Compare Home Warranty Options in Ohio

See what plans you qualify for in less than 2 minutes

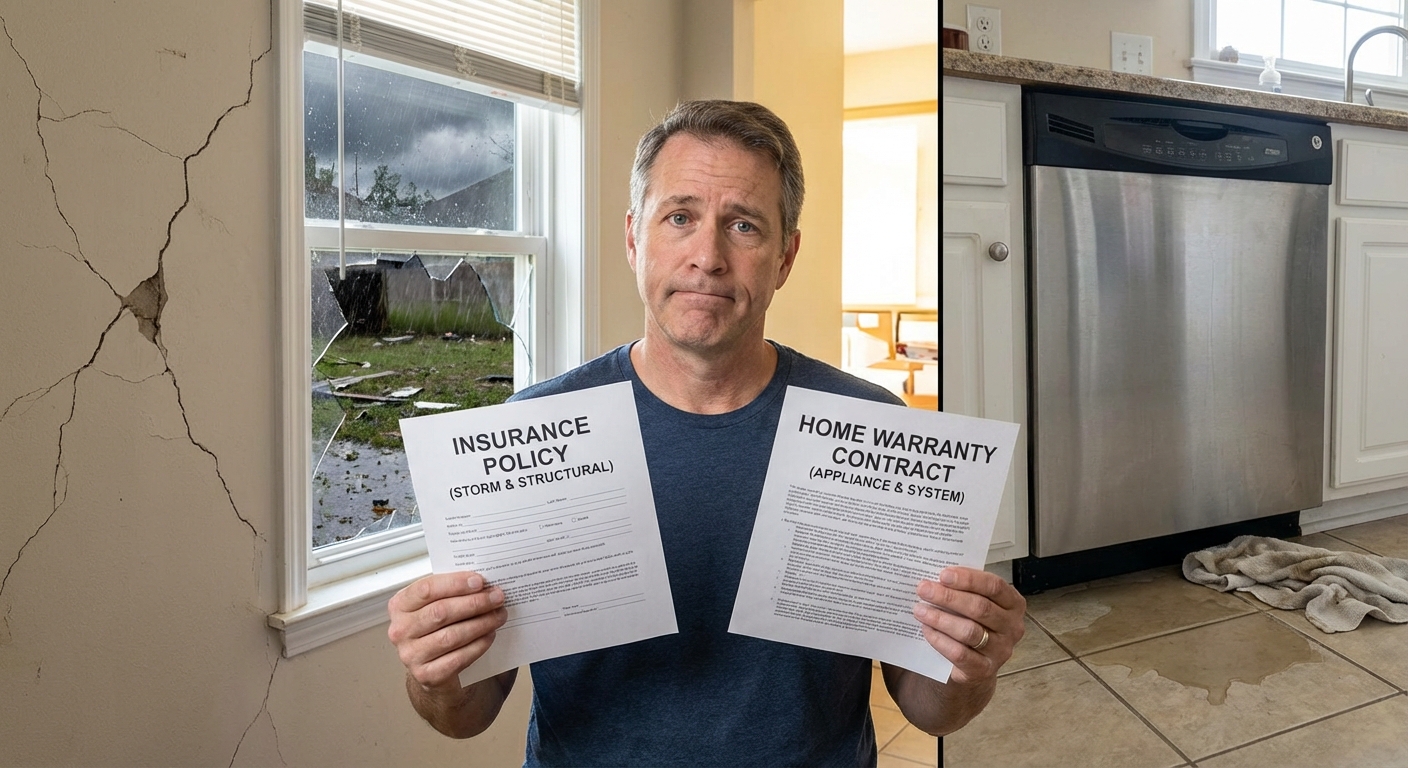

What Each Policy Actually Covers

Most homeowners assume that because both products protect their home, they overlap. They don't. Home insurance and a home warranty address completely different risks.

