Compare Car Insurance Rates in Ohio

See if you qualify for a lower rate in less than 2 minutes

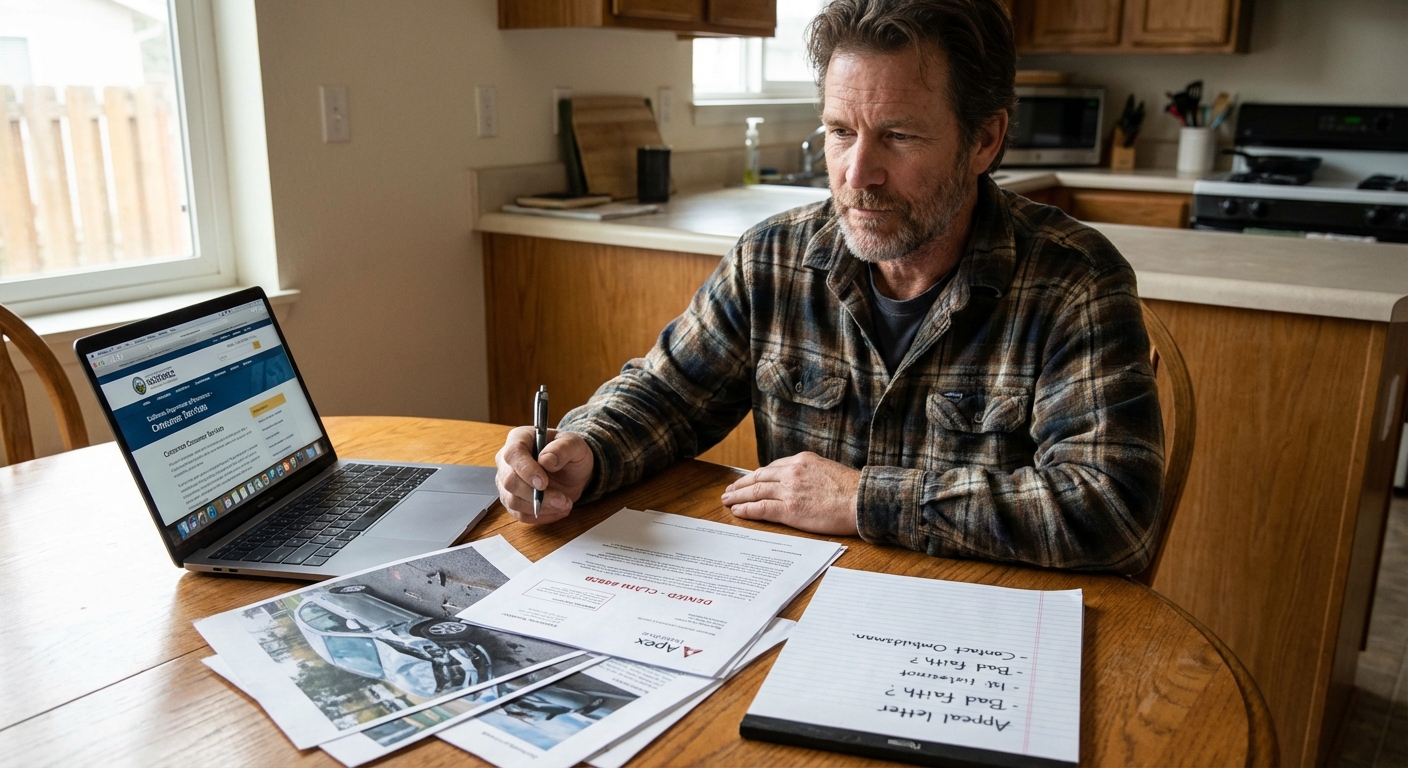

The Internal Appeals Process: Your First Line of Defense

When your insurer denies a claim or offers a settlement that feels unfair, your first move is always to work within the company's own system before escalating elsewhere. Most insurance carriers maintain a formal internal appeal process, and using it correctly can resolve many disputes without ever involving outside parties.

Step 1: Review the Denial Letter Carefully

Your denial letter is your roadmap. It must state the exact reason for denial, whether it's a policy exclusion, missing documentation, or a coverage dispute. Note the appeal deadline listed in the letter, which is typically 30 to 60 days for auto insurance policies. Under existing standards for prompt, fair, and equitable settlements, insurers are expected to resolve claims within 30 days, so hold them to that timeline. In states with 2025–2026 AI transparency rules (Illinois, Michigan, Florida), you can also formally request clarification if the decision relied on artificial intelligence models.

