Compare Car Insurance Rates in Ohio

See if you qualify for a lower rate in less than 2 minutes

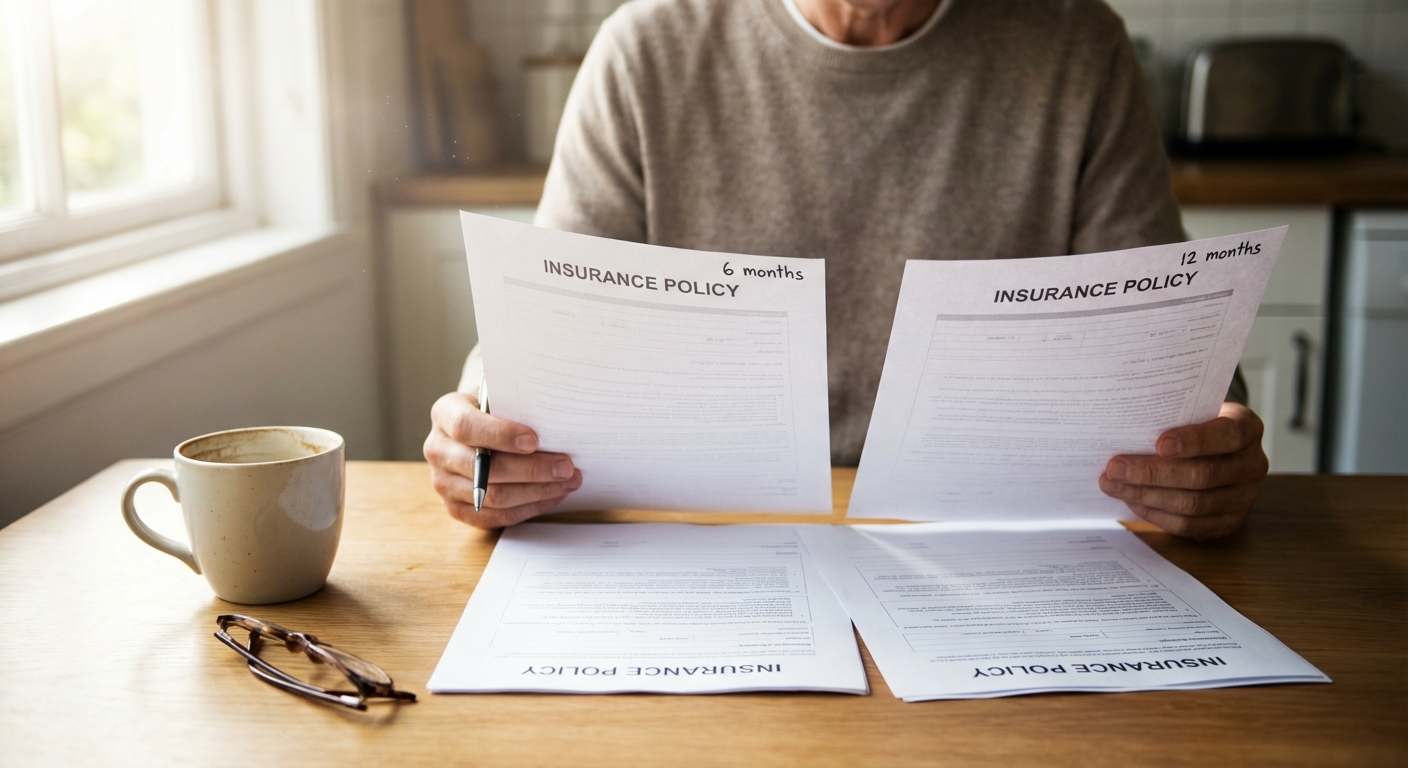

Why Most Car Insurance Policies Are 6 Months Long

If you've ever wondered why your car insurance renews every six months instead of once a year, you're not alone. The 6-month policy term has become the industry standard, and it's not an accident. Insurers designed shorter policy periods primarily for their own benefit: the ability to reassess and reprice your coverage twice per year rather than locking in rates for a full 12 months.

