Compare Car Insurance Rates in Ohio

See if you qualify for a lower rate in less than 2 minutes

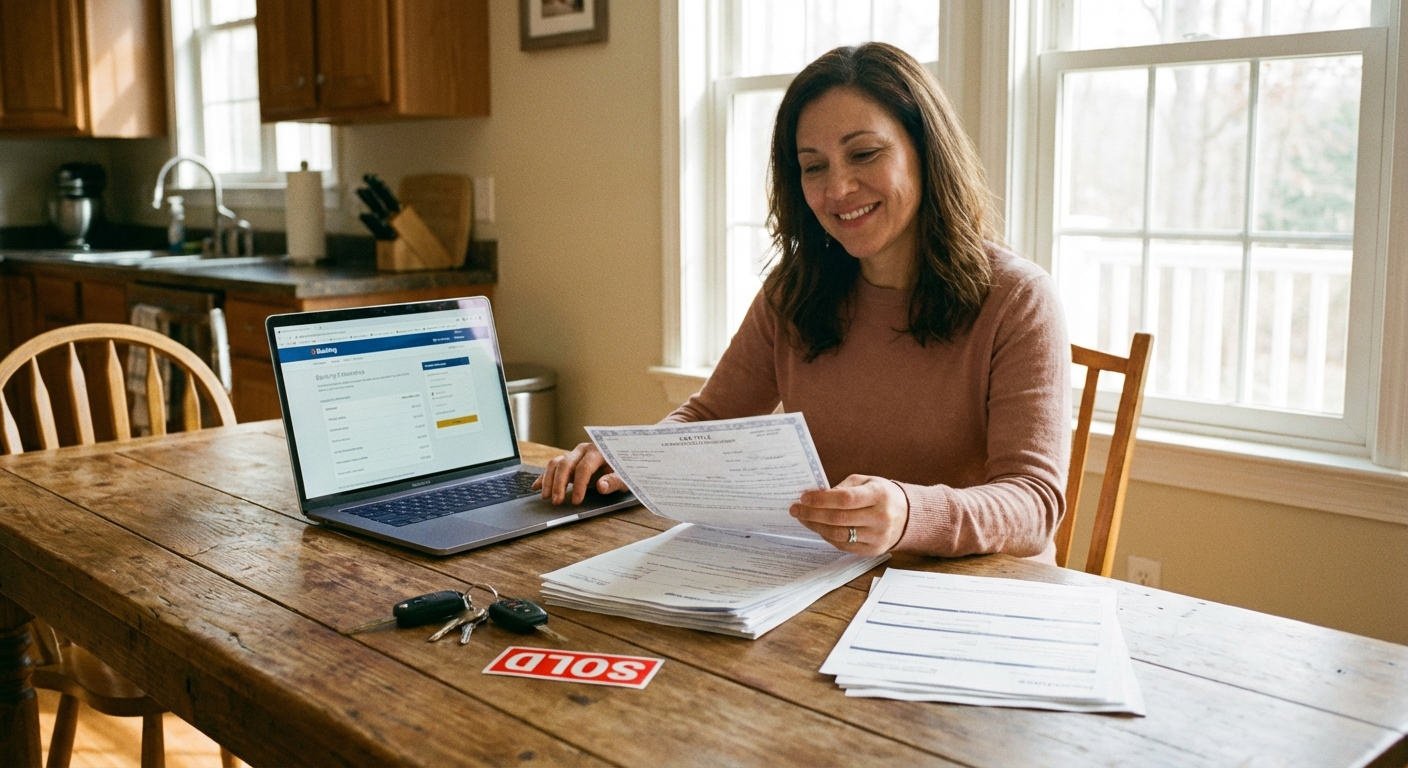

When Should You Remove a Car From Your Insurance Policy?

Knowing the right moment to remove a vehicle is just as important as knowing how. Remove it too early and you could be liable for an uninsured vehicle you still technically own. Remove it too late and you're burning money on coverage you don't need.

Common Reasons to Remove a Vehicle

| Reason | Best Timing for Removal |

|---|---|

| Sold the car | After title is signed over and bill of sale is complete |

| Car was totaled | After total loss settlement is finalized and title is transferred |

| No longer driving it | After surrendering plates or transferring registration |

| Moving to another state | After new-state policy is active and old plates are returned |

| Switching insurers | Exactly on the start date of your new policy |

The #1 Mistake to Avoid

Never cancel or remove a vehicle from your policy before the ownership or DMV steps are complete. If a car is still registered in your name and an incident occurs, you could face legal and financial liability — without any coverage to back you up.

If you're simply storing a vehicle you still own rather than selling it, you may want to explore options for car insurance when selling your car as a cost-saving alternative to full removal.

Compare Car Insurance Rates in Ohio

See if you qualify for a lower rate in less than 2 minutes

How to Remove a Car From Your Insurance Policy: Step-by-Step

Removing a vehicle is processed as a policy endorsement — a mid-term change — not a full cancellation. Your other vehicles stay covered throughout the process.