Step 2: Build Your Case

Gather every piece of supporting evidence you can find:

- Your full insurance policy with relevant sections highlighted

- Photos of vehicle damage, the accident scene, or injuries

- Police or accident reports

- Repair estimates from at least two licensed shops

- Witness statements or contact information

- All prior communications with your adjuster

Step 3: Submit a Formal Written Appeal

Write a clear appeal letter addressed to the insurer's appeals department (check your denial notice for the address). Your letter should:

- Reference your policy number, claim number, and date of denial

- Quote the exact denial reason and explain why it is incorrect

- Cite the specific policy language that supports your position

- List all attached supporting documents

Step 4: Escalate to a Supervisor or Claims Manager

If the initial adjuster doesn't budge, explicitly request a second-level internal review by a supervisor or claims manager. This is a standard option at most insurers and brings fresh eyes to your claim. Internal review timelines typically run 30 to 90 days, so follow up proactively to keep your appeal moving. Learn more about what a car insurance claim adjuster does and how each type of adjuster operates within the process.

Compare Car Insurance Rates in Ohio

See if you qualify for a lower rate in less than 2 minutes

Escalating Outside the Company: Regulators & Dispute Tools

If internal appeals fail, several powerful external options can pressure your insurer into a fair resolution.

File a Complaint With Your State Insurance Department

Every state has a Department of Insurance (DOI) or Insurance Commissioner that regulates insurer conduct. Filing a formal complaint is free, requires no attorney, and puts your insurer on record with a government regulator. State insurance departments recovered significant sums for consumers. Missouri alone recovered $46.2 million in 2025 through its Consumer Affairs Division (a record, nearly double the $22 million recovered in 2024), and Pennsylvania returned $16.4 million across more than 15,500 complaints. Nationally, auto insurance complaints to state commissioners rose 7.5% in the year leading up to March 2026, coinciding with the widespread adoption of AI-driven claims evaluation tools. Michigan regulators also strengthened their oversight in 2025 via DIFS Bulletin 2025-25-INS, which replaced prior guidance to curb delay tactics, misrepresentations, and failure to pay undisputed claims promptly, with potential fines or license revocation for violations.

How to file:

- Visit your state DOI website or the NAIC consumer page to locate your state's portal

- Gather policy documents, denial letters, photos, and all correspondence

- Submit online, by mail, or by phone (most states accept all three methods)

- You'll typically receive an acknowledgment within 2 weeks, and your insurer must respond within 25 to 30 days depending on your state

| State Example | Insurer Response Deadline | Notes |

|---|---|---|

| California | Varies | Complaint required before access to state's Automobile Claims Mediation Program |

| Ohio | ~30 days | Analyst assigned; full investigation may take longer |

| Texas | 25 days | Insurer must respond to DOI; written reasons required when declining or canceling policies (eff. Jan. 1, 2026) |

| Louisiana | 30 days | Cancellation/non-renewal notice period doubled to 60 days eff. July 1, 2026 |

| Michigan | ~30 days | DIFS Bulletin 2025-25-INS strengthened oversight; penalties include fines or license revocation |

Invoke the Appraisal Clause for Value Disputes

If you and your insurer agree a claim is covered but disagree on the dollar amount, the appraisal clause in your policy is one of the most effective tools available. Be aware that a growing trend shows insurers using employee adjusters as appraisers and rejecting most consumer-proposed umpires, creating deliberate delays. Know your rights before invoking it. Learn more about how the appraisal clause works in detail, including Texas SB 458 (effective September 1, 2025, applying to policies issued or renewed January 1, 2026 onward, with TDI Docket 2862 rulemaking completed in June 2026) and Washington SB 5721 updates.

Here's how it works:

| Step | What Happens |

|---|---|

| 1. Written Demand | Either party sends a written request to invoke the appraisal clause. Under Texas SB 458 rules, auto claims require demand within 120 days |

| 2. Each Side Hires an Appraiser | You hire one; the insurer hires one. Each party typically pays their own appraiser |

| 3. Appraisers Negotiate | Both appraisers assess the loss and attempt to agree on a value. Texas rules give appraisers 75 days to agree |

| 4. Umpire (If Needed) | If appraisers disagree, a neutral umpire is selected. Costs are typically split, and any two of the three must agree for a binding outcome |

Note: The appraisal clause only resolves disputes about the amount of loss, not whether your claim is covered. Experts generally recommend invoking it only when the dollar gap is significant, since appraiser fees ($300 to $900 each in 2026) and umpire costs can eat into smaller disputes.

Mediation vs. Arbitration: Know the Difference

For disputes that go beyond dollar amounts, car insurance arbitration and mediation offer two distinct paths. The American Arbitration Association (AAA) updated its Consumer Arbitration Rules effective May 1, 2025, and those rules govern most consumer auto insurance disputes that reach AAA. Virtual hearings are now the default, documents-only proceedings apply to cases at or below $25,000 (unless the arbitrator or both parties agree otherwise), integrated mediation procedures (launched April 1, 2025) are built in as a streamlined pre-arbitration option with no separate filing fee, and claims from the same party under a single contract can now be consolidated. Arbitrators also received expanded discovery authority under new Rule 20, expanded sanctions power under Rule 57, and the ability to administer appellate arbitration to a three-arbitrator panel where policies allow it.