When a driver has an accident, picks up a speeding ticket, or sees their credit score change, a 6-month policy allows the insurer to adjust rates at the very next renewal instead of absorbing that risk for another year. From a business perspective, this protects the carrier from pricing mismatches caused by shifting risk profiles. At the same time, shorter terms allow insurers to stay competitive by adjusting prices in line with market conditions and rival carriers.

While 12-month policies were once more common, the shift to 6-month terms has become near-universal among major carriers, though annual options still exist if you know where to look. After a 6% drop in 2025, car insurance rates are projected to climb again in 2026, but only slightly. Insurify forecasts the national annual average will reach $2,158, a modest 1% increase from 2025's $2,144. More aggressive projections from Bankrate, Experian, and CarInsurance.com place the 2026 average closer to $2,500 to $2,926 per year, driven partly by 25% tariffs on imported auto parts, which push up repair and replacement costs and, in turn, insurance premiums. Understanding your policy term in this environment could save you hundreds of dollars per year.

How a 6-Month Car Insurance Policy Works

A 6-month (semi-annual) car insurance policy provides full coverage for exactly six months from the effective date. Once the term ends, you'll receive a renewal notice, typically 30 to 45 days in advance, that outlines your new premium, any changes to coverage, and your payment options. Many policies auto-renew if a payment method is on file, but you should always review your renewal notice carefully before it kicks in. Learn more about car insurance automatic renewal and what to watch for before your policy renews.

What Happens at Renewal?

At each renewal, your insurer re-evaluates your risk profile. Your new rate can go up or down based on:

- Driving record changes, such as new tickets, accidents, or DUIs. Most violations stay on your record for 3 to 5 years.

- Credit score shifts. In most states, credit is a key pricing factor. Drivers with poor credit can pay significantly more for full coverage than those with excellent credit. Note: California, Hawaii, Massachusetts, and Michigan prohibit insurers from using credit scores.

- State-level rate filings. If your insurer files for a rate increase in your state, it applies at your next renewal.

- Changes in your household, like adding a teen driver or removing a vehicle.

- Claims history. Even a single at-fault claim can trigger a bump at renewal.

- Tariff-driven repair costs. The 25% tariff on imported vehicles and auto parts has been in effect since April 2025, but its impact on car insurance premiums is just now starting to hit. University of South Carolina economist Robert Hartwig estimates the per-vehicle impact at $35 to $120 in additional annual premium, with broader projections placing tariff-related increases as high as 4 to 8 percentage points above baseline.

This means that with a 6-month policy, you're re-evaluated far more frequently than you would be under a 12-month plan. That can work for or against you depending on your situation.

Grace Period Note: If your policy expires and you haven't renewed, most insurers offer a grace period of 10 to 30 days. Act fast or purchase new coverage immediately to avoid a coverage gap and the rate hike that comes with it.

Compare Car Insurance Rates in Ohio

See if you qualify for a lower rate in less than 2 minutes

6-Month vs 12-Month Car Insurance: Pros, Cons & Key Differences

Choosing between a 6-month and 12-month car insurance policy isn't just about preference. It has real financial implications. Here's a side-by-side breakdown of both options:

| Feature | 6-Month Policy | 12-Month Policy |

|---|---|---|

| Rate Stability | Rates can change every 6 months | Rates locked for a full year |

| Flexibility to Switch | Can shop and switch twice per year | Locked in longer; may face cancellation hassles |

| Rate Improvement Timing | Faster savings if record improves | Must wait until annual renewal |

| Upfront Cost | Lower lump-sum if paying in full | Higher lump-sum payment required |

| Admin Frequency | Renew/review twice per year | Renew/review once per year |

| Availability | Widely available across all major carriers | Offered by select carriers only |

| Protection from Hikes | Less protection; rates can rise sooner | Shielded from mid-year market increases |

| Tariff Exposure | Rate hikes from tariff-driven repair costs hit sooner | Locked rate provides a 12-month buffer |

For a deeper dive into how payment timing affects total cost, check out our guide on car insurance cost per year vs per month.

Protect your car with Farmers

Average Rate:

Find coverage options that fit your budget.

