Compare Car Insurance Rates in Ohio

See if you qualify for a lower rate in less than 2 minutes

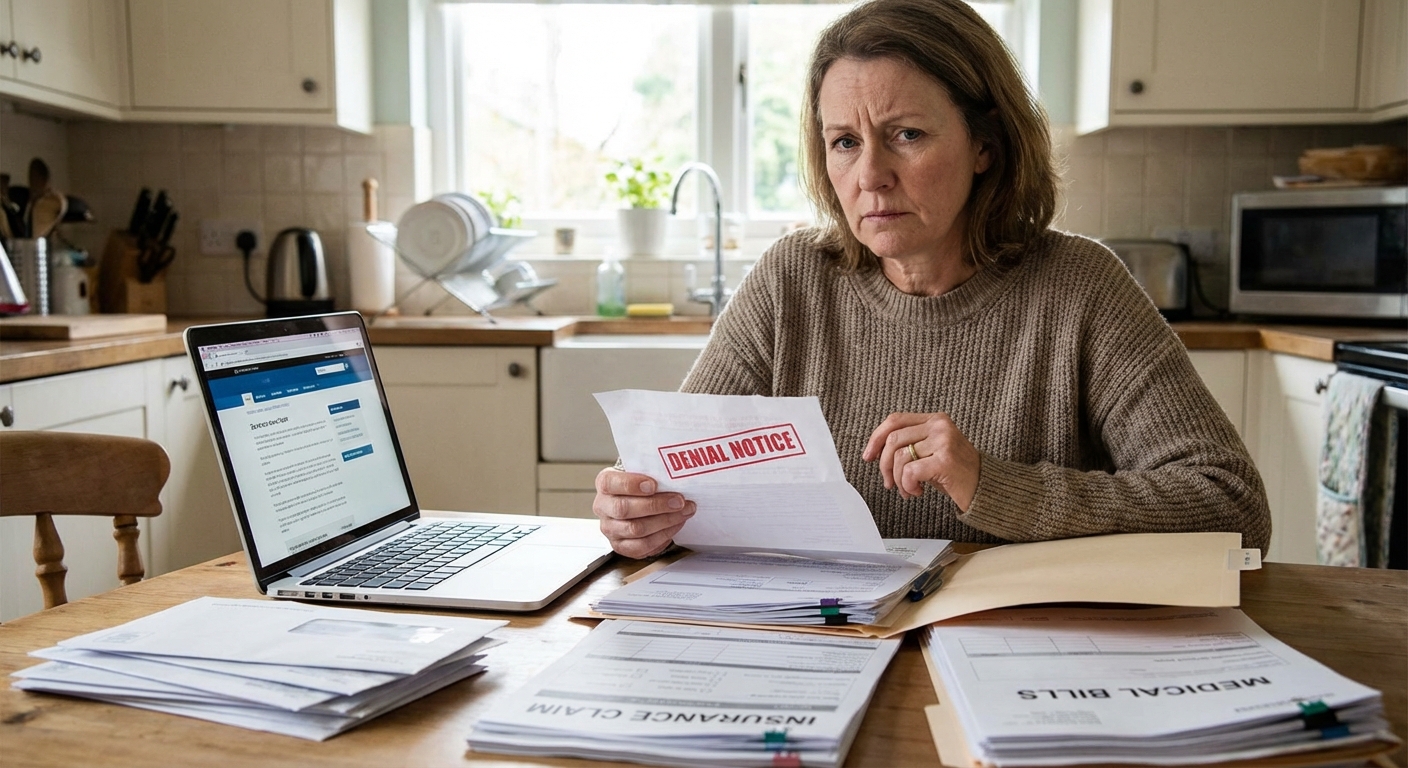

What Constitutes Bad Faith Insurance

Bad faith insurance occurs when an insurance company fails to uphold its duty of good faith and fair dealing to its policyholders. This duty requires insurers to handle claims fairly, promptly, and transparently. When insurers prioritize profits over their obligations, they engage in bad faith practices that can leave policyholders financially vulnerable.

Unreasonable Claim Denial

Insurance companies act in bad faith when they deny valid claims without legitimate justification. Common examples include rejecting claims for covered events, denying coverage based on misrepresented policy terms, or altering policy language after a claim is filed. These denials often happen without proper explanation or investigation.

