Compare Car Insurance Rates in Ohio

See if you qualify for a lower rate in less than 2 minutes

What Is Car Insurance Price Optimization?

Car insurance price optimization is a data-driven pricing strategy used by insurers to maximize revenue — not by accurately reflecting your risk, but by calculating the highest premium you'll accept before shopping elsewhere. Rather than basing your rate purely on actuarial data like your driving record or claims history, insurers layer in customer demand models to identify your "price elasticity."

In plain terms: How much can we raise this person's rate before they leave?

The Casualty Actuarial Society defines it as the supplementation of traditional supply-side actuarial models with quantitative customer demand models — feeding algorithms data about your tenure, payment history, shopping behavior, demographics, and even competitor pricing. The output is a personalized premium engineered to extract as much profit as possible from customers deemed unlikely to comparison shop.

| Pricing Factor | Traditional (Risk-Based) | Price Optimized |

|---|---|---|

| Driving record | ✅ Used | ✅ Used |

| Vehicle type | ✅ Used | ✅ Used |

| Claims history | ✅ Used | ✅ Used |

| Years with insurer | ❌ Not relevant | ✅ Used to raise rates |

| Shopping frequency | ❌ Not relevant | ✅ Used to raise rates |

| Payment habits | ❌ Not relevant | ✅ Used to raise rates |

Compare Car Insurance Rates in Ohio

See if you qualify for a lower rate in less than 2 minutes

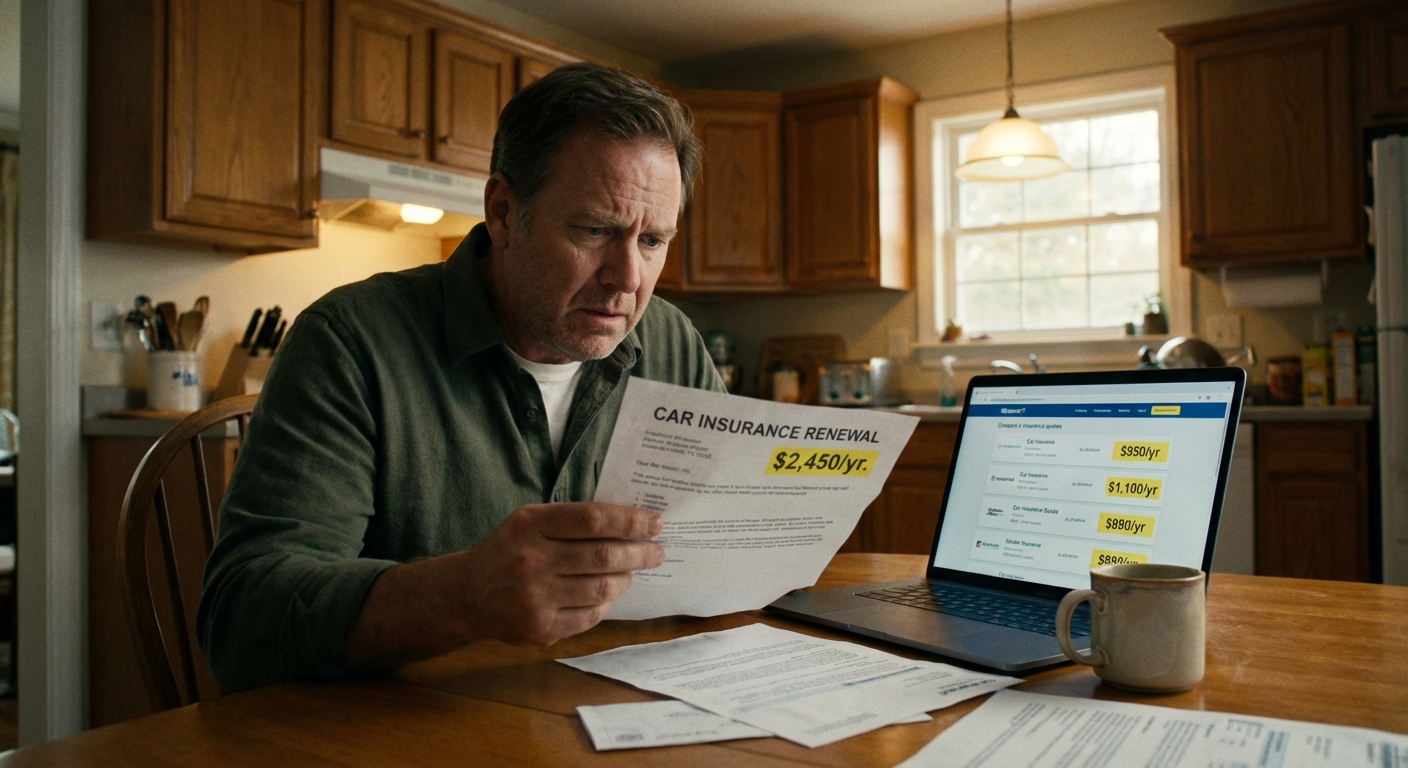

The Loyalty Penalty: How Staying Loyal Costs You Money

The insurance loyalty penalty is the direct financial consequence of price optimization. While insurers market loyalty discounts and long-term customer perks, the reality is that long-term policyholders are quietly charged more than new customers for identical coverage.

Here's how the cycle works: insurers offer attractive introductory rates to win new business, then implement gradual renewal rate creep year after year. Each small increase — often 5% to 8% — feels inconsequential on its own, but compounds significantly over time. The algorithm knows that most customers won't bother switching over a $15/month bump.

How Much More Are Loyal Customers Paying?