Step 1: Gather Your Documents

Before contacting your insurer, collect:

- Your current policy declarations page

- Bill of sale or signed title (if sold)

- Total loss claim number and settlement confirmation (if totaled)

- DMV plate surrender receipt (if applicable in your state)

- Your driver's license and VIN of the vehicle being removed

Step 2: Choose Your Removal Date

Be deliberate about the effective date:

- If sold: Set it for the day after the title is officially signed over

- If totaled: Set it for the date the settlement was finalized and title transferred to the insurer

- If switching insurers: Match it exactly to your new policy's start date — not a day before

Step 3: Contact Your Insurance Company

You can reach out through multiple channels. In 2025–2026, most major insurers now allow full self-service vehicle removal via their mobile app or online portal — including the ability to upload proof of sale and see your updated premium instantly with real-time recalculation.

When you call or submit online, record the date, time, and name of the representative you spoke with.

Step 4: Confirm the Change in Writing

Always request written confirmation that the vehicle has been removed — most insurers now provide this instantly via email or your online account dashboard. This document should clearly show:

- The vehicle's year, make, model, and VIN

- The exact effective date coverage ended

- Your updated policy premium going forward

Keep this on file — you may need it for the DMV, a lender, or to prove continuous coverage history.

Step 5: Handle State DMV Requirements

State rules vary widely. A significant number of states — including New York, New Jersey, Florida, Maryland, Pennsylvania, North Carolina, and others — require you to surrender your license plates before or simultaneously with dropping coverage on a vehicle. Keeping your plates active without insurance can result in fines, registration suspension, or even a driver's license suspension.

For a deeper look at how the car insurance cancellation process works — including state-specific rules — check out our full step-by-step cancellation guide.

Protect your car with Farmers

Average Rate:

Find coverage options that fit your budget.

The insurance savings you expect.

Average Rate:

Enjoy personalized policies, comprehensive coverage & more.

See how much you could save today!

Average Rate:

Drivers who switch their auto insurance and save with State Farm save $764 on average!

Safe Drivers Save with Allstate®

Average Rate:

Get rewarded with savings for having a clean driving record.

Getting a Prorated Refund When Removing a Car

One of the most overlooked benefits of removing a vehicle mid-policy is the refund you may be owed. If you've paid your premium in advance, your insurer will recalculate the total premium without that vehicle and return the difference.

How the Refund Is Calculated

Most insurers use one of two methods:

| Method | How It Works | What You Get |

|---|---|---|

| Pro-Rata | Full unused premium refunded, no penalty | 100% of unearned premium (minus fees) |

| Short-Rate | Insurer keeps a small percentage as a penalty | ~85–90% of unearned premium |

Pro-rata is the most common method for mid-term vehicle removals where you keep the policy active. Short-rate penalties — typically 10–15% of unearned premium — are more commonly applied when you fully cancel a policy on your own initiative. Learn more about how short-rate vs. pro-rata cancellations affect your final refund amount.

Example (Pro-Rata):

- Car 2 accounts for $800/year of your annual premium

- You remove it exactly 6 months into the policy

- Refund ≈ $800 × (6 remaining months ÷ 12) = $400 back

Fees That May Be Deducted

- Admin or processing fees: Typically $10–$50 for a mid-term vehicle change, though many insurers waive this for simple removals

- Short-rate penalty: Around 10–15% of unearned premium, more commonly applied on full cancellations

- No refund if paying monthly: If you pay monthly, you've only prepaid for the current month — the savings simply appear as a lower bill going forward

Refund Processing Timelines

Most insurers process refunds within 10 to 30 business days after the vehicle is officially removed — often closer to 2–3 weeks in practice. Payment method matters too: direct deposit or card credits usually appear within 1–2 weeks, while paper checks can take 3–4 weeks total including mail time. If you pay monthly, the credit typically appears on your next billing cycle.

Many states' regulations require "prompt" return of unearned premium, and some even mandate interest on late refunds if the insurer misses the deadline. If you haven't received your refund after 30 days, contact your state's Department of Insurance.

Always ask your insurer directly: "Do you use pro-rata or short-rate for mid-term vehicle changes, and are there any processing fees?"

Learn more about how car insurance mid-term cancellation fees work to understand all the scenarios that impact your payout.

Important Situations & Potential Issues

Removing One Car While Keeping the Policy Active

You can absolutely remove a single vehicle and keep your policy running for the remaining cars. The insurer processes it as an endorsement and recalculates your premium. Your coverage on all other listed vehicles continues without interruption.

If you're replacing the removed vehicle with a new one, check out our guide on adding a car to your insurance policy to understand grace periods and coverage deadlines.