Insurers may claim damages were pre-existing without evidence, cite vague policy exclusions that don't actually apply, or misclassify losses to avoid payouts. Some companies even cancel policies retroactively to avoid paying claims, which is a clear violation of good faith obligations.

Delayed Payments

Deliberate stalling of claim processing extends beyond reasonable investigation time. Bad faith delays include ignoring claim submissions despite repeated contact, requesting excessive documentation unnecessarily, frequently changing adjusters without explanation, or keeping claims "under review" indefinitely. State law typically requires insurers to adopt reasonable standards for prompt investigation and settlement of claims, and to not refuse to pay claims without conducting a reasonable investigation. Insurers must also promptly provide a reasonable and accurate explanation of the basis for claim denials or compromise settlement offers.

These tactics pressure policyholders into accepting lowball settlements or abandoning valid claims entirely. When you need funds for accident-related repairs or medical bills, delays create financial hardship that insurers exploit to minimize payouts.

Failure to Investigate

Insurers must conduct thorough, timely investigations before making claim decisions. Bad faith occurs when companies deny claims without any investigation, hide evidence supporting liability, ignore relevant documentation or medical recommendations, or employ deceptive tactics such as relying on drive-by inspections or unqualified adjusters.

A major concern in 2026 is the use of AI-driven claim handling. In late 2025 and early 2026, the National Association of Insurance Commissioners and multiple states rolled out new AI governance rules aimed at transparency, fairness, and meaningful human involvement. Regulators now require documented AI governance programs, and courts increasingly treat fully automated denials as evidence of unreasonable claims handling. Every state requires human clinical oversight before an adverse determination is issued in health-related cases, and similar principles are being extended across other lines.

Lowball Settlement Offers

Offering settlements significantly below the claim's actual value constitutes bad faith, especially when insurers use outdated data, ignore current market values, or fail to consider all damages. Insurers may refuse to pay for original manufacturer parts, insist on aftermarket components, or undervalue your vehicle using flawed valuation methods. If you're unsure whether an offer is fair, learn more about disputing a car insurance settlement so you can recognize when you're being shortchanged.

Compare Car Insurance Rates in Ohio

See if you qualify for a lower rate in less than 2 minutes

Common Examples of Bad Faith Insurance Practices

Understanding real-world examples helps identify when your insurer may be acting in bad faith. These scenarios occur across various insurance types, affecting millions of policyholders annually.

Car Insurance Bad Faith Examples

Auto insurers engage in bad faith through multiple tactics. They may deny accident claims despite clear liability evidence, refuse to honor uninsured motorist coverage when hit-and-run drivers flee the scene, or deliberately delay rental car reimbursements and medical payment coverage.

Recent cases underscore how serious these violations can be. A Colorado jury awarded $145.26 million to Fermin Salguero-Quijada against NorGUARD Insurance for denying rehabilitation after a traumatic brain injury, and a Nevada jury returned a $114 million verdict against USAA ($100M punitive) after finding it improperly denied and delayed a policyholder's claim. More recently, a North Carolina business court ruled on March 3, 2026 that a captive insurer accused of stalling a $116 million claim to protect its parent's sale cannot escape bad faith liability, holding that an insurer can still face bad faith liability for claims-handling conduct even if the claim is ultimately paid. If your auto claim was mishandled, review our car insurance dispute resolution guide.

Home Insurance Bad Faith Scenarios

Property insurers act in bad faith by undervaluing damage from covered events like fires or storms, claiming damages were pre-existing without evidence, or canceling policies retroactively to avoid paying claims. Some companies refuse to pay for temporary housing despite loss of use coverage explicitly included in your policy. If you're facing a property claim denial, our guide on home insurance claim denial reasons explains how to fight back.

Following major disasters, insurers may overwhelm policyholders with excessive documentation requests, hoping policyholders will give up pursuing legitimate claims. They might dispute contractor repair estimates without providing valid reasoning or alternative assessments from qualified professionals.

Life Insurance Bad Faith Tactics

Life insurers engage in bad faith by rejecting claims based on irrelevant pre-existing conditions not disclosed in the policy, demanding excessive documentation from grieving beneficiaries, or misrepresenting policy exclusions to deny death benefits. Some carriers delay payments for months while "investigating" straightforward death claims. Beneficiaries facing a wrongful denial should read our guide on life insurance claim denials.