The insurance savings you expect.

Average Rate:

Enjoy personalized policies, comprehensive coverage & more.

See how much you could save today!

Average Rate:

Drivers who switch their auto insurance and save with State Farm save $764 on average!

Safe Drivers Save with Allstate®

Average Rate:

Get rewarded with savings for having a clean driving record.

Who Benefits Most From Each Policy Term?

Not every driver has the same needs. The right policy term often depends on where you are in your driving history, financial profile, and current market conditions.

Drivers Who Benefit Most From Each Term

Choose a 6-month policy if:

- You recently had a ticket or accident that will drop off your record within 3 to 5 years

- Your credit score is actively improving (can unlock major savings in most states)

- You're a new or young driver building a clean history

- You prefer the flexibility of shopping for better rates more often

- You want a lower lump-sum amount when paying the full term upfront

Choose a 12-month policy if:

- Your record is clean and you want to lock in your current rate

- Tariff-driven or industry-wide premium increases are expected, and you want protection

- You prefer simplicity, one renewal per year instead of two

- Your insurer offers an annual loyalty discount that outweighs flexibility

What Is the Average 6-Month Car Insurance Premium in 2026?

Understanding what a typical 6-month premium looks like helps you gauge whether you're getting a fair rate. Here's where averages stand in 2026, based on the latest data from Insurify, The Zebra, ValuePenguin, and NerdWallet:

| Coverage Type | Avg. Monthly Cost | Avg. 6-Month Premium | Avg. Annual Premium |

|---|---|---|---|

| Full Coverage (Insurify) | ~$179–$186/month | ~$1,079 | ~$2,158–$2,237 |

| Full Coverage (The Zebra) | ~$194/month | ~$1,163 | ~$2,326 |

| Full Coverage (NerdWallet) | ~$192/month | ~$1,150 | ~$2,300 |

| Full Coverage (ValuePenguin) | ~$208/month | ~$1,248 | ~$2,496 |

| Minimum Liability | ~$52–$98/month | ~$312–$588 | ~$625–$1,176 |

Rates vary considerably by state. Drivers in high-cost states like Nevada, Louisiana, Florida, and New York pay significantly more, while those in lower-cost states like Vermont, Idaho, Ohio, and Maine tend to pay well below the national average. You can explore a full breakdown of car insurance cost per year vs per month to understand what you're really paying.

How 2026 Tariffs Are Affecting Your Renewal Rate

The 25% tariffs on imported auto parts have been firmly in place as of 2026, and their financial ripple effects are now reaching drivers across the country in the form of higher repair bills and steeper insurance premiums. When repair costs rise, insurers pass those costs to policyholders at renewal. The American Property Casualty Insurance Association (APCIA) estimates the 25% parts tariff will raise auto repair claim costs by about 2.7%, translating to roughly $80 to $100 more per repairable claim. For drivers on 6-month policies, this pressure hits every renewal cycle, making it a strong case for exploring annual terms if you qualify. Learn more about the full tariff impact on car insurance rates in 2026.

Which Major Insurers Offer 6-Month vs 12-Month Policies?

Most major carriers default to 6-month terms, but annual options are available, sometimes with restrictions.

| Insurer | Default Term | 12-Month Available? | Notes |

|---|---|---|---|

| GEICO | 6 months | Rarely | Standard 6-month; ask an agent for state-specific options |

| Progressive | 6 months | No | Now primarily 6-month across all states |

| State Farm | 6 months | Varies by state | Defaults to semi-annual in most states |

| USAA | 12 months | Yes | Military families only; flexible payment schedules |

| Erie Insurance | 12 months | Yes | Known for Rate Lock feature, holds rate flat until qualifying policy changes |

| Allstate | 6 months | Sometimes | Verify by state |

| Nationwide | 6 months | Verify by state | Rate stability programs available |

| Travelers | 6 months | Verify by state | Semi-annual standard in 2026 |

| Amica | Varies | Yes in some states | Strong option for stable-record drivers |

| Liberty Mutual | 6 months | Yes | Often cited as offering annual terms |

If annual rate stability is your top priority, USAA (military families), Erie Insurance, and Liberty Mutual are your best documented options. For maximum flexibility and frequent shopping opportunities, carriers like GEICO, Progressive, and State Farm give you the most options. Explore our guide on the best car insurance companies for 2026 to evaluate carriers side by side before choosing.