State Minimum Liability Limits Updated in 2025

If you remove one car and keep another, be aware that several states raised their minimum auto liability requirements in 2025. Your remaining vehicles must meet these updated minimums:

| State | Old Minimum | New Minimum (2025) |

|---|---|---|

| California | 15/30/5 | 30/60/15 (eff. Jan 1, 2025) |

| Utah | 25/65/15 | 30/65/25 (eff. Jan 1, 2025) |

| Virginia | 30/60/20 | 50/100/25 (eff. Jan 1, 2025) |

| North Carolina | 30/60/25 | 50/100/50 (eff. July 1, 2025) |

It's a good time to do a full car insurance policy review after removing a vehicle — you may find additional coverage gaps or savings opportunities while you're at it.

Removing a Totaled Vehicle

Once your insurer declares a total loss, accepts the claim, and you sign over the title, the vehicle should be removed from your policy promptly. However:

- Don't remove it before the settlement is finalized — you need coverage in force through the end of the claims process

- If you retain the salvage, you'll need to discuss separate coverage options with your insurer, as standard full coverage typically won't continue on a salvage-titled vehicle

- Liability coverage tied to the original accident date remains in effect for any claims from that incident, even after the car is removed

For more guidance on how selling or losing a vehicle affects your coverage, see our article on car insurance when selling your car.

Maintaining Continuous Coverage History

Even if you're removing your only vehicle and won't drive for a while, a coverage lapse can cost you significantly. Industry data shows that a lapse of up to 30 days can raise your future premiums by 8–20%, while gaps of 1–3 months commonly trigger increases of 20–35% or more. Lapses beyond 3 months may push you into the non-standard/high-risk market, with surcharges of 35%+.

One notable exception: starting January 1, 2026, Louisiana's Act 476 enacted a rule stating that a first coverage lapse alone cannot be the sole trigger for a rate increase — and if you've had 5+ years of continuous coverage, a new lapse is treated as your "first." Outside of Louisiana, most states still allow surcharges for any gap.

If you plan to drive again within 6–12 months, consider a non-owner car insurance policy to keep your continuous coverage history intact. Our guide on how to switch car insurance companies covers how continuous coverage history carries over when you return to the market.

Removing a Car When You Have Umbrella Insurance

This is critical and often overlooked. Most personal umbrella policies require that all owned vehicles maintain minimum underlying liability limits — typically $250,000–$500,000 per person in bodily injury. In 2025–2026, insurers have become stricter about requiring that all household vehicles and drivers be disclosed and appropriately insured before issuing or renewing an umbrella policy.

If you remove a car from your auto policy but still own and drive it, your umbrella insurer may deny coverage for any auto-related claims involving that vehicle — or even argue you've breached policy conditions more broadly.

Before removing any vehicle, ask your umbrella insurer:

- Does removing this vehicle affect my umbrella coverage?

- What minimum liability limits must remain on my other vehicles?

- Do all owned vehicles need to be listed on an underlying auto policy?

If you're selling the car outright and won't own it anymore, the umbrella policy generally continues unaffected — as long as your remaining vehicles still meet the required minimum liability limits.

Considering whether to adjust your overall coverage after a vehicle change? Our guide on car insurance for financed vs. paid-off vehicles can help you decide what coverage you really need going forward.

Frequently Asked Questions

Can I remove a car from my insurance policy online?

Most major insurers now allow you to remove a vehicle through their mobile app or online account portal — including uploading your bill of sale and seeing your updated premium instantly with real-time recalculation. However, some still require a phone call or written request, especially for complex mid-term changes. Always follow up by downloading or screenshotting the updated declarations page as written confirmation of the change.

Will removing a car from my policy cancel the entire policy?

No — removing one vehicle is processed as a policy endorsement, not a full cancellation. Your policy stays active and your remaining vehicles continue to be covered without interruption. The only exception is if the car you're removing is the only vehicle on the policy, in which case the policy will effectively end unless you add another vehicle or convert it to a non-owner policy.

How long does it take to get a refund after removing a car?

Most insurers process prorated refunds within 10 to 30 days of the effective removal date — often closer to 2–3 weeks. Direct deposit or card credits typically appear within 1–2 weeks after processing, while paper checks can take 3–4 weeks total. If you pay monthly, the adjustment usually appears as a lower next bill rather than a separate refund payment.

Do I need to notify my lienholder when removing a car from my policy?

If the vehicle being removed has an active loan or lease, yes — you likely need to notify the lender. Most finance agreements require you to maintain full coverage (collision and comprehensive) for the life of the loan. Removing coverage without notifying the lender can put you in breach of your loan agreement and may trigger "force-placed" insurance, which is far more expensive than standard coverage. See our guide on car insurance for financed vs. paid-off vehicles for more details.

What happens if I remove a car from my policy but forget to return the license plates?

In many states — including New York, New Jersey, Florida, Maryland, Pennsylvania, North Carolina, and others — if your vehicle's plates remain active but the car is uninsured, the state DMV may flag the vehicle and issue fines, suspend your registration, or suspend your driver's license. Always check your state's specific plate surrender requirements and complete them in the correct sequence relative to your policy change. Keep your plate surrender receipt as proof.