Health Insurance Bad Faith Behavior

Health insurers act in bad faith by denying coverage for medically necessary treatments, refusing to follow physician recommendations without valid medical reasons, or terminating coverage during treatment without proper notice. Insurers may label procedures as "experimental" despite widespread medical acceptance, or refuse pre-authorizations for procedures their own policies clearly cover.

Protect your car with Farmers

Average Rate:

Find coverage options that fit your budget.

The insurance savings you expect.

Average Rate:

Enjoy personalized policies, comprehensive coverage & more.

See how much you could save today!

Average Rate:

Drivers who switch their auto insurance and save with State Farm save $764 on average!

Safe Drivers Save with Allstate®

Average Rate:

Get rewarded with savings for having a clean driving record.

Legal Remedies and Potential Damages

When insurance companies act in bad faith, policyholders have legal recourse to recover damages beyond the original policy benefits. Understanding available remedies helps you evaluate whether pursuing legal action makes financial sense.

Types of Damages Available

Compensatory Damages cover actual losses including unpaid policy benefits, emotional distress, interest on delayed payments, and related costs such as attorney fees. You can recover medical bills paid out-of-pocket, lost wages from missing work to fight the claim, and even increased premiums incurred when forced to find new coverage.

Punitive Damages punish egregious insurer misconduct and deter future bad faith practices. Courts award punitive damages when insurers act with recklessness or malice. As shown in recent verdicts, these awards can significantly exceed compensatory damages.

Attorney Fees and Costs are often recoverable in bad faith cases, making legal representation more accessible. Unlike typical contract disputes where each side pays their own fees, bad faith statutes in many states allow courts to order insurers to reimburse your legal costs.

Notable Damage Awards

Recent verdicts illustrate the potential scale of bad faith claims. Juries have shown they are willing to impose significant punitive awards for egregious conduct:

| Case | State | Total Award | Punitive Damages |

|---|---|---|---|

| NorGUARD brain injury denial | Colorado | $145.26 million | Substantial punitive component |

| USAA auto collision delay | Nevada | $114 million | $100 million |

| Quota-share insurers bad faith | Indiana (federal) | $112 million | Included |

| Ceimo v. Paul Revere (disability) | Various | $84 million | Included |

| Captive insurer stalling | North Carolina | $116 million claim (2026 ruling) | Pending |

While not every case results in eight-figure verdicts, even moderate bad faith cases often settle for multiples of the original claim value once insurers face litigation exposure. Most routine bad faith settlements typically resolve in the $50,000 to $250,000+ range for individual policyholders, with high-impact cases reaching the low-to-mid seven figures.

Statutory Remedies by State

Some states provide statutory awards without requiring proof of injury beyond lost benefits. Texas allows statutory damages when denials lack a reasonable basis, along with interest on delayed payments. Georgia's primary bad faith statute is O.C.G.A. § 33-4-6, which provides that if an insurer refuses to pay a covered loss within 60 days after demand and that refusal is in bad faith, the insurer is liable for the full amount of the loss, plus up to 50% of the liability for the loss or $5,000 (whichever is greater), plus all reasonable attorney's fees.

Florida's 2023 tort reform still controls in 2026: mere negligence by an insurer is no longer enough to establish bad faith, and an insurer has no liability for bad faith on a liability claim if it tenders the lesser of policy limits or the amount demanded within 90 days after receiving notice with sufficient evidence to support the claim amount. In May 2025, Georgia Gov. Brian Kemp signed HB 1344, the Georgia Insurance Affordability and Claims Integrity Act, which strengthens claims oversight through increased penalties, enhanced fraud enforcement, improved storm claims processes, and stronger uninsured motorist requirements.

| State | Statutory Remedy | Key Notes |

|---|---|---|

| Texas | Statutory + interest | 2-year bad faith deadline |

| California | Consequential + punitive | Emotional distress damages available |

| Florida | Fees + interest + punitives | 2023 safe harbor still controls |

| Georgia | 50% penalty or $5,000 + fees | 60-day demand rule under § 33-4-6 |

| Louisiana | Proven economic damages only | Act 3 (2024) narrowed damages |

How to Document Bad Faith Insurance Practices

Proper documentation is essential for proving bad faith and maximizing your recovery. Start gathering evidence immediately when you suspect your insurer is acting improperly, because waiting reduces your chances of success.