A Closer Look: Erie Insurance Rate Lock

Erie Insurance's Rate Lock feature is worth a special mention. Unlike standard annual policies that re-rate every year, Erie can help you avoid car insurance rate increases with the ERIE Rate Lock feature. Even if you have a claim, your rates won't change until you make certain changes to your auto insurance policy, such as adding or removing a vehicle or a driver from your policy or changing your primary garaging location. Your rate only recalculates if you make those specific changes.

ERIE Rate Lock (sometimes called Erie SelectAuto, or Erie RateProtect in New York) helps drivers avoid rate increases. Availability varies by state, and Rate Lock is currently available in IL, IN, KY, MD, NC, NY, OH, PA, TN, VA, WI, WV, and DC. In Virginia, the maximum lock period is limited to 3 years. This makes Erie one of the strongest rate-stability tools available to any driver who qualifies, particularly valuable in 2026 given ongoing tariff pressures. Read our full Erie car insurance review for a deeper dive, and learn how rate lock guarantees compare across other carriers.

Learn more about how rate locks and mid-policy rate changes work under each term. If you need short-term coverage between renewals, see our guide on temporary car insurance as an alternative. You can also review when and how to switch car insurance companies to stay on top of your rates every renewal cycle.

Frequently Asked Questions

Can I switch from a 6-month to a 12-month car insurance policy?

Yes, but availability depends on your insurer and your driving record. Some carriers only offer 12-month policies to drivers with a clean record spanning at least three years. Your best move is to ask at renewal time, since switching mid-term could involve cancellation fees or pro-rated refunds. If your current insurer doesn't offer annual terms, consider shopping carriers like USAA, Erie, Liberty Mutual, or Amica that do.

Is a 6-month car insurance policy cheaper than a 12-month policy?

Not necessarily. The annual cost is typically similar regardless of term length. The difference is in how costs are structured. A 6-month policy has a lower full-pay lump sum (currently ranging from roughly $1,079 to $1,248 for full coverage nationally depending on the source), making it easier to earn a pay-in-full discount of 5% to 20% without a massive upfront commitment. However, if rates rise at your 6-month renewal due to tariff-driven repair costs or record changes, your annual total could end up higher than it would have been under a locked-in 12-month rate.

How often can insurance companies raise my rates on a 6-month policy?

With a 6-month policy, your insurer can adjust your rate at every renewal, meaning up to twice per year. Rate changes can be triggered by a new accident or ticket on your record, a drop in your credit score (in most states), state-level rate filings, or general market trends like increased repair costs from tariffs. To minimize unwanted hikes, keep your driving record clean, monitor your credit, and compare competitor quotes at each renewal. You can also review our guide on short rate vs pro rata cancellation if you plan to switch carriers mid-term.

What happens if I cancel my 6-month car insurance policy early?

If you cancel before the term ends, your insurer will typically issue a pro-rated or short-rate refund for the unused portion of your premium. A pro-rated refund gives back the exact unused days, while a short-rate refund applies a small penalty for early cancellation. Always confirm your insurer's cancellation policy before switching mid-term and ensure your new coverage starts the same day to avoid a lapse. Review our how to cancel car insurance guide to understand any fees that may apply.

Do 12-month car insurance policies completely lock in my rate?

Generally yes. Your premium is fixed for the full year unless you make changes to your policy, such as adding a driver, changing vehicles, or updating your address. However, if you file a claim during the policy period, your rate may still increase at renewal. Erie Insurance is well known for offering a true Rate Lock feature that holds your rate flat until you make qualifying policy changes, even after claims or market-wide rate hikes, making it a standout option for drivers who prioritize long-term stability. Always confirm the specifics with your agent, as the feature must typically be added at renewal and eligibility requirements vary by state.