Medicaid payback requirement, so remaining assets can pass to other family members, charities, or future beneficiaries at the trust creator's discretion. Learn more about using a trust as beneficiary and when it makes sense.

How to Name the Special Needs Trust as Beneficiary

Naming the SNT correctly on your life insurance policy is one of the most important steps in this entire process. A mistake here can send funds directly to your child, triggering benefit disqualification.

Step-by-step process:

- Establish the SNT first. The trust must exist before you can name it as a beneficiary. Work with a special needs attorney to draft and execute the trust document.

- Obtain the trust's EIN (Employer Identification Number). Required by most insurers for trust beneficiary designations.

- Contact your insurance company. Request their beneficiary designation form and any required trust certification form.

- Provide the full trust name, creation date, trustee name(s), and EIN on the form.

- Submit and confirm. Get written confirmation that the designation has been recorded correctly.

- Review every 3 to 5 years. Life events, policy changes, and trust amendments can require updates.

For a deeper look at beneficiary designation rules and common errors, see our guide on beneficiary mistakes to avoid that could cost your family thousands. Parents of minor children should also review naming a minor as beneficiary for related guardianship issues.

Coordinating With ABLE Accounts (Major 2026 Expansion)

A powerful complement to a life insurance funded SNT is an ABLE account. The January 1, 2026 expansion under the ABLE Age Adjustment Act makes these accounts more useful than ever. As of January 1, 2026, you may open an ABLE account if your disability began before age 46 (up from the previous age 26 threshold), and the annual contribution limit increased to $20,000.

The National Disability Institute projects about 6 million more people will qualify, with total eligibility growing to roughly 14 million Americans, up from about 8 million. Additional 2026 rules families should know:

- ABLE Account Owners in the continental U.S. who work and do not participate in an employer-sponsored retirement plan may contribute up to an additional $15,650 (or their earnings, whichever is less) into their ABLE account

- Up to $100,000 in ABLE savings is disregarded as a resource and will not affect Supplemental Security Income eligibility, and any Medicaid benefit including Medicaid waiver services is preserved even above that level

- 529-to-ABLE rollovers and the Saver's Credit for ABLE contributions are now permanent under the recent updates

This means families can use both tools together:

- SNT (funded by life insurance): holds larger lump sums and provides long-term supplemental support

- ABLE account: provides tax-free growth for everyday disability expenses and can accept trust distributions the beneficiary controls

Tax Implications & Government Benefit Coordination

Tax Treatment of Life Insurance Proceeds in an SNT

Life insurance death benefits paid to a properly structured third-party SNT are:

- Income tax-free under IRC §101(a)

- Outside the child's countable assets for SSI and Medicaid purposes

- Not subject to probate (the proceeds bypass the estate entirely)

This makes life insurance one of the cleanest and most tax-efficient funding mechanisms available for a special needs trust. Learn more about when life insurance is taxable and the exceptions to watch for.

Staying Eligible for SSI and Medicaid

An important 2024 SSA rule change still applies in 2026: the federal in-kind support and maintenance (ISM) rule removed food from the in-kind support definition, so trusts can now pay for groceries without reducing SSI. The trust must still be drafted with careful language to ensure other distributions don't reduce government benefits:

| Distribution Type | Effect on SSI/Medicaid |

|---|---|

| Direct cash payments to the child | Counts as income, reduces SSI benefit |

| Paying rent or utilities directly | Triggers "in-kind support", can reduce SSI by up to one-third |

| Paying for groceries and food | Now allowed (no reduction to SSI) |

| Paying for therapy, recreation, tech | Generally allowed without affecting benefits |

| Paying for medical not covered by Medicaid | Generally allowed, must coordinate with Medicaid rules |

The trustee should always pay service providers directly rather than giving cash to the beneficiary. For families navigating long-term care planning, our guide on life insurance and Medicaid eligibility covers these interactions in more depth, including California's Medi-Cal asset test changes.