Several states also run their own structured programs. California's Automobile Claims Mediation Program handles first-party physical damage disputes where the total claim exceeds $7,500 and the amount in dispute exceeds $2,000, with mediation available only after you file a formal complaint with the CDI first.

Mediation brings in a neutral third-party mediator who facilitates negotiation but has no authority to force a resolution. It's faster and cheaper than court, and you retain all legal rights if it fails. In 2025, AAA mediation filings represented $2.4 billion in disputes and settled in a median of just 112 days.

Arbitration is more like a private court. A neutral arbitrator hears both sides and issues a binding decision. Many auto insurance policies include mandatory arbitration clauses, particularly for uninsured/underinsured motorist (UM/UIM) disputes. Check your policy carefully before assuming you can go straight to court. For a deeper look at how this process works, review our guide on car insurance arbitration.

Protect your car with Farmers

Average Rate:

Find coverage options that fit your budget.

The insurance savings you expect.

Average Rate:

Enjoy personalized policies, comprehensive coverage & more.

See how much you could save today!

Average Rate:

Drivers who switch their auto insurance and save with State Farm save $764 on average!

Safe Drivers Save with Allstate®

Average Rate:

Get rewarded with savings for having a clean driving record.

When to Bring In Professional Help

Sometimes a dispute becomes complex enough that you need expert firepower on your side. Two professionals, public adjusters and attorneys, serve very different roles. Recent 2026 case law shows courts remain willing to hold insurers accountable. In California, the Court of Appeal's May 2026 Bornoff v. State Farm decision revived a bad-faith claim based purely on allegedly unreasonable claims-handling delay, and a 2026 North Carolina court upheld $116 million in bad faith liability against a captive insurer that allegedly stalled a claim for over a year to protect its parent company's acquisition prospects. Learn more about the full fight-back process in our guide on how to fight a denied insurance claim.

Public Adjuster vs. Attorney: Who Do You Need?

| Public Adjuster | Attorney | |

|---|---|---|

| Best For | Undervalued or delayed claims | Denied claims, bad faith, litigation |

| What They Do | Documents damage, negotiates with insurer | Provides legal advice, files lawsuits |

| Fees | 5 to 20% of settlement (state caps apply) | 33 to 40% of settlement |

| Can Sue? | No | Yes |

| Ideal Stage | During active negotiation | After all other options fail |

2026 Public Adjuster Fee Update: State caps vary widely. Florida allows up to 20% for standard claims and 10% for state-of-emergency claims (with a 1% cap when insurers pay policy limits within 14 days of loss). Georgia caps at 33.3%. Tennessee caps at 15% before any payment and 25% of new money afterward. Iowa caps disaster claims at 10%. Louisiana caps commercial claims at 10%. Pennsylvania's HB 1972 (passed the House in February 2026) would set a 10% catastrophe cap and 18% cap for regular claims. California currently has no statutory cap, but proposed AB 597 would set 15% on "new money" for disaster claims. Always verify your state's rules before signing any public adjuster contract.

The general rule: start with a public adjuster if your claim is disputed on value and coverage is not in question. Escalate to an attorney if the insurer is acting in bad faith, your claim was outright denied, or negotiations have completely stalled. For disputes over car insurance settlements, represented claimants consistently recover significantly more than those who go it alone. Federal appellate courts, however, continue to demand a clear causal link between insurer misconduct and damages, so documentation is critical.

Time Limits, Documentation, and State Deadlines

One of the most common (and costly) mistakes in insurance disputes is waiting too long. Deadlines operate at multiple levels simultaneously.

Document Everything From Day One

Strong documentation is the backbone of any successful dispute. Follow this checklist from the moment an incident occurs:

- 📸 Photos & video of all vehicle damage, the scene, and any injuries

- 📋 Police reports and accident exchange information

- 🧾 Repair estimates from at least two licensed shops

- 📞 Call logs with dates, times, and names of every person you speak with

- 📬 Certified mail for all formal letters and appeals

- 🗂️ Copies of everything submitted to your insurer

If your dispute involves a total loss, make sure you understand how insurers assess damage and what comparable vehicles are selling for in your market. This data is critical for total loss negotiation, especially with total loss frequency hitting a record 23.1% of all auto claims in 2025.