Essential Documentation

Maintain comprehensive records of all interactions with your insurance company. Save every email, letter, claim form, and written correspondence. Keep detailed notes of phone conversations including dates, times, names of representatives, and conversation summaries. These records establish patterns of misconduct and prove you fulfilled your policy obligations.

Claim-Supporting Records

Preserve all evidence supporting your claim's validity. For auto claims, gather repair estimates, photos of damage from multiple angles, police reports, and witness statements. Medical claims require itemized bills, treatment records, physician recommendations, and diagnostic reports. Property claims need damage assessments, contractor estimates, and proof of loss.

Evidence of AI-Driven Misconduct

A key focus in 2026 bad faith litigation is preserving evidence of algorithmic denials. Indiana's HB 1271 (effective March 4, 2026) bars insurers from downcoding a claim on AI output alone without a professional's review, Alabama's SB 63 requires AI-assisted prior authorization decisions to rest on the individual's clinical circumstances, and similar rules apply in other states. Florida HB 527 explicitly prohibits using an algorithm or AI system as the sole basis for denying or reducing a claim payment, and a human professional must independently analyze the facts and certify that AI was not the lone decision-maker.

Watch for red flags: automated denial notices with no human explanation, repeated upload requests through digital portals, and any mention of "risk scoring" or "fraud flags" without supporting evidence. Track how many times the insurer requests the same documentation repeatedly, a common stalling tactic.

Timeline Documentation

Create a detailed timeline showing when you filed the claim, when the insurer acknowledged it, investigation milestones, and response delays.

| Event | Date | Insurer's Deadline | Actual Response |

|---|---|---|---|

| Claim filed | 1/15/2026 | 1/30/2026 | 2/20/2026 (21 days late) |

| Documents submitted | 2/5/2026 | 2/20/2026 | No response |

| Follow-up call | 2/25/2026 | N/A | "Under review" |

| Denial letter | 3/30/2026 | 2/15/2026 | 43 days late |

When to Hire a Bad Faith Insurance Attorney

Recognizing when to seek legal representation can significantly impact your case outcome. Early attorney involvement preserves evidence and builds a strong record of misconduct that insurers can't dismiss.

Warning Signs Requiring Legal Help

Hire an attorney immediately when your insurer denies claims without policy justification, delays payments beyond statutory timeframes, fails to conduct proper investigations, ignores your communications, refuses to defend covered lawsuits, or engages in obstructive tactics like repetitive document requests or shifting explanations.

Additional red flags include adjusters who won't return calls for weeks, denial letters referencing policy provisions that don't exist, threats to non-renew your coverage if you don't accept their settlement offer, automated denial notices with no clear human review, or adjusters who pressure you to sign releases before explaining what rights you're giving up.

Attorney Fee Arrangements

Most bad faith attorneys work on contingency: the standard fee is 33% to 40% of the recovery, sometimes lower if the case settles quickly, with $0 upfront in most engagements. A typical tiered structure is 33% for settlements reached before trial and up to 40% if the case has to be tried.

State Laws Governing Bad Faith Insurance

Bad faith insurance laws vary significantly by state, affecting what claims you can bring and what remedies are available.

First-Party vs. Third-Party Bad Faith

First-party bad faith involves disputes between policyholders and their own insurers over denied or delayed benefits. Most states recognize first-party bad faith claims, either through the implied covenant of good faith and fair dealing or specific statutes.

Third-party bad faith involves insurers failing to settle claims against their policyholders within policy limits or refusing to provide a defense. For example, if you carry $50,000 in liability coverage and the injured party offers to settle for $45,000, but your insurer refuses and the case goes to trial resulting in a $200,000 judgment, you could have a third-party bad faith claim for the $150,000 excess judgment.

2026 State-Specific Developments

Several 2026 court rulings have reshaped bad faith litigation. In March 2026, the Georgia Court of Appeals in Cannon v. Safeco reversed the dismissal of an insured's bad-faith claims and held that a liability insurer cannot fulfill its duties simply by turning over its policy limits without obtaining a release of claims pending against its policyholder. This means Georgia insurers face bad faith exposure even when they interplead policy limits.

Other jurisdictions have narrowed bad faith exposure. Ohio's Supreme Court tightened discovery in bad faith suits in February 2026, and Texas courts ruled that bad faith allegations alone don't defeat appraisal rights. Meanwhile, Louisiana's Act 3 of 2024 continues to narrow recoverable damages to proven economic losses in 2026.