Drivers who don't compare quotes every 2–3 years could pay 15% to 25% more than necessary. The financial damage grows sharply with tenure:

| Years with Same Carrier | Auto Insurance Overpayment | Home Insurance Overpayment | Combined Annual Loss |

|---|---|---|---|

| 1–3 years | $287/year | $156/year | $443/year |

| 4–6 years | $624/year | $389/year | $1,013/year |

| 7–10 years | $1,043/year | $712/year | $1,755/year |

| 10+ years | $1,456/year | $1,124/year | $2,580/year |

Loyalty to your insurance company can cost $1,200 or more per year — and in some cases, households with both auto and home policies who've never switched can overpay by $2,500+ annually.

Explore how the insurance loyalty penalty plays out in detail, including what switching savings actually look like with current 2026 rate data.

Protect your car with Farmers

Average Rate:

Find coverage options that fit your budget.

The insurance savings you expect.

Average Rate:

Enjoy personalized policies, comprehensive coverage & more.

See how much you could save today!

Average Rate:

Drivers who switch their auto insurance and save with State Farm save $764 on average!

Safe Drivers Save with Allstate®

Average Rate:

Get rewarded with savings for having a clean driving record.

States That Ban Price Optimization — and How Regulators Are Fighting Back

Because price optimization charges customers different rates for the same risk profile, many state regulators have classified it as unfair discrimination — illegal under existing insurance statutes that require similar risks to receive similar rates.

States That Have Banned or Restricted Price Optimization

At least 16 states and the District of Columbia have formally prohibited the practice:

Consumer Advocacy Driving Change

Several major organizations have been leading the charge against price optimization:

- Consumer Federation of America (CFA) — Has sent formal letters to the Federal Trade Commission opposing price optimization and calls on state insurance departments to end its use, citing disproportionate harm to low-income consumers.

- United Policyholders — Testified before regulators and petitioned the NAIC for national oversight of the practice.

- Consumer Watchdog — Conducted two major investigations in California, confirming price optimization violates Proposition 103.

- Consumer Reports — Called on state insurance commissioners nationwide to investigate whether consumers are being unfairly overcharged.

Consumer complaints about insurers rose 7% in 2025 compared to 2024, reflecting growing frustration with opaque pricing practices. Despite advocacy efforts, the remaining 34 states still lack explicit bans — meaning millions of drivers in those states may be subject to price optimization with no regulatory protection.

How to Identify and Escape the Loyalty Tax

Warning Signs You're Being Price Optimized

Understanding the car insurance loyalty penalty vs. new customer rates starts with knowing the red flags:

- Your premiums increase at every renewal without any claims, tickets, or major life changes

- Your insurer offers a "loyalty discount" of 5–10%, but new customer promotions offer 20–40% off

- You've been with the same carrier for 5+ years and never compared quotes

- When you threaten to cancel, your insurer suddenly offers a substantial rate reduction

- You have excellent credit and a clean driving record, yet your rate keeps climbing

Strategies to Stop Overpaying

1. Shop Every 6 to 12 Months Experts recommend comparing quotes before every renewal — or at minimum, once a year. Some experts suggest shopping in December, when many carriers are setting rates for the new year. Getting quotes from at least 3 competing insurers is the single most effective way to combat price optimization.

2. Switch Carriers When It Makes Sense Median annual savings from switching insurers range from $461 to $804 per year. You can switch at any time — you don't need to wait for your policy to expire. Your old insurer is required to refund any unused premium.

3. Use Competing Quotes as Leverage Even if you prefer to stay with your current insurer, a competing quote gives you negotiating power. Call your insurer, mention the competitor's rate, and ask them to match it. If they can't — or won't — that's your signal to switch.

4. Review Your Coverage Annually Life changes affect your rate. Moving, paying off a car loan, improving your credit score, or completing a defensive driving course can all reduce your premium. Make sure your insurer has your most current information.

5. File a Complaint if You Suspect Foul Play In states with bans, contact your state insurance department if you suspect price optimization is inflating your rates. You have the right to request an explanation of any rate increase.

Frequently Asked Questions

What exactly is car insurance price optimization?

Car insurance price optimization is the practice of using algorithms and behavioral data — such as how long you've been a customer, your shopping history, and payment habits — to determine the highest premium you'll accept without switching insurers. It goes beyond traditional risk-based pricing by incorporating customer demand models. The goal is to maximize profit per customer, not to accurately reflect your actual risk as a driver.

Is insurance price optimization legal?

It depends on your state. At least 16 states and the District of Columbia have formally banned the practice, classifying it as unfair discrimination because it charges customers different rates for the same risk profile. However, the remaining 34 states do not have explicit bans, meaning insurers in those states may legally use price optimization in their rate filings. Check with your state insurance department to understand the rules where you live.

How do I know if I'm being charged a loyalty penalty?

Key warning signs include annual premium increases without any claims or changes to your driving record, minimal loyalty discounts compared to the new-customer offers advertised, and a sudden willingness from your insurer to drop your rate when you threaten to leave. The best way to confirm it is to get competing quotes — if multiple competitors are offering the same coverage for significantly less, you're likely paying the loyalty penalty.

How much money can I save by switching car insurance carriers?

Savings vary by driver profile, location, and coverage level, but median annual savings from switching carriers range from $461 to $804 per year. Drivers who haven't compared rates in 2–3 or more years could be overpaying by 15% to 25%. Long-term policyholders with both auto and home insurance who've never switched can overpay by $2,500 or more annually when both policies are factored in.

How often should I shop for car insurance?

Most experts recommend shopping for car insurance every 6 to 12 months, ideally before your policy renewal date. At a minimum, compare quotes once per year — or whenever you experience a major life change such as moving, buying a new car, getting married, or improving your credit score. Annual shopping is the most reliable defense against renewal rate creep and the loyalty penalty.