Homeowners insurance is a traditional insurance policy that protects your home and belongings from sudden, unexpected events. Common covered perils include:

- Fire and smoke damage

- Wind and hailstorms

- Theft and vandalism

- Lightning strikes

- Burst pipes (the resulting water damage, not the pipe itself)

- Personal liability if someone is injured on your property

If a tornado rips through your roof or a kitchen fire destroys your cabinets, homeowners insurance is what pays. Most mortgage lenders require you to carry it as a condition of your loan.

A home warranty, on the other hand, is a service contract (not insurance) that covers the breakdown of major home systems and appliances due to normal wear and tear. Typical items covered include:

- HVAC systems (heating and air conditioning)

- Plumbing and electrical systems

- Water heater

- Refrigerator, dishwasher, oven, and washer/dryer

- Optional add-ons like pools, septic systems, and roof leaks

When your 10-year-old air conditioner dies in July because it's simply worn out, your homeowners insurance won't touch it, but a home warranty very likely will. Learn more about what a home warranty covers in our complete coverage guide.

How Much Does Each One Cost in 2026?

Home Insurance Costs

The national average cost of homeowners insurance in 2026 ranges from about $2,395 to $2,868 per year, depending on the source and coverage level. Insurify reports an average of $2,868 annually (about $239 per month) for a policy with $300,000 in dwelling coverage, while LendingTree's national rollup comes in at $2,395 per year. Forbes puts the average at $2,720 per year for a $350,000 dwelling limit with a $500 deductible. Premiums vary significantly based on:

- Location, where coastal, hurricane, tornado, or wildfire-prone areas are far more expensive. Oklahoma now leads the nation at an average of $5,298 per year.

- Home value and rebuild cost, since higher-value homes carry higher premiums

- Deductible, where choosing a higher deductible (e.g., $2,500) lowers your premium

- Claims history and credit score, both of which insurers factor into pricing

- Discounts, such as bundling home and auto, installing security systems, or having a new roof

Home Warranty Costs

Home warranty plans are considerably more affordable than home insurance. NerdWallet's 2026 analysis pegs the average home warranty at $73 per month ($876 per year), with the range running from as low as $28 to as high as $191 per month. Here's how the major plan tiers break down:

| Plan Type | Avg. Annual Cost | Avg. Monthly Cost |

|---|---|---|

| Appliance-only plan | $400-$500 | ~$35-$45/month |

| Systems-only plan | $400-$650 | ~$45-$55/month |

| Combo (systems + appliances) | $500-$1,200 | ~$55-$75/month |

| Comprehensive with add-ons | $1,200-$1,500/year | $100-$125/month |

In addition to the annual or monthly premium, you'll pay a service call fee averaging about $108 per visit in 2026 (typically $75-$150) every time a technician is dispatched for a repair. This replaces the large deductible you'd pay with an insurance claim.

When weighing the home warranty vs saving money decision, the right answer depends on your home's age and your financial cushion. You can also explore our full home warranty cost guide for a deeper breakdown.

What's Excluded and Common Misconceptions

Understanding what isn't covered is just as important as knowing what is.

What Home Insurance Excludes

- Wear and tear, so your worn-out roof, old plumbing, or aging HVAC system are not covered

- Mechanical breakdown of appliances, meaning if your dishwasher motor burns out, that's not a covered peril

- Flood damage from rising water, which requires a separate flood insurance policy

- Earthquake damage, also excluded and requiring a separate rider or policy

- Neglect and poor maintenance, since insurers can deny claims tied to deferred upkeep

What Home Warranties Exclude

- Damage from perils, since fire, storms, or theft damage is insurance territory, not warranty territory

- Pre-existing conditions, since failures that existed before the contract started are typically excluded

- Improper installation or code violations, where if a system was installed incorrectly, the warranty may not apply

- Cosmetic damage, including scratches, dents, and non-functional parts

- Items exceeding coverage caps, since most warranties set per-item repair limits (often $1,500 to $5,000)

The Big Misconception: Many homeowners mistakenly believe a home warranty is a type of insurance. It is not. The Federal Trade Commission and most state regulators classify home warranties as service contracts, governed by contract law rather than insurance regulations. A smaller number of states regulate them under their insurance code with stricter reserve requirements, but in most jurisdictions, warranty companies are not held to the same solvency standards as insurance carriers.