SECURE Act 2.0 Coordination for Retirement Assets

If you also plan to leave retirement accounts (IRA, 401k) to the SNT, work with your attorney to preserve Eligible Designated Beneficiary (EDB) status for your disabled child. A disabled beneficiary can stretch inherited retirement account distributions over their lifetime instead of the standard 10-year rule, but only if the SNT is drafted properly as a see-through trust. Regulations finalized in 2024 clarified that life-expectancy payouts are available to any EDB of an accumulation trust, not just conduit trusts, which is a major win for special needs planning because conduit distributions can jeopardize public benefits. SECURE Act 2.0 also confirmed that a special needs trust may name a qualifying charitable organization as remainder beneficiary without triggering the truncated 10-year payout period. Broader estate planning strategies with life insurance can help coordinate these moving pieces.

Working With Special Needs Attorneys & Common Mistakes to Avoid

Why a Special Needs Attorney Is Essential

Special needs planning sits at the intersection of estate law, tax law, disability benefits, and insurance. A general estate attorney may not have the expertise to draft a compliant SNT. Look for an attorney who:

- Is a member of the Special Needs Alliance or Academy of Special Needs Planners

- Has experience with Medicaid and SSI benefit rules in your state

- Works alongside a financial planner familiar with disability planning

- Can coordinate the SNT with your will, guardianship documents, and beneficiary designations

Most Common Mistakes to Avoid

A particularly overlooked mistake in 2026: even if your own beneficiary designations are perfect, Grandma's old policy may still name your child directly. Proactively inform relatives that any life insurance or inheritance for your child should name the SNT, not the child.

Also avoid general life insurance mistakes that affect all families, like letting a policy lapse or forgetting to name a contingent beneficiary. For single parents raising a special needs child, life insurance for single parents provides additional coverage guidance specific to your situation.

Frequently Asked Questions

Can a special needs trust be the owner of a life insurance policy?

Yes, a special needs trust can own a life insurance policy, though this is a more advanced planning strategy. When the trust owns the policy, it keeps the death benefit out of the parent's taxable estate, which can be beneficial for larger estates. This approach requires careful coordination with an estate planning and special needs attorney to ensure the trust document grants the trustee proper authority to purchase and manage insurance policies.

What happens if I name my special needs child directly as a life insurance beneficiary?

If you name your child directly and they are receiving SSI or Medicaid, the death benefit could immediately push their assets above the program's $2,000 resource limit. This would disqualify them from benefits until the funds are spent down, usually through an expensive first-party trust setup or court proceedings that also trigger Medicaid payback at death. Always name the third-party SNT as beneficiary, not the child personally.

How do ABLE accounts work alongside a special needs trust in 2026?

ABLE accounts and SNTs work best together, not as competitors. In 2026, ABLE accounts allow up to $20,000 in annual contributions with tax-free growth, and the eligibility age of onset expanded from 26 to 46. Up to $100,000 is excluded from SSI resource limits, so the SNT can hold larger sums from life insurance while the ABLE account gives the beneficiary more day-to-day control over disability-related expenses without endangering benefits.

Do life insurance proceeds paid to an SNT affect the child's SSI or Medicaid?

No. When life insurance proceeds are paid to a properly structured third-party SNT (not the child directly), they are not counted as the child's assets and do not affect SSI or Medicaid eligibility. The trust holds and manages the funds, and distributions for supplemental needs generally do not count as income. Proper SNT drafting and trustee administration are critical to maintaining this protection.

How often should I review my life insurance coverage and SNT beneficiary designations?

You should review both your life insurance coverage and SNT beneficiary designations at least every three to five years, and immediately after major life events like divorce, a new child, a change in your child's diagnosis or care needs, policy changes, or trust amendments. Beneficiary designations override your will, so an outdated form can send funds to the wrong place entirely. Annual check-ins with your special needs attorney and financial planner are strongly recommended.