Key Time Limits to Know

Deadlines exist at multiple stages of the dispute process. Missing any one of them can permanently eliminate your right to recover. For a complete state-by-state breakdown, see our statute of limitations guide. Statutes of limitations for car insurance claims typically range from 1 to 6 years for personal injury and 1 to 10 years for property damage, depending on state.

| Deadline Type | Typical Timeframe | Notes |

|---|---|---|

| Report claim to insurer | Immediately to 30 days | Varies by state and policy |

| Internal appeal filing | 30 to 60 days from denial | Always check your denial letter |

| State DOI complaint | Varies by state (often 1 to 4 months) | Check your state DOI website |

| Statute of limitations (personal injury) | 1 to 6 years by state | Starts from accident date |

| Statute of limitations (property damage) | 1 to 10 years by state | Starts from accident date |

Notable state limits for personal injury lawsuits:

- 1 year: Kentucky, Tennessee

- 2 years: Most states, including CA, TX, FL (for accidents after March 24, 2023), PA, AZ, AL, CT, DE, GA, HI, ID, IN, IA, KS, LA (eff. July 1, 2024), NV, OK, WV

- 3+ years: AR, CO, MD, MA, MI, MO (5 yrs), ME (6 yrs), ND (6 yrs), MN (6 yrs)

Notable state limits for property damage lawsuits:

- 1 year: Louisiana

- 2 years: Alabama, Alaska, Arizona, Texas, Pennsylvania, Connecticut, Kansas, Indiana, Montana, Oklahoma, West Virginia, Florida (HB 837)

- 3 to 10 years: California (3 yrs), Illinois (5 yrs), Virginia (5 yrs), Oregon (6 yrs), Wisconsin (6 yrs), MN (6 yrs), RI (10 yrs)

Important state-specific updates: Florida's HB 837 (signed March 24, 2023) reduced the bodily injury statute of limitations from 4 years to 2 years and replaced pure comparative negligence with a modified version (plaintiffs found more than 50% at fault cannot recover). New York's Assembly Bill A10008, effective for actions commenced on or after May 26, 2026, eliminated the "90/180-day" serious-injury category and added modified comparative fault rules with a damages cap. Louisiana extended its personal injury deadline from 1 to 2 years for injuries occurring on or after July 1, 2024. Always verify your state's current limits with a local attorney or your state DOI.

For step-by-step guidance from the start of your claim, review our how to file a car insurance claim guide, or learn what to do if you receive an insurance adverse action notice.

Frequently Asked Questions

What is the first step when my car insurance claim is denied?

Read your denial letter thoroughly to understand the exact reason for the denial and note the appeal deadline, typically 30 to 60 days. Then gather all supporting evidence (photos, police reports, repair estimates) and submit a formal written appeal letter to your insurer's appeals department. Reference your specific policy language and explain clearly why the denial is incorrect. If your initial adjuster won't reconsider, explicitly request a review by a supervisor or claims manager.

Can I take my insurance company to small claims court?

Yes, in most states you can sue your insurer in small claims court without an attorney if the disputed amount falls within your state's limit, which ranges from as low as $2,500 in some states to $25,000 in others. Small claims is best suited for clear-cut disputes like underpaid repairs or unreimbursed rental costs. Filing fees are generally $30 to $100, and hearings are typically scheduled within 30 to 60 days. The AAA's 2025 consumer rules also preserve your right to small claims court even when your policy has an arbitration clause.

What does the appraisal clause do and when should I use it?

The appraisal clause is a built-in policy provision that resolves disagreements about the dollar amount of a loss, not whether a claim is covered. Each side hires an independent appraiser; if they disagree, a neutral umpire casts the deciding vote, with the outcome being binding. It's most effective when the gap between your estimate and the insurer's offer is significant, as appraiser fees ($300 to $900 each in 2026) and umpire costs can outweigh the benefit on smaller disputes. Know your rights under your state's specific laws (like Texas SB 458 with its 120-day auto demand window, or Washington SB 5721 with its OIC umpire registry). See our full guide on the insurance appraisal clause for more detail.

How do I file a complaint with my state insurance department?

Visit your state's Department of Insurance website or go to NAIC.org to find your state's complaint portal. You can typically file online, by mail, or by phone, and most states acknowledge your complaint within two weeks. Your insurer is generally required to respond within 25 to 30 days, and your state regulator will investigate whether the company violated any fair claims handling laws. This step often prompts insurers to reconsider denied or underpaid claims. Missouri's DOI set a record $46.2 million in consumer recoveries in 2025, nearly double the prior year.

When should I hire an insurance attorney instead of a public adjuster?

Hire an attorney when your claim has been outright denied, your insurer is acting in bad faith (unreasonable delays, misrepresentation, or lowball offers), or negotiations have completely failed and you need to pursue legal action. Recent 2026 rulings, including the California Bornoff v. State Farm decision reviving a bad-faith delay claim and a $116 million North Carolina bad-faith verdict, show courts continue to hold insurers accountable. Public adjusters are better suited when coverage is acknowledged but the settlement offer is too low. They handle documentation and negotiation but cannot provide legal advice or file lawsuits. Most insurance attorneys work on contingency (33 to 40% of the recovery), so there's no upfront cost to get started.