Be sure to review the fine print carefully (especially exclusions and caps) before signing any contract. Our guide to the best home warranty companies of 2026 walks through what to look for.

Do You Need Both? Who Should Carry Each Policy

Homeowners Insurance: Nearly Everyone Needs It

If you have a mortgage, homeowners insurance isn't optional, since your lender requires it. But even if your home is paid off, going without it is a major financial risk. A single house fire or liability lawsuit could cost hundreds of thousands of dollars, and with premiums up roughly 24% nationally over the past few years, going uninsured is more dangerous than ever. Homeowners insurance is the financial safety net no homeowner should go without.

Home Warranty: Right for Some, Not All

A home warranty makes the most sense if:

- Your home is older, since aging systems and appliances are more prone to failure

- You have limited emergency savings, since a warranty converts unpredictable repair bills into a fixed monthly cost

- You recently bought a home and aren't familiar with the condition of its systems

- You prefer convenience, since the warranty company finds and dispatches contractors for you

A warranty may be less valuable if you have newer systems still under manufacturer warranties, a robust emergency fund, or a newer home. Explore home warranty alternatives and our home warranty for older homes guide to weigh your options.

Where to Buy Each

Homeowners Insurance: Purchase directly from insurers like State Farm, Allstate, or Farmers, or use a comparison tool to get quotes from multiple carriers at once.

Home Warranties: The most consistently top-rated companies for 2026 include American Home Shield (best for comprehensive coverage and HVAC), First American Home Warranty (best starter plan), AFC Home Warranty (best premiums), Liberty Home Guard (best add-ons), Cinch Home Services (best systems plan), 2-10 Home Buyers Warranty (best enhanced coverage), and Select Home Warranty (best for roof coverage). You can purchase directly from their websites or use a home warranty plans comparison to find the best fit for your budget.

Frequently Asked Questions

Is a home warranty the same as home insurance?

No, they are fundamentally different products. Home insurance is a regulated insurance policy that covers sudden and accidental damage from events like fire, storms, and theft. A home warranty is a service contract that covers the repair or replacement of appliances and systems due to normal wear and tear. They are governed by different laws and provide different types of protection.

Can a home warranty replace homeowners insurance?

Absolutely not. A home warranty cannot replace homeowners insurance, and most mortgage lenders legally require you to maintain a homeowners insurance policy. A warranty only covers mechanical failures of specific systems and appliances, not structural damage, theft, liability, or losses from fire or natural disasters.

How much does a home warranty cost per month in 2026?

Most home warranty plans cost between $30 and $90 per month in 2026, with NerdWallet pegging the cross-provider average at $73 per month. A basic appliance-only or systems-only plan averages around $35-$55 per month, while a comprehensive combination plan runs closer to $60-$75 per month. Premium plans with multiple add-ons can exceed $100 per month, and expect to pay an additional service call fee averaging $108 per visit.

Will home insurance pay to replace my HVAC system?

Standard homeowners insurance will not pay to replace your HVAC system if it fails from age or normal wear and tear. However, if your HVAC is damaged by a covered peril such as a fire or lightning strike, your policy may cover the resulting damage. For wear-and-tear breakdowns, learn what a home warranty covers and why it is typically the right solution for aging equipment.

Should I get both a home warranty and homeowners insurance?

For most homeowners, yes, especially those with older homes or aging systems. The two products complement each other perfectly: insurance protects against catastrophic, unexpected events while a warranty handles the everyday mechanical failures that insurance specifically excludes. Together, they provide comprehensive financial protection for your home from virtually every angle.