How to File a Bad Faith Complaint

Taking action against bad faith insurers involves several steps, from initial complaints to potential litigation.

Step 1: Exhaust Internal Appeals First

Before escalating externally, complete the insurer's internal appeal process. File a formal appeal and allow time (typically 15 to 60 days) for a response. This step is often required before you can file an external complaint or lawsuit, and it creates a paper trail showing you acted in good faith.

Step 2: File a Complaint with Your State Insurance Department

Contact your state insurance regulator to file a formal complaint detailing the bad faith practices. You can find your state department through the National Association of Insurance Commissioners (NAIC) at naic.org. Provide documentation of denials, delays, or misconduct including copies of your policy, claim submissions, denial letters, and correspondence.

State insurance departments investigate consumer complaints and can impose fines, require corrective action, or compel the insurer to reconsider your claim. Their involvement creates an official record that may pressure the company to settle.

Step 3: Send a Bad Faith Demand Letter

Have your attorney draft a comprehensive demand letter outlining the insurer's misconduct and requesting full policy benefits plus additional damages. The letter should cite specific policy provisions supporting your claim, document each instance of bad faith conduct with dates and evidence, reference applicable state laws the insurer violated, and demand a specific settlement amount.

Step 4: File a Lawsuit and Enter Discovery

If the insurer doesn't resolve the issue, file a lawsuit in state superior court. Your complaint should allege breach of contract, breach of the covenant of good faith and fair dealing, and violations of state insurance regulations.

During discovery, your attorney will request internal claim files, adjuster notes, emails, policy manuals, and, increasingly relevant in 2026, records of any automated scoring or AI-driven denial decisions. This phase often reveals damaging evidence that dramatically increases settlement value.

Step 5: Settlement or Trial

Many bad faith cases settle once insurers face litigation exposure. Settlement negotiations typically intensify as trial approaches, and mediators often help parties reach agreements. If settlement isn't reached, a jury evaluates the insurer's conduct and determines damages.

Frequently Asked Questions

What is the difference between a claim denial and bad faith?

Not every claim denial constitutes bad faith. Insurers can legitimately deny claims that aren't covered under policy terms or lack sufficient supporting evidence. A denial becomes bad faith when it's unreasonable, lacks legitimate policy basis, results from an inadequate investigation, or ignores clear evidence supporting coverage. For example, denying theft coverage despite a police report and surveillance footage would likely be bad faith, while denying a claim for mechanical breakdown under comprehensive coverage is legitimate.

How long do I have to file a bad faith insurance lawsuit?

Statutes of limitations vary significantly: Alabama is 2 years for tort bad faith and 6 years for contract; Alaska is 2 and 3 years; Arizona is 2 and 6 years; California is 2 years for tort and 4 years for contract. Florida allows 5 years for statutory bad faith, and Louisiana is only 1 year for tort with 10 years for contract. Missing these deadlines permanently bars your claim, so consult an attorney as soon as you suspect bad faith. Check our claim statute of limitations guide for state-specific rules.

Can I sue my insurance company without an attorney?

While legally possible to represent yourself in a bad faith lawsuit, these cases are complex and insurers have experienced legal teams defending them. Most bad faith attorneys work on contingency (typically 33% for settlements and up to 40% if tried), meaning no upfront costs. Self-representation risks missing critical deadlines, failing to preserve evidence, or accepting settlements worth far less than your claim's actual value. Most successful bad faith outcomes involve experienced attorneys who understand how to prove unreasonable conduct.

What evidence proves insurance bad faith?

Strong bad faith evidence includes denial letters lacking specific policy justification, documented delays beyond statutory timeframes, proof the insurer ignored supporting documentation, internal communications revealing improper denial motives, and expert testimony that the insurer's conduct violated industry standards. In 2026, also preserve any evidence of automated or AI-driven denial decisions, repeated digital portal upload requests, or "fraud score" flags applied without a genuine factual basis. Save every email and note the dates, times, and representative names from phone calls.

Will suing my insurance company affect my future coverage?

Insurers cannot legally cancel or non-renew your policy in retaliation for filing a bad faith lawsuit. Such actions would constitute additional bad faith and violate state insurance laws. However, you may choose to switch insurers after resolving your claim since trust is often damaged beyond repair. State insurance departments take retaliatory cancellations seriously and can impose significant penalties against insurers that engage in